This article first appeared in The Edge Malaysia Weekly on April 3, 2023 - April 9, 2023

Jitters over the health of banks continue to roil stock markets, and as a result, financial conditions are tightening. There is a flight to safety, from smaller to larger banks as well as to low-risk money market funds. Liquidity is being drained from the global banking system, partially reversing excesses from years of quantitative easing. Many banks too are responding by being more cautious and imposing stricter lending standards. All of the above will raise the risks of a global credit crunch, affecting spending and investments. Businesses, especially smaller ones, are finding it harder to refinance and borrow from banks or raise money from capital markets. Tighter credit will most likely bring forward a global economic recession. It is also disinflationary.

This banking crisis was precipitated by the US Federal Reserve’s extraordinarily loose monetary policy during the Covid-19 pandemic, followed by extraordinarily steep interest rate hikes over the past one year. So, it is somewhat ironic that the crisis will be giving the central bank a helping hand in cutting aggregate demand and damp inflationary pressures. By all indications, the Fed (and likely other major central bankers) is nearly done with its current interest rate hike cycle — though the fallout will continue to reverberate across the broader economy.

While the absolute quantum of interest rate increase has, so far, been less than, say, during the late 1970s and early 1980s, and current interest rates are still relatively low by historical standards, the hikes came exceptionally fast and steep. Case in point: The federal funds rate (FFR) rose from near zero to between 4.75% and 5% currently, equivalent to a 20-fold increase. Yields on the benchmark 10-year Treasury rose from 1.52% at the start of 2022 to a high of 4.25% in October, an increase of 2.75%, or 2.8 times. Such aggressive interest rate hikes have consequences.

Stocks were pummelled last year, particularly high-growth tech stocks, as the fall in values of their discounted future cash flows was larger. The interest rate-sensitive global housing market slumped as people struggled to adjust to sharply higher borrowing costs. In the US, the 30-year fixed mortgage rates more than doubled from 3.1% to 6.4% currently, after hitting a high of 7.1% in late 2022. According to a recent Organisation for Economic Co-operation and Development report, housing prices in 31 of the 46 economies it tracks fell in the most recent quarter of available data.

Meanwhile, traditionally low-risk bonds, including the “safest” US Treasuries, suffered their worst losses on record in 2022. Bonds have fixed-income streams whose values fall when interest rates rise. The longer the bond’s term to maturity, the worse the drop in market values (price).

The bond market’s historic price slump spilled over into the banking sector this month. Banks the world over are, collectively, sitting on huge unrealised losses, given that bonds (government, corporate and mortgage-backed securities [MBS]) typically make up a material portion of their assets.

We did a back-of-the-envelope calculation to illustrate the drop in value (see Table 1). An investor in the 10-year US Treasury would have suffered a capital loss of 15.3%, based on the yield difference of 1.96% between January 2022 and today. You can do the simple maths — multiply this percentage loss by the banks’ total bond holdings, and you would have a colossal figure for unrealised losses. For instance, US banks collectively held about US$5.5 trillion (RM24.3 trillion) in bonds (mainly agency-backed MBS and Treasuries) — accounting for about 24% of total assets — at end-2022. Of course, bonds of different durations will have varying degree of losses — those with shorter maturities will have smaller losses than those with longer maturities. The Federal Deposit Insurance Corp (FDIC) estimates total unrealised bond losses for US banks at US$620 billion at end-2022.

As long as banks do not sell the bonds, these are simply paper losses. (There are different accounting treatments for losses depending on how a bank classifies its holdings. More on this later.) The problem starts when banks are forced to sell their bonds, thereby realising the losses. We saw just how quickly and easily this could morph into a systemic banking crisis, in the US this month.

For a quick recap, Silicon Valley Bank (SVB) became the second-largest bank to fail in US history, the biggest being Washington Mutual Bank in 2008, following a run on the bank. What happened? SVB had an abnormally high percentage of bond holdings (56% of total assets) on its balance sheet and as unrealised losses mounted, worried depositors — mostly Silicon Valley start-ups and venture-capital firms with large, uninsured deposits (of more than US$250,000 per account) — rushed to withdraw their money. The sudden huge outflow of deposits forced SVB to liquidate its bonds at current market values (losses), which then tipped it into insolvency (where the values of liabilities exceeded assets). The bank had to be taken over by FDIC on March 10 to stem contagion fears. Another regional bank, Signature Bank, suffered the same fate and went into FDIC receivership just days later. Despite the quick actions, worries continued to spread to other smaller banks, all of which continue to suffer substantially higher-than-normal deposit withdrawals.

The fallout reverberated around the world — turning into a crisis of confidence in the global financial system. In Europe, the Swiss government instructed UBS Group AG to mount an emergency rescue of compatriot Credit Suisse Group AG, which, incidentally, is already beset with its own set of problems. Since the SVB turmoil, banks have lost tens of billions in market value, some more than others. For instance, leading Japanese banks have been harder hit, as they had accumulated foreign bonds in recent years — in the search for yields on the back of more than two decades of a zero interest rate policy, crowding-out by the Bank of Japan as well as slow loans growth in the domestic market.

Is SVB a canary in the coal mine?

Who is next? Investors are poring over the balance sheets of banks everywhere, trying to identify the next problem bank. Most recently, shares in Deutsche Bank were pummelled after the cost of insuring against default for its debt surged. Are Malaysian banks vulnerable to similar unrealised bond losses and liquidity troubles?

As we have explained previously, the issues for SVB are, to a certain extent, idiosyncratic — an exceptionally narrow customer base and high uninsured deposits (according to various reports, they ranged from 88% to 96% of total deposits), abnormally high long-dated bond holdings relative to traditional loans and, critically, failure to hedge interest rate risks.

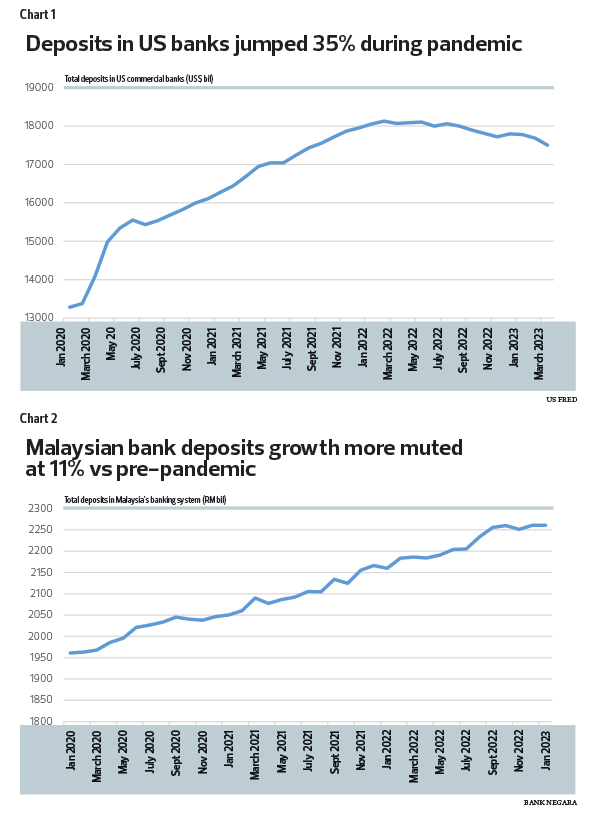

The overall US banking system is, no doubt, suffering from withdrawal symptoms — from excessive government stimulus, near-zero interest rates and massive quantitative easing over the past few years. At the outset of the pandemic, banks were inundated with large deposit inflows — excess savings surged from generous government handout, coupled with little avenue to spend during lockdowns.

Bank deposits increased by nearly US$5 trillion, or 35%, from about US$13.4 trillion in March 2020 to US$18.1 trillion in March 2022 (see Chart 1). Meanwhile, loans to businesses were limited during the pandemic. Banks had to put all these excess cash to work, and many ended up buying Treasuries and especially MBS (new mortgages and refinancing activities saw a huge jump as the housing sector boomed). Then the Fed started hiking interest rates aggressively.

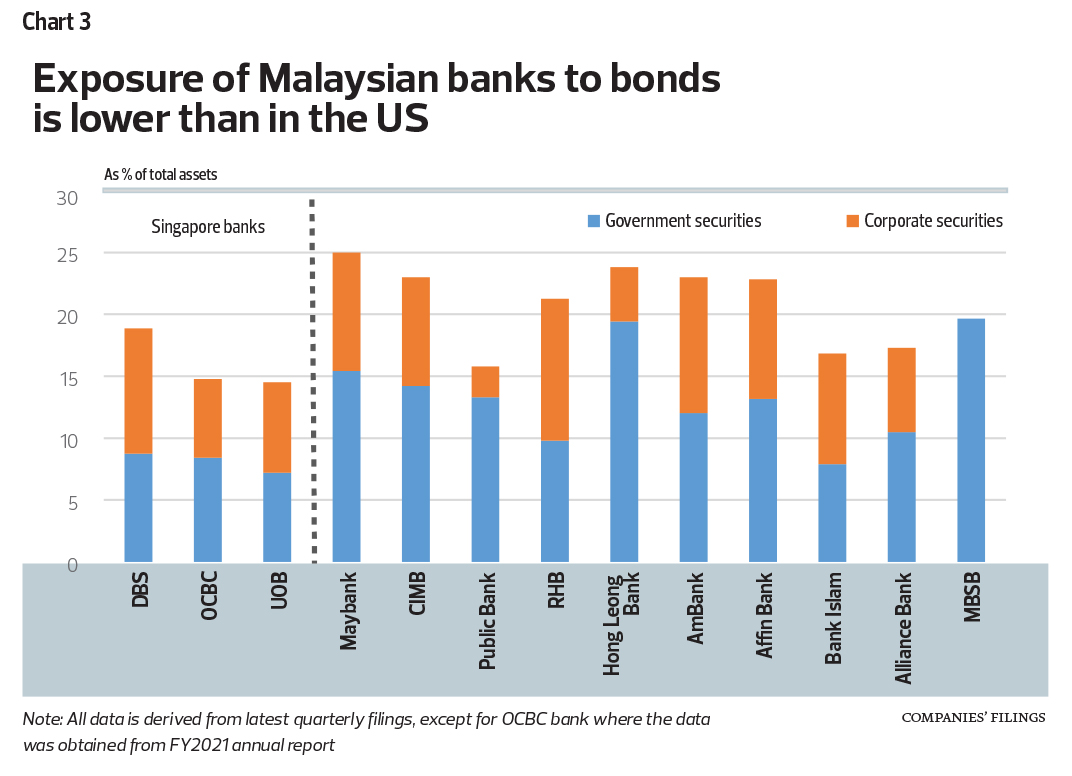

Clearly, the situation is quite different in Malaysia. For starters, pandemic cash handouts were far smaller and, while deposits also rose during the pandemic — owing to loan moratoriums and lower spending — it was nowhere near the scale of that in the US. Total deposits increased from RM1.968 trillion to RM2.186 trillion between March 2020 and March 2022, or equivalent to just about 11% growth (see Chart 2).

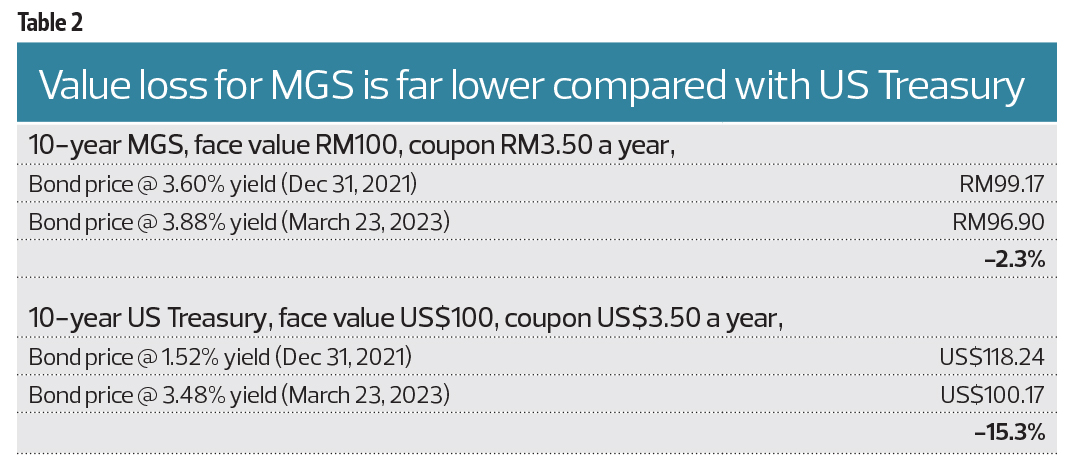

And while investments in government and corporate bonds also rose at the outset of the pandemic — as a result of excess deposits and lower loan demand — the increase was small, from 17.9% in January 2020 to a high of 19.7% of total assets in August 2021. Currently, the average bond holdings among Malaysian banks is 19.1% of total assets, or about RM645.2 billion, compared with 24% in the US banking system. Of note, 90% of the total are made up of local bonds — only 10% of which are foreign currency denominated bonds (see Chart 3).

Bank Negara’s tempered OPR hikes limit interest rate risks for banking system …

More importantly, Bank Negara Malaysia has raised the overnight policy rate (OPR) by only 1%, from 1.75% to 2.75% over the same period (compared with the 4.75% hike in the US FFR). Yields for the benchmark 10-year Malaysia Government Securities (MGS) have risen by even less — from 3.6% at the start of 2022 to 3.88% currently. The yield differential is less than 0.3%. This means the drop in value for 10-year MGS is only about 2.3%, based on our back-of-the-envelope calculations (see Table 2).

This is a huge difference compared to the 15.3% drop in value for the 10-year Treasury. Furthermore, unrealised losses for shorter duration bonds will be much lower. For instance, more than half of Maybank’s bond holdings have durations of less than five years.

In short, total unrealised losses for local banks should be much lower. (Incidentally, the majority of loans [79%] are based on floating interest rates, which are repriced immediately on Bank Negara’s policy rate changes.) Therefore, we think interest rate risks for the overall Malaysian banking system is low. Naturally, some banks will be affected more than others. For instance, Maybank, CIMB, Hong Leong Bank, Ambank, Affin Bank and RHB Bank have a higher percentage of bonds on their balance sheets compared with banks such as Public Bank, Bank Islam, Alliance Bank and MBSB. This could be due to a combination of factors, including deposit inflows, the ability to make loans and the target customer market.

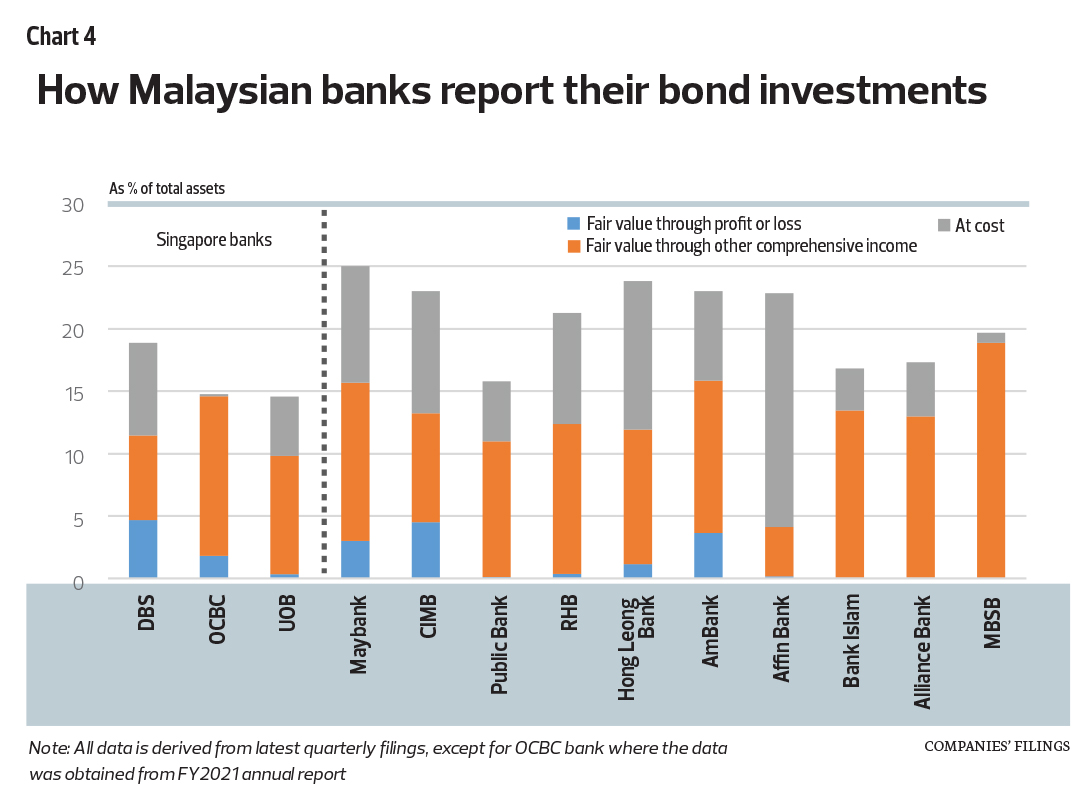

Banks have some discretion in terms of accounting for their bond holdings (which is part of financial assets and liabilities) and treatments for unrealised gains and losses. Under IFRS 9 (known as MFRS 9 in Malaysia and SFRS 109 in Singapore), bond investments can be measured at cost (if they are intended to be held to maturity) or at fair values (if they may be sold before maturity). And there are guidelines for treating changes in fair value measurements — they can be reflected through either the profit and loss (FVTPL) or other comprehensive income (FVOCI).

Under the first option, gains (losses) are recognised in the Income Statements, meaning reported net profit for the period is higher (lower). Under the second option, gains (losses) are disclosed below the net profit line in the Statements of Comprehensive Income. In this case, the gains (losses) have no impact on reported net profit. However, both the FVTPL and FVOCI options have balance sheet effects — unrealised gains (losses) will increase (decrease) retained earnings and shareholders’ equity (see Chart 4 for the different approaches in the accounting treatments for bond investments by Malaysian banks).

For instance, Affin Bank and, to a lesser extent, Hong Leong Bank have the highest proportions of bond investments measured at cost, which could indicate that, in the current environment, both their reported net profit and equity may be “overstated”. By comparison, the other seven local banks have, on average, mark-to-market some 63% of their bond holdings. In addition, Maybank, CIMB and Ambank would have adjusted their reported profit lower for a portion of these unrealised losses.

As mentioned above, bond holdings that are mark-to-market will affect balance sheets — unrealised losses or impairments will drag on the capital adequacy ratio of banks. Herein lies the importance of Bank Negara’s more tempered path for interest rate hikes. The smaller interest rate hikes mean lower unrealised capital losses, thus limiting the negative impact on lending capacity and/or need to raise fresh capital.

Smaller interest rate hikes also help keep a lid on the burden for debt servicing, for leveraged households, businesses as well as the government. Government debt and liabilities totalled RM1.5 trillion, or 83% of GDP.

In short, Bank Negara is protecting the lending capacity of the domestic banking system — and economic growth. Banks typically run into trouble because of deterioration in the quality of their assets, when bad debt provisions and write-offs increase. This could still happen if the expected global recession hits hard and affects the ability of businesses to service/repay their debts. At this point in time, however, interest rate risks — that are currently afflicting US and European banks — for Malaysia’s banking system appear low.

… but there is a trade-off

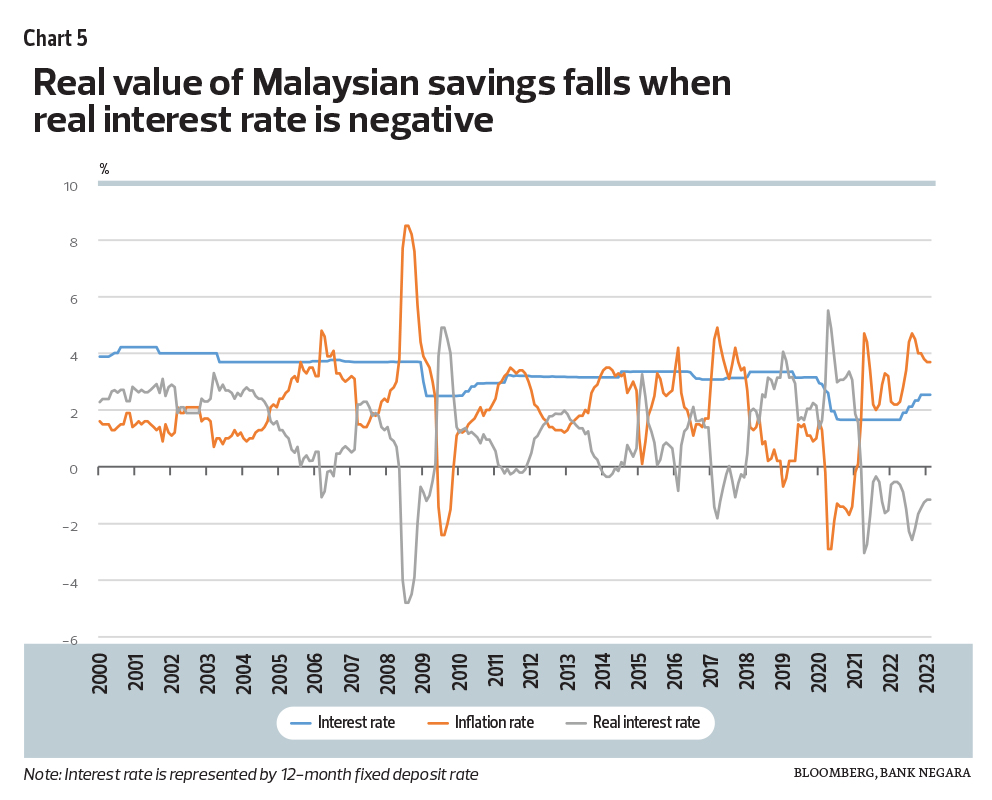

As with everything in life, there is a trade-off. And as we have always said, there is no free lunch in economics. First, savers could have obtained more had interest rates gone higher. With high inflation, savings are now earning negative real rates (that is, below inflation) (see Chart 5).

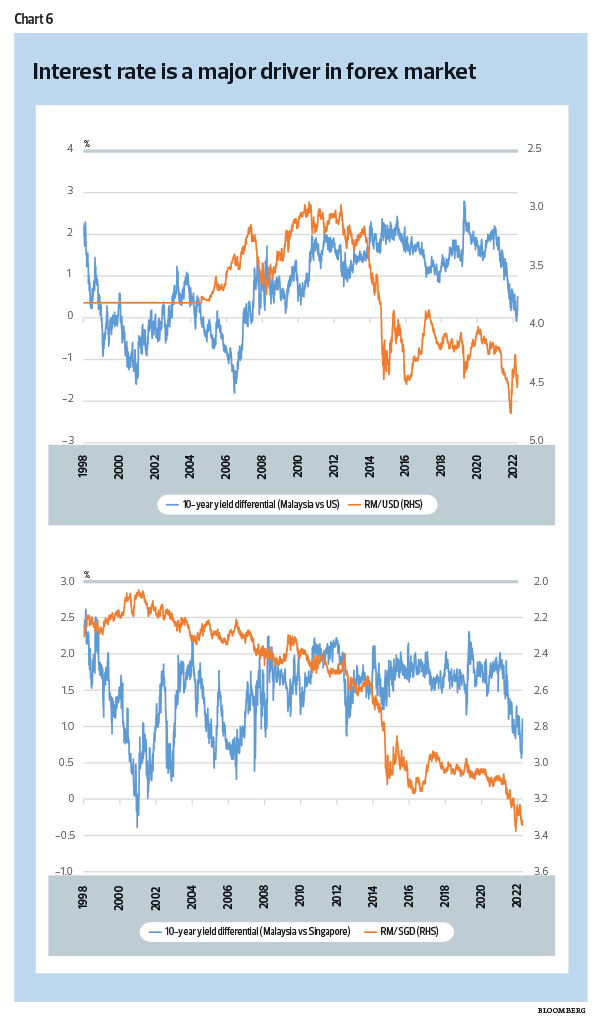

Second, the trade-off is a weaker ringgit — and higher cost of living for all Malaysians. The interest rate is the price of money (or credit or time, if one is inclined to be argumentative) — and it certainly is one of the major drivers in foreign exchange movements (see Chart 6); although this relationship is by no means linear or perfect. Can a country maintain a relatively low interest rate while also stabilising its exchange rate? Is the weak ringgit a function of the interest rate differentials between the ringgit and other currencies or are there even more dominant factors? We will address more of these issues in our articles over the next two weeks.

The Global Portfolio was up 2.5% for the week ended March 29, led by double-digit gains for Alibaba Group Holding Ltd (+14.1%) and Tencent Holdings Ltd (+10.8%). Shares in Grab Holdings Ltd also regained some recent lost ground, up 8.6%. On the other hand, the iShares 20+ Treasury Bond ETF fell 2% last week. We remain convinced that Chinese-based stocks will perform well in the foreseeable future. Thus, we have added BYD Co and Meituan to the portfolio. Following these latest transactions, the Global Portfolio is now fully invested. Total portfolio returns since inception stand at 25.1%, trailing the MSCI World Net Return Index’s 42.3% returns over the same period.

Meanwhile, we reinvested most of our cash in the Malaysian Portfolio into low-risk bonds, via the ABF SG Bond Index Fund ETF. Cash holdings were pared to 8.7% of total portfolio value. Total portfolio returns now stand at 139.5% since inception. This portfolio is outperforming the benchmark FBM KLCI, which is down 18.2%, by a long, long way.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.