This article first appeared in The Edge Financial Daily, on April 20, 2016.

Sunway Construction Group Bhd

(April 19, RM1.57)

Maintain buy with a higher target price (TP) of RM1.98: Sunway Construction Group Bhd (Suncon) was awarded the RM1.2 billion Klang Valley mass rapid transit line 2 (MRT2) project on March 29 this year.

This lifts its order book to RM4.8 billion, equivalent to 2.5 times financial year 2015 (FY15) revenue, improving earnings visibility.

We see prospects for more contract wins as Suncon has submitted tenders worth RM18 billion for highway and building projects.

We lift our realisable net asset value-based TP to RM1.98 from RM1.74 to reflect a higher sustainable construction earnings assumption.

Suncon remains our top buy in the construction sector.

Suncon won the tender for viaduct guideway package V201 (Sungai Buloh-Persiaran Dagang stretch) of MRT2 for RM1.21 billion due to its competitive price and strong technical capabilities.

Suncon expects a 10% profit before tax (PBT) margin for this project with a construction period of five years. It plans to bid for the station works worth about RM300 million within the package to improve its profit margin from this project.

Suncon has also submitted tenders for the Sungai Besi-Ulu Klang Expressway and Damansara-Shah Alam Elevated Expressway civil work packages.

We gather that the indicative value is over RM1 billion for one of the packages. Few contractors can execute the work due to the complexity of the highly elevated highway section, and thus we see less competition.

Suncon and its local joint-venture (JV) partner KTS Holdings Sdn Bhd will also bid for the upcoming Pan Borneo Highway package in Sibu, Sarawak, worth about RM1.7 billion.

KTS owns a quarry in Sibu, improving the JV’s competitiveness for the upcoming tender.

Suncon clinched RM1.36 billion worth of new contracts in the first quarter of 2016, increasing its order book to RM4.8 billion from RM3.7 billion at end-2015.

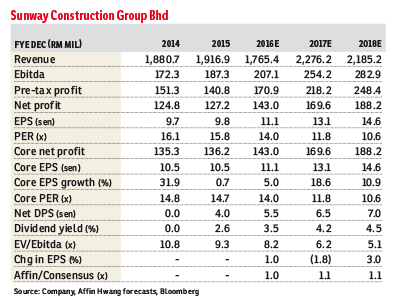

We fine-tune our earnings forecasts (+1%/-2%/+3% for FY16/FY17/FY18).

Besides, we revise upward our 2016 new contract assumption to RM3 billion from RM2 billion previously as the implementation of major public infrastructure projects accelerates.

We also raise our PBT margin assumption to 10% from 8% previously with a longer five-year construction period for the MRT2 project.

We believe Suncon’s current ex-cash FY16 price-earnings ratio of 12 times is attractive compared with its peer average of 18 times.

We maintain “buy”. Key risks are delays in the implementation of public infrastructure projects and cost overruns. — Affin Hwang Capital, April 19