This article first appeared in Forum, The Edge Malaysia Weekly on October 10, 2022 - October 16, 2022

US Federal Reserve chair Jerome Powell recently hiked the US fed funds rate by 75 basis points (bps) to 3%-3.25%, and signalled that by the end of the year, the central bank is targeting an interest rate of 4.5%. This means that another 125bps of interest rate hikes are in the offing. Powell went on to say that the final target is to bring inflation down to 2%, from August 2022’s 8.3% year on year. That presages some very vigorous movements for the US dollar, and some rather bleak outlooks for other currencies that do not act to preserve the value of their currencies.

The current downswings of the ringgit against the US dollar have many worried how long it will last and how much their lives will change. Thoughts of whether they would be shoved into poverty, hunger or hopelessness have popped up in their minds.

Why would a currency like the USD have so much sway on the lives of Malaysians? Based on European Central Bank (ECB) data in 2021, the USD is the currency in roughly 40% of all trade invoices globally. Former prime minister Tan Sri Muhyiddin Yassin was recently quoted as saying the food import bill for last year was

RM63 billion. One can do the math easily and find that upward changes in USD would lead to higher costs of food in Tanah Airku. This was evidenced recently by the crisis in the price of chicken in Malaysia (sparked by the cost of feed, which is 100% imported) and of broad-based food inflation. What is worse is that, it is not a one-off event: Russia’s unwarranted aggression against Ukraine has pushed wheat and corn prices into the stratosphere, and oil and gas prices teeter on the brink of another flight with winter approaching in the northern hemisphere and Russian supply sanctioned. This is on top of a four-year drought in South America, big exporters of grains and feeds to the world.

With all this doom rolling in like a killer tsunami, thoughts and actions must now turn towards defending the rakyat. In our last article (“Taming the volatility of the ringgit”, Issue 1439, Sept 19), we pointed out that Bank Negara Malaysia has done well in managing foreign exchange risks for itself, but now we must ask whether we have the experience to handle what is happening in the US economy as the consequences hit the rakyat.

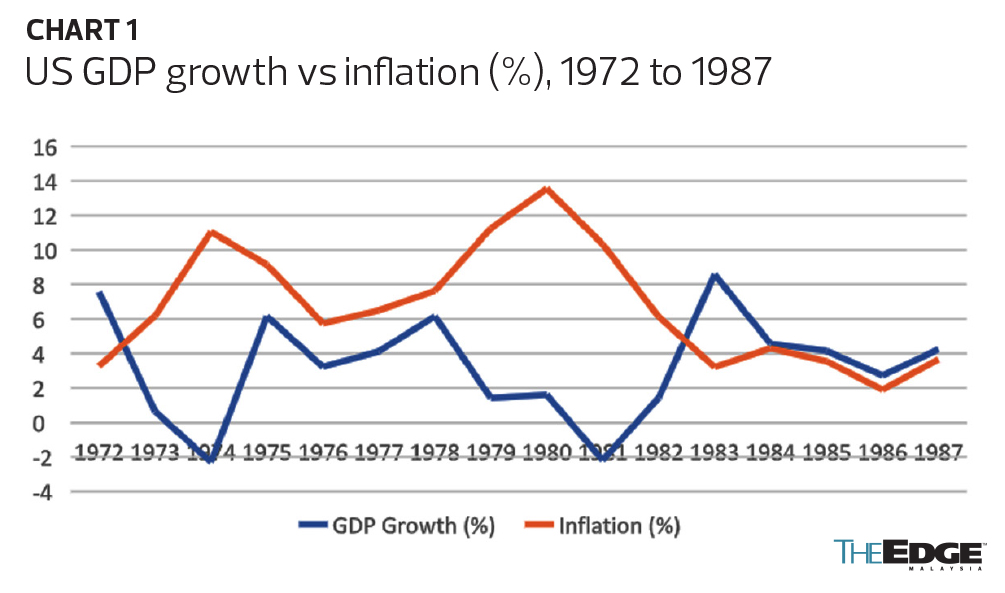

What is happening to the US economy is a major fight against stagflation. In the 1970s and 1980s, the US had a major battle against stagflation that is eerily similar to what is happening today. In that episode, lasting 16 years, the US had emerged from the Vietnam War and the huge amount of wartime spending that was needed was in their economy. They were forced to abandon the Gold Standard, and the oil crisis happened, sending inflation zooming upwards and gross domestic product skidding downwards (see Chart 1).

The data range we chose was from 1972, a year before the oil crisis, to 1987, when the US stock market crashed on Black Monday, changing economic fundamentals substantially. Some datapoints popped out:

1. The US Consumer Price Index (CPI) went from 3.27% in 1972 to a high of 13.55% in 1980, dropping to below 2% a year before the 1987 crash.

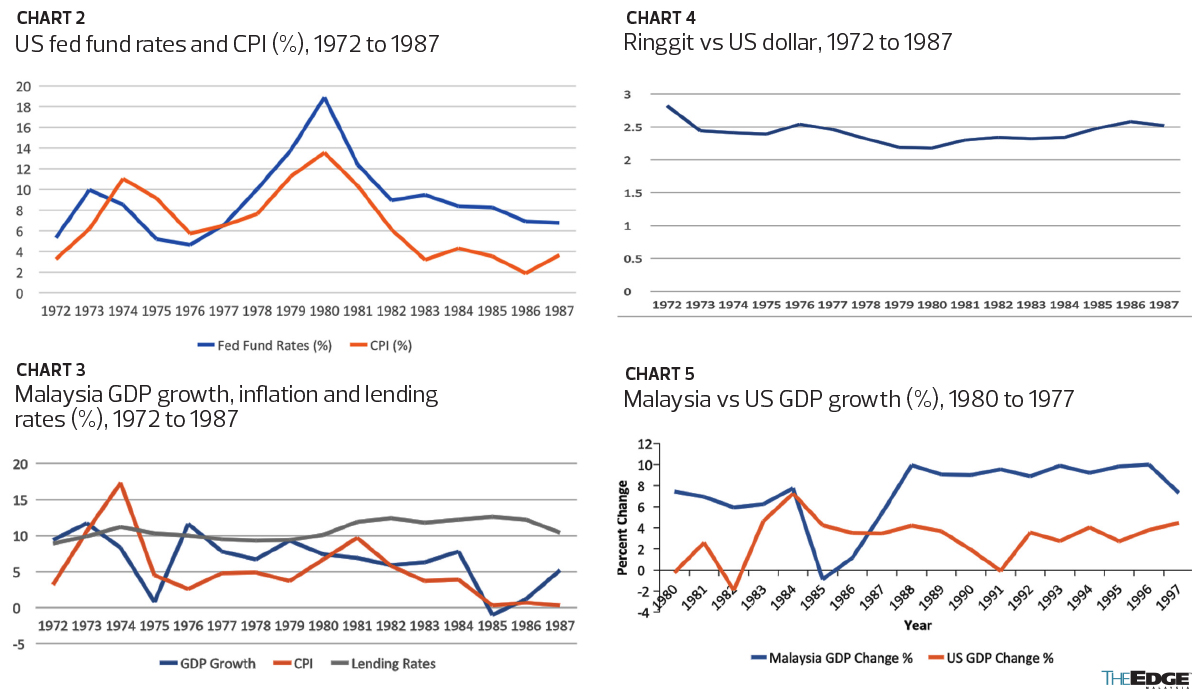

2. US interest rates, using fed fund rates, started at 5.33% in 1972 before going as high as 18.9% in 1980 and thereafter falling to 6.77% in 1987 (see Chart 2).

This entire stagflation episode took 16 years to fight. This was not a sprint but an ultra-marathon. The current one looks likely to be another long battle, too.

How did Malaysia do during this period?

Malaysia started the period already at high interest rate levels and kept them high throughout the period, with a peak of 12.4% in 1982. This seems to say we were fighting two different crises, one before the period and one during. Further, inflation started at 3.2% in 1972, hit a high of 17.3% in 1974, and ended at 0.3% in 1987, which indicated overkill, as Malaysia’s GDP dropped from 7.8% in 1984 to a -1% recession in 1985, kicked along by severe drops in rubber and tin prices, two commodities forming the bulk of Malaysia’s export earnings then (see Chart 3).

As one can see in Chart 3, Malaysia’s interest rates were in the double digits from 1980 to 1987 (and skirting around 10% in the years before) while from 1982, the US’ trended downwards from under 10% to 6.77% in 1987.

Despite the higher interest rate posture by Malaysia, the ringgit actually fell against the USD in the period from 1980 to 1987 (see Chart 4).

This seems to say that if another country’s economy doesn’t recover as fast or policy action meant for another purpose is lagging in ending or even implementation as the case may be, then that country’s currency (herein ringgit) will lose value against another’s (herein USD).

However, Chart 5 added mystery to the whole thing. Basically what it says is that the US and Malaysian economies were countercyclical to each other but, given what happened, counter-intuitively, Malaysia was not immune to what was happening in the US and the transmission of higher inflation through its causes did happen and Malaysia was hit as well.

Nowadays, as we have argued several times before, things have changed. Due to Malaysia pegging the ringgit to the USD in 1998, our economy is pro-cyclical with the US’ as Chart 5 shows.

Does this mean this time, Malaysia will be hit worse?

Huzaime Hamid is the chairman and CEO of Ingenium Advisors Sdn Bhd, a Malaysian financial macroeconomics advisory company

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.