This article first appeared in The Edge Malaysia Weekly on August 31, 2020 - September 6, 2020

AMID the market rally centred on counters related to the pandemic, a number of consumer stocks with decent business profiles tend to be overlooked.

One such stock is Padini Holdings Bhd, with net cash of RM440 million and a decent dividend yield of 3.2%. However, with analysts having mixed views on the fashion retailer, it tends to be overlooked by investors.

In earlier reports, Padini’s prospects were seen as unexciting due to cautious consumer spending amid the subdued economic outlook and low wage growth, coupled with its inability to fully pass on the Sales and Services Tax, effective Sept 1, 2018, to end users.

What retail analysts also did not find helpful to Padini’s traditional business model was the saturation of the local fast-fashion industry, coupled with the emergence of online fashion retailers. Additionally, the ringgit’s weakness against the yuan has resulted in higher cost of apparel imports from China.

Padini swung to the red in the fourth quarter ended June 30, 2020 (4QFY2020), which it attributed to lower sales resulting from the implementation of the Movement Control Order (MCO) from March 18, which restricted business operations in the quarter under review. The group reported a net loss of RM16.84 million on the back of RM174.2 million in revenue for the quarter, compared with a net profit of RM54.43 million against revenue of RM516.47 million for 4QFY2019.

According to the Malaysia Retail Industry July Report by Retail Group Malaysia, the fashion and fashion accessories sub-sector recorded a contraction of 30.5% in 1Q2020, making it the worst-performing retail sub-sector during the period.

Considering the varied opinions on Padini, analysts point out that the impact on earnings has been felt across the industry and that the company is faring fairly well considering the circumstances.

For its financial year ended June 30, 2020 (FY2020), Padini has made three interim dividend payouts of 2.5 sen per ordinary share amounting to RM49.34 million in total.

“No sales (were) generated during the MCO period from March 18, 2020, until May 4, 2020,” says Padini, which will not be rewarding shareholders with a dividend for 4QFY2020.

“Retail business in general is impacted by the outbreak of Covid-19 to varying degrees, both in terms of sales as well as profitability. Management will continue to implement measures to control costs, optimising working capital, preserving cash and streamlining its operations to minimise the impact. The next financial year remains challenging and the outlook is still unpredictable as the full impact of the Covid-19 pandemic cannot be ascertained until the health crisis is fully brought under control,” it adds.

While Padini did not declare a dividend in 4QFY2020, historically, the company managed to do so even during the economic downturn in 2008 and 2009.

In FY2019, full-year dividends totalled 11.5 sen, comprising quarterly payouts of 2.5 sen per share as well as a special dividend of 1.5 sen.

While historical dividends are not representative of future dividends, an analyst views the company’s historical record as relevant and can fairly serve as good guidance for payouts in time to come.

“This is on the group’s cash hoard of RM586 million to sustain yearly dividend payments of RM76 million and Covid-19 not negatively impacting Padini’s business landscape for the long term. With regard to its dividend prospects, my overall take is that dividend would resume soon corresponding to quarterly earnings recovery and a positive operating cash flow,” an analyst who declines to be named tells The Edge.

He notes that Padini’s January to March 2020 net cash from operating activities was negative, given that operations cash flow for the nine-month period ended March 31, 2020, was reduced to RM130 million from RM217 million during the six-month period ended Jan 31, 2020. The fact that the cash-flow decline would likely continue into the upcoming quarter means it is reasonable for Padini to hold off dividend payment to preserve cash flow for now.

“That said, the worst would be over for them, albeit recovery could be eventual. Note its strong balance sheet position, which has enabled it to weather the unfortunate black swan event,” he says.

Kenanga Research says Padini’s FY2020 core net profit (CNP) of RM75.2 million came in below its consensus expectation, due to lower-than-expected margins on price discounts to attract consumers. As such, the research house cut its estimated FY2021 CNP by 18% and target price to RM2.15 from RM2.65 and maintains its market perform call.

Meanwhile, AmInvestment Bank Research sees improvement in the fashion retailer’s sales in subsequent quarters following the easing of restrictions.

“However, we believe Padini’s long-term prospects will be challenging due to the unexciting domestic outlook and saturation in the fast-fashion industry,” it says.

The research house downgraded its “hold” call to “buy”, with a lower fair value of RM2.36 from an earlier RM3.02 per share, which is based on a price-earnings ratio of 13 times FY2022F earnings per share.

According to Bloomberg, analysts have a 12-month consensus target price of RM2.40 on Padini with four having a “buy” call, six “hold” and two “sell”.

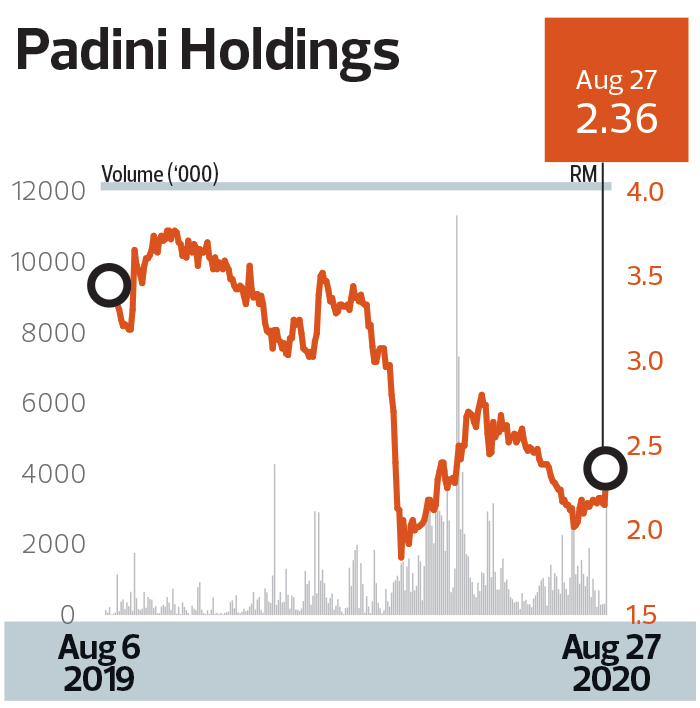

Last Thursday, despite the poor 4QFY2020 results, Padini’s share price rose 20 sen or 9.3% to RM2.35 in mid-day trade from RM2.15 the day before. It ended the day at RM2.36, giving it a market capitalisation of RM1.553 billion.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.