KUALA LUMPUR (May 6): Analysts have revised down their earnings forecasts and target prices (TPs) for Supermax Corp Bhd as they foresee lower average selling prices (ASPs) for gloves after the group’s net profit for the nine months ended March 31, 2021 (9MFY21) came in below their expectations.

Kenanga Research analyst Raymond Choo said in a note that the group’s 9MFY21 profit after tax and minority interests came in below expectations at 71% of his full-year forecast.

“The negative variance to our estimate was due to lower-than-expected ASPs. Hence, we downgrade [our] FY21/FY22 net profit [forecasts] by 6%/6%,” he said.

Following the roll-out of Covid-19 vaccines, which is likely to cause glove demand to moderate, the group highlighted that global glove prices had since dropped by 15% to 25%.

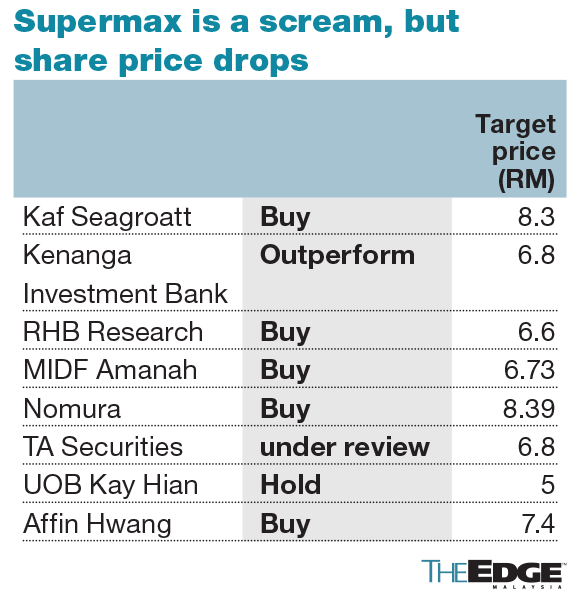

While reiterating his "outperform" call on Supermax, Choo downgraded his TP to RM6.80 from RM7.80 based on 11 times 2022 revised earnings per share (EPS) of 61.9 sen (previously 12 times).

RHB Research Institute analyst Alan Lim also said Supermax’s core net profit for 9MFY21 of RM2.85 billion was below expectations as it made up only 66% of his estimate.

He attributed the negative variance to the temporary closure of the company's production plant after the detection of several Covid-19 cases among its foreign workers.

“We have lowered [our] FY21 to FY23 core earnings [forecasts] by 21% to 41% due to a lower utilisation rate assumption of 85% from 90%,” he said.

According to him, Supermax’s FY21 utilisation rate was affected by the temporary plant closure, and for FY22 to FY23, the lower utilisation rate would stay due to normalised demand-supply assumptions.

He also reduced his ASP assumptions for FY21 to US$77 or about RM317.59 (from US$89), for FY22 to US$49 (from US$57), and for FY23 to US$37 (from US$48) after taking into account the recent ASP decline.

While maintaining his "buy" call on the stock, Lim lowered his TP to RM6.60 from RM8.75 due to a reduction in his earnings estimates and that of the long-term blended ASP to US$37.

“We believe near-term high ASPs will encourage more competition in future. We have lowered our long-term nitrile glove ASP [assumption] to US$40 per 1,000 pieces. Hence, [our] long-term blended glove ASP [estimate] for Supermax has been reduced to US$37,” he added.

MIDF Research analyst Ng Bei Shan, who also opined that Supermax’s 9MFY21 results missed expectations, believes the group’s ASPs were likely to have peaked in the third quarter ended March 31, 2021 (3QFY21).

“Gauging Supermax’s latest set of results, we think that ASPs for the company had likely peaked in 3QFY21,” she said.

She expects that ASPs may moderate depending on the development of the pandemic, and how well and soon the situation can be contained.

“We understand that some buyers are adopting a wait-and-see approach in replenishing their inventories given the high prices currently,” she said.

She revised down her FY21 and FY22 earnings forecasts by 4.7% and 6.7% respectively for Supermax as she adjusted her ASP and input cost assumptions to better reflect current market dynamics.

While reiterating her "buy" call on Supermax, she lowered her TP to RM6.73 from RM13.83.

Meanwhile, Affin Hwang Capital analyst Ng Chi Hoong said Supermax's 9MFY21 results missed his expectations mainly because he underestimated the duration of the production halt in February, which was estimated to be around 5% to 10% of the production volume for the quarter.

“We are lowering our earnings forecast for FY21 by 7% to factor in the 3QFY21 performance and lowering our TP to RM7.40 (from RM10.90), while maintaining our 'buy' call,” he added.

His forecasts already factored in a 5% to 10% decline in ASPs by year end, and a 3% to 5% month-on-month decline in ASPs in 2022.

Supermax shares encountered some selling pressure this morning after it delivered the set of lacklustre results. The counter, which was the top loser this morning, fell as much as 71 sen or 12.75% to RM4.86.

At 10.53am, the counter had pared some losses at RM5.04, still down by 53 sen or 9.52%.