This article first appeared in The Edge Malaysia Weekly on April 8, 2019 - April 14, 2019

The love-hate relationship between Malaysia and its biggest trading partner, Singapore, will come under the spotlight again.

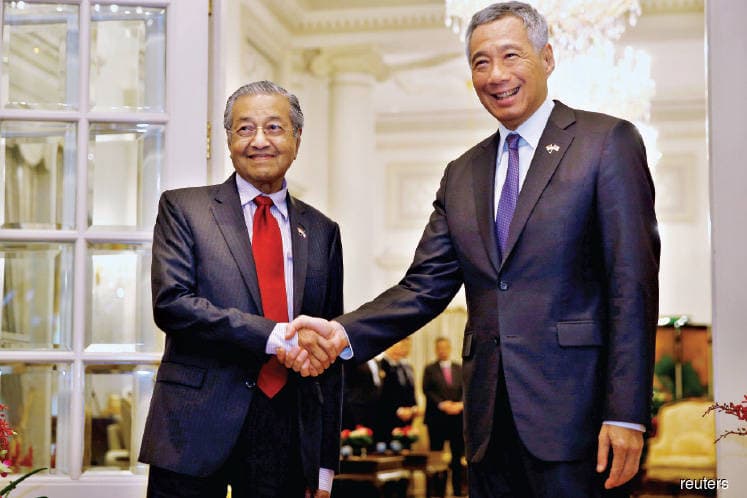

Prime Minister Tun Dr Mahathir Mohamad and his Singaporean counterpart Lee Hsien Loong will meet at the 9th Singapore-Malaysia Leaders’ Retreat in Putrajaya on Monday and Tuesday.

The retreat was supposed to be held last November but was postponed. Bilateral issues to be resolved between the two countries include airspace and maritime border disputes as well as the recurring issue of the price at which Malaysia supplies water to Singapore.

Last Friday, Mahathir said at a press conference that all “unresolved” matters between Malaysia and Singapore will continue to be discussed at the upcoming leaders’ retreat.

Given the significance of the two countries in the Asean region, investors will be closely tracking any developments at the meeting.

The Monetary Authority of Singapore (MAS) will be releasing its latest monetary policy statement on Friday, together with the advance gross domestic product estimate for the first quarter.

In view of the current global economic slowdown, the consensus expectation is that monetary policy will remain unchanged in April while growth for 1Q2019 is expected to slow. It is worth noting that MAS tightened its monetary policy last April.

Key economic data releases include China’s March trade data on Friday, which is among those that investors will be monitoring after China’s Purchasing Managers’ Index (PMI) unexpectedly jumped to 50.8 for March. A reading below 50 signals contraction while a reading above that indicates expansion. Investors will be watching to see if the expansion translates into stronger export numbers for the month.

Other data includes China’s March Consumer Price Index (CPI) and Producer Price Index (PPI), which will be out a day before the March trade data is released.

Investors will also be looking at some of the data, including money supply M2 (M2 typically includes all elements of cash and checking deposits as well as “near money”, which refers to saving deposits, money market securities, mutual funds and so on) as well as data on aggregate financing, which will be out on Wednesday.

Over in Europe, Brexit will continue to dominate the headlines with the emergency European Union (EU) summit on Wednesday. European Council President Donald Tusk had called for the summit after MPs in the UK rejected Prime Minister Theresa May’s Brexit deal on March 29.

It will be interesting to see how developments will unfold. If a request for an extension is not granted, it will lead to a no-deal Brexit on April 12. May has until April 10 to discuss some sort of an agreement on a revised Brexit deal with Labour opposition leader Jeremy Corbyn.

If a deal is agreed upon, it will enable the UK to leave the EU on May 22, a day before member states elect new members of the European Parliament.

It is worth noting that last Friday, May formally requested more time to plan the UK’s exit, until June 30, and admitted that the UK is preparing to participate in the upcoming EU elections.

Nonetheless, another extension is not guaranteed. If it happens, a no-deal Brexit will see the UK crash out from the EU, which could lead to a crisis. However, most investors are expecting an extension beyond April 12.

The emergency summit is likely to overshadow the European Central Bank’s (ECB) monetary policy decision, which will be held on the same day. With Brexit on the horizon, ECB is unlikely to make any changes to its monetary policy.

Investors will also be keeping tabs on the Federal Open Market Committee (FOMC) minutes on Wednesday. The US Federal Reserve’s dovishness in March surprised the equity market, giving it a lift, with the median consensus being no further rate hikes for this year.

It will be interesting to see what the next move is for the Fed, given the noise surrounding a potential interest rate cut as well as details on the balance sheet reduction programme.

The US-China trade talks will also be on the radar of investors, who will be looking for any signs of a deal with both countries become more positive.

US President Donald Trump and China’s President Xi Jinping have publicly hailed substantial progress in the trade talks. While no firm date has been given for a Trump-Xi summit, it is possible that we will be hearing more updates from the two countries, especially on some of the more difficult issues.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.