This article first appeared in The Edge Malaysia Weekly on April 25, 2022 - May 1, 2022

JUST last week, the International Monetary Fund (IMF) said that it expects global economic growth to slow significantly this year as the effects of the war in Ukraine spread to the rest of the world. The international body revised downward its global growth forecast for the year to 3.6% from a 4.4% forecast made in January.

The war in Ukraine, which has lasted for nearly two months, does not show any sign of easing. In fact, it is said to be intensifying as Russia launches attacks on Ukraine’s Donbas region. Economies around the world have only just emerged from the Covid-19 pandemic and are now battling rising inflation.

Undoubtedly, the war will make it more challenging to get economic growth back on track.

While the war in Ukraine has had no direct impact on Malaysia, some believe that the second-order impact has now emerged, following the expansion of sanctions on Russia by the Western nations and Russian President Vladimir Putin’s vow to press on until his goals are achieved.

The second-order impact refers to how Malaysia would be affected by higher cost pressures and through indirect trade channels, says UOB Malaysia senior economist Julia Goh, especially if growth prospects of its key trading partners like the US, European Union (EU) and China are impacted from the heightened geopolitical risks.

“Given that Bank Negara Malaysia forecasts for Malaysia’s [economic growth] assume global growth between 3.8% and 4.3%, there are downside risks [to the country’s GDP growth],” she observes.

The central bank’s gross domestic product growth forecast of between 5.3% and 6.3% in 2022 is slightly lower than the government’s official forecast of 5.5% to 6.5%.

According to Associated Chinese Chambers of Commerce and Industry of Malaysia’s Socioeconomic Research Centre executive director Lee Heng Guie, Bank Negara’s projected growth is largely anchored on a stronger revival in domestic demand, especially from private consumption, and public investment.

He adds that slower-than-expected consumer spending due to inflation and cost of living concerns as well as slow job creation and weak improvement in income growth would exert risk on expectations of stronger economic traction.

“There is a 35% chance of GDP coming in at the lower end of the range estimation,” he says.

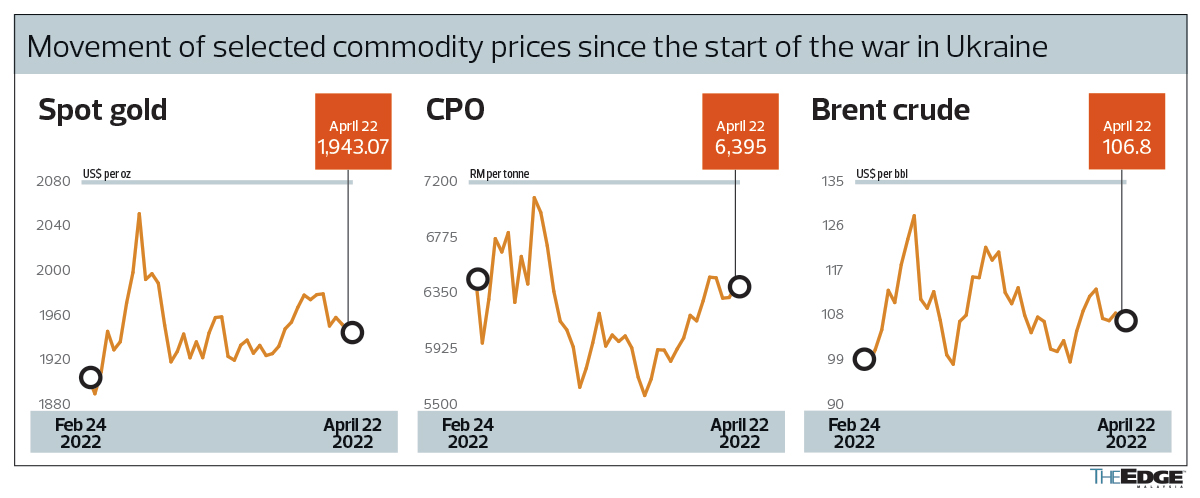

The concern now for Malaysia, he opines, is on its external sector, how a potentially sharp global economic slowdown due to persistent negative shocks and supply chain disruptions, higher and protracted inflation, tighter global monetary policy in the US as well as slower growth in China would dampen exports, even amid higher crude oil and palm oil prices.

Yet, others remain hopeful. Sunway University economics professor Dr Yeah Kim Leng believes the country’s transition to endemicity since April 1, with borders reopening and the normalisation of social and economic activities, may boost domestic demand sufficiently to offset the deterioration in the external environment.

“The fiscal spending boost from an expansionary budget together with a pickup in the implementation of infrastructure projects and approved capital investment projects would complement the release of pent-up consumption that may be large enough to sustain growth within the projected range,” he says, adding that the second-quarter growth performance will be the bellwether of whether the lower end of the growth forecast range would need to be marked down.

So far, early indicators published show some promise of growth for 1Q2022. Industrial output grew 4.1%, with manufacturing expanding a healthy 6% year on year in the first two months of the year. Wholesale and retail trade rebounded strongly to an average of 8% for the first two months compared with a contraction of 1.7% in the same period in 2021.

Total trade has also expanded 21.4% for the first two months, compared with 9.1% in 2021.

Lee estimates that 1Q2022 GDP will come in at 4.6% y-o-y.

Furthermore, he adds that the most recent Employees Provident Fund (EPF) withdrawals totalling RM40 billion, where an estimated 40% will be used for essential expenditure and festive celebration spending, is expected to lift domestic demand in April and May.

Having said that, businesses face some challenges with increased production and operating costs as worker shortages and supply disruptions are expected to impact business capital spending. Some companies are also constrained by limited working capital amid soaring raw material prices.

So far, the pass-through from the rise in producer prices and import prices to consumer price inflation has been muted given how the government has been managing price controls of essential items.

“The government seems to be taking a stronger approach in managing the risks coming from imported inflation. Subsidies remain generous and that limits the rise in inflation relative to other countries and also minimises the negative impact on consumers’ purchasing power.

“On top of that, the high commodity prices bring benefits to commodity producers, leading to higher profit to producers and smallholders,” says CGS-CIMB Research head of economics Ahmad Nazmi Idrus.

Malaysia’s inflation for March increased 2.2% from a year earlier, similar to February. The main driver of inflation in March was the 4% increase in the food and non-alcoholic beverages segment, as prices of food items including chicken and vegetables spiked more than 10%.

Global stagflation risk increases

Economists agree that the risk of global stagflation has definitely risen, with threats of slowing global growth amid rising inflation as commodity prices soar.

Nazmi says the possibility of global stagflation should not be discounted, given consumers in countries that face high inflation, such as the US and UK, have started to cut down on non-essential spending, potentially leading to slower growth.

“However, markets have been saying that the recent inflation data from the US may have reached its peak. If this is true, then we might see wages catching up to inflation growth and likely start to see rising spending again,” he adds.

In the US, the March Consumer Price Index increased 8.5% from a year ago, the fastest climb the country has seen since 1981.

Lee warns that the risk of monetary policy mistakes in balancing between supporting the growth and taming inflation could cause the next recession in the US economy.

“Past episodes of inflation shock suggest that the US Federal Reserve will face a daunting task in tightening monetary policy aggressively to cool inflation without causing a US recession,” he adds.

Meanwhile, Goh believes that slower global growth and elevated inflation are probable whereas stagflation risk will depend on the impact of higher inflation on consumers’ purchasing power and investments, on top of the impact of the withdrawal of monetary and fiscal stimulus.

But for now, indicators from the US remain robust, particularly the labour market, highlights Goh. She observes that the average US business cycle expansion averages 43 months while the current expansion is at 25 months, suggesting that there is still room for growth this year.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.