KUALA LUMPUR (Sept 8): There has been a notable increase in private placement activities on Bursa Malaysia lately, as companies take advantage of ample liquidity in the market to raise cash by selling shares to pre-identified investors.

Given its faster execution process compared with other fund-raising methods, it is not surprising that private placement is the method of choice.

On the other hand, earnings dilution awaits minority shareholders as they are not included in the fund-raising process. There is also the risk of future speculation on the shares, and minority shareholders often do not know to whom the shares are placed.

Of the 79 private placements announced between Jan 1 and Sept 3 this year, 57 of them or 72.15% were announced from May onwards — when it was clear that the pandemic and the Movement Control Order it led to, would cause business disruptions.

On April 16, Bursa Malaysia also upped the private placement general mandate to 20% of a company’s issued share capital, from 10% previously. This is still lower than other countries like Hong Kong or Singapore, it said.

“The exchange recognises the need for listed issuers to resume operations and raise funds quickly and efficiently, as a means to finance their businesses and aid their recovery during these trying times,” it said, as it allowed the interim measure until December 2021.

However, few companies actually cited cash flow issues as the reason behind the placements — only 13 of the placements or 16.46% were to pay off debts.

Some 27 placements or 34.18% merely cited working capital and “future business expansion that has yet to be identified” as rationale for the fund-raising.

On the flip side, 39 of them or 49.37% clearly earmarked how the proceeds would be used, like to fund specific projects or to acquire certain machineries. Interestingly, eight companies in this category placed their shares twice this year, which would mean further earnings dilution for minorities.

But if the plan was ready and the prospects clear, why not a rights issue that would give existing shareholders the choice to participate and benefit more from such ventures? In the same period, only six rights issues have been announced as opposed to the 79 private placements.

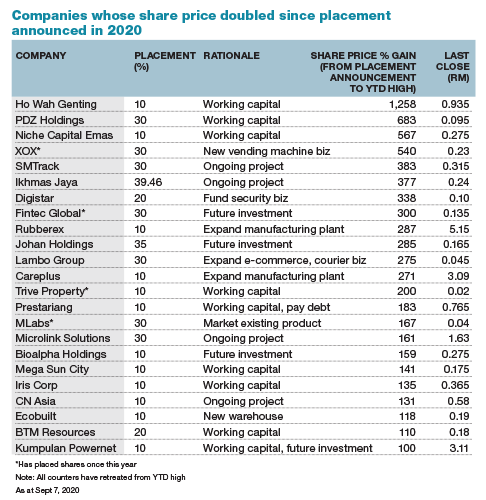

Another peculiar trend is the share price movements of these companies that have announced share placements, of which 90% are penny stocks. About half saw their share prices reach their highest this year — some hitting record highs — in the months after their respective placement announcements. For 23 of them, their share prices have at least doubled.

This was puzzling, given the fact that 18 or 78.26% of these 23 companies have been loss-making in the last 12 months, and that existing minority shareholders will lose out from the dilution.

Notably, the rise in placement activities — and the subsequent share price jumps — also come at a time of higher retail interest in the market.

“In real business, it is really difficult to ask for money from someone. How do such companies so easily get a buyer for their shares?” one investor points out to The Edge.

Balancing company needs and shareholder interests

While ambiguity in placements can put counters at risk of speculative play, there is some rationale behind the non-disclosure of the placees, said Equitiestracker Holdings Bhd head of research Peter Lim.

“There are operators [that dwell in speculative plays] but the authorities need to balance between being stringent and killing the vibrancy of the market,” Lim told The Edge.

“There are investors who wish to remain low-key, and to disclose them means risking the investment,” Lim said.

“From the regulators’ perspective, one option is to disclose the portion of institutional and private investors, for the reference of future investors,” he added.

Rakuten Trade Sdn Bhd vice president of research Vincent Lau, meanwhile, affirmed the need for private placement among troubled companies. “These are loss-making, small cap companies that may need cash fast. They may lack the track record to get adequate borrowings, so this is a good avenue for such purposes,” he said.

Existing measures are also present to control speculation, such as the suspension on short-selling and the two-day limit-up/down share price freeze, he added.

“Bursa has stated that margin financing has not reached elevated levels,” Lim said. “The market is best described as vibrant right now, not overheated.”

Other gatekeepers have to play their role

Other than regulators, minority shareholders must also safeguard themselves by equipping themselves with the necessary knowledge about the company they are investing in, said Equitiestracker’s Lim.

“Buyers beware,” he said, reminding minority shareholders to vote against the placement if there are concerns.

There is also another gatekeeper in this entire process.

“Listed issuers must disclose the views of its board of directors that the 20% general mandate is in the best interest of the listed issuer and its shareholders, as well as the basis for such views,” said Bursa Malaysia, in response to questions from The Edge.

In this regard, shareholders who have given the general mandate for such corporate activities are dependent on the integrity of independent directors to protect their interests.

"We believe that the protection of shareholders’ rights should be balanced against safeguarding listed issuers’ interest, especially in these difficult and exceptional times," Bursa said.

“Enhancing business efficacy through faster time to market for listed issuers to raise funds, is critical to ensure the long term sustainability and interest of both listed issuers and their shareholders,” it added.