This article first appeared in Capital, The Edge Malaysia Weekly on December 28, 2020 - January 3, 2021

THE selection of winners was especially tough this year, with many stocks reaching dizzying heights and mind-boggling multiples, though Malaysian stocks remain a mere fraction of the US$100 trillion that global stocks are now worth. The bellwether FBM KLCI looked set to end the year lower for a second straight year at the time of writing but reflected 23.18 times earnings — significantly higher than 17.7 times in 2019 and 21.3 times in 2018.

As many as 19 research outfits were represented in the 15th edition of The Edge Best Call Awards — the highest since the awards were started in 2005 (we skipped one year but brought back the awards because of popular demand).

We long-listed as many as 39 calls that proved right in 2020 but selected only 17 calls for 15 stocks from 131 nominations received for 90 stocks. The calls dropped from the running included stocks whose ascent, though steep, may not be sustainable. We also decided against picking winners for glove-related stocks this year but will look at them next year when the dust settles, so to speak.

The number of submissions we received for consideration was the highest since 2015, the first year The Edge opened nominations for this annual award beyond the heads of “sell-side” research outfits to the general investing public — readers of The Edge, fund managers, private investors and equity analysts themselves — for what they thought was the best “buy” or “sell” call that proved correct in 2020. Last year, 112 nominations were received from 15 research outfits for 81 stocks, compared with 82 nominations for 67 stocks in 2018, 90 recommendations for 66 stocks in 2017, and 86 nominations for 75 stocks in 2016.

The highest was 139 submissions for 102 stocks in 2015.

This year’s winners continue to include those who rightly stuck their neck out by calling an outright “sell” or “buy” against consensus and were proven right. A number of our winners this year were alone when they first made their “buy” or “sell” call. Like last year, we made some allowances for calls made in 2019 that proved right in 2020.

The awards are our best-effort attempt to recognise good fundamental stock analysis and its importance in making informed investment decisions. They are not meant to influence year-end appraisals or annual bonuses. Feedback is welcome at [email protected].

With that, here are this year’s winners — selected based on submissions and publicly available data — in no particular order. Congratulations to the winners. To the good stock pickers not recognised here, keep up the good work. Here’s wishing everyone a Merry Christmas and a Happy New Year! Stay safe and may 2021 be a better year for everyone!

Credit Suisse head of research Danny Goh’s call on Hong Leong Financial Group Bhd

When Credit Suisse’s Danny Goh reinitiated coverage on Hong Leong Financial Group Bhd (HLFG) with an “outperform” rating on June 1 this year, he told clients that HLFG was trading at a steep 32% discount to its sum-of-parts valuation of RM19.65 per share and that its life insurance business and associate stake in MSIG — which he valued at RM5.1 billion — were not reflected in its market capitalisation.

At the time, HLFG was hovering around RM13 apiece (RM15.1 billion market cap) but Goh reckons it should fetch at least RM15.70, which was his target price. Interestingly, Bloomberg data showed that one of the three earlier “buy” recommendations were cut to “hold” (to join two other “hold” calls) the day Goh reinstated coverage on HLFG following the release of its latest quarterly earnings.

While the stock slipped closer to RM12 within the first two months of the call, it was quick to more than retrace those losses — surging as much as 54% in just over three months to reach as high as RM18.68 on Dec 14. Closing at RM17.50 (RM20 billion market cap) on Dec 22, the stock was still up 35% in just under six months from June 1 — not too shabby for a large-cap stock that is only up 3.55% year to date. Goh’s target price has been increased to RM20.60 since Nov 19 this year, which reflects 17.7% upside potential if he continues to be right.

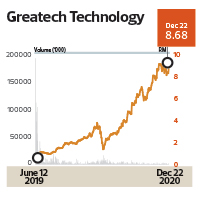

UOB Kay Hian Research analyst Desmond Chong’s call on Greatech Technology Bhd

One other analyst was already tracking Greatech Techology Bhd when UOB Kay Hian’s Desmond Chong initiated coverage on July 2 this year. His “buy” call at the time, however, was earlier than his peer’s and it proved prescient, with the stock up 261.7% year to date as it ended at RM8.68 on Dec 22 to give it RM5.4 billion market capitalisation.

When starting coverage, Chong described Greatech as having “unique positioning for the fourth industrial revolution” beyond the typical automated test equipment (ATE) manufacturers in Malaysia that are benefiting from the growth in industrial automation globally because it also automates processes in production lines.

His initial RM4.80 price target reflected 19% upside to the RM4.04 the stock was hovering at back then, but the target prices were subsequently revised higher when Greatech’s order book was bolstered by more contract wins. When upgrading his target price to RM7.60 to reflect 19% upside in mid-August, he told clients that the stock could justify a higher valuation multiple given its unique value proposition of having a strategic exposure in the solar, medical and automotive industries that offer better dynamics to weather cyclicality. His target price has been upped to RM9.90 since Nov 30 this year, which is 8.4% above the stock’s 52-week high of RM9.13 on Nov 13 and 145% above where it was when Chong started coverage just six months back in early July. Investors would likely be keeping an eye on whether Greatech can continue replenishing its order books.

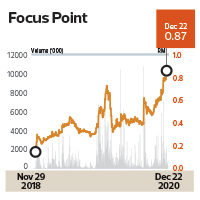

TA Research analyst Tan Kong Jin’s call on Focus Point Holdings Bhd

It is easy to miss Focus Point Holdings Bhd, whose market capitalisation stood just below RM200 million even after gaining as much as 152% this year to close at 90.5 sen on Dec 17. The stock’s rally in February was cut short in March when stocks around the world reacted to the declaration of a pandemic. Investors would have locked in most of their gains early in the year if they had followed Tan’s “sell” call on Feb 28 when the stock was at 68.7 sen. At the time, Tan told clients the stock had surged 110% since he initiated coverage in May 2019 and was already fully valued at 67 sen.

Investors would have made another round of gains if they saw the opportunity and bought the stock again when Tan upgraded the stock to a “buy” on March 30 when it was hovering at 36.5 sen, which reflected a discount of over 80% to his target price of 67 sen. At the point of his upgrade, the only other stock recommendation was a “hold”.

From there, the stock soared as much as 152% to reach as high as 92 sen intra-day on Dec 16. At the time of writing, Tan has yet to change his call, despite the stock price being 30% above his target price of 67 sen as it closed at 87 sen on Dec 22.

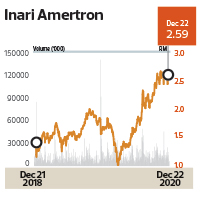

Maybank Investment Bank Research analyst Kevin Wong’s call on Inari Amertron Bhd

Shares of Inari Amertron Bhd, one of Broadcom Inc’s top OSAT (outsourced semiconductor assembly and test) providers, were up more than 52% year to date to give it a market capitalisation of RM8.5 billion. With as many as 20 analysts actively tracking the semiconductor player, it is not easy to stand out.

Yet Maybank Investment Bank Research’s Kevin Wong made more than one timely recommendation on the stock this year, putting it ahead of five other houses that submitted their call for consideration for The Edge Best Call Awards.

The first timely call was Wong’s downgrade from “hold” to “sell” on Nov 27, 2019, after Inari’s first-quarter earnings came in one-fifth below full-year forecasts. Its share price slipped nearly 40% — from RM1.80 levels in late November 2019 to as low as RM1.09 on March 19 this year — before rebounding. The rebound came just three days after Wong’s upgrade of Inari to “buy” from “sell” on March 16. His RM1.50 target price had implied 39% upside potential, with Inari shares hovering around RM1.08 back then. Closing at RM2.59 on Dec 22, there is still 31% upside potential to Wong’s target price of RM3.40 if he continues to be right.

Hong Leong Investment Bank Research analyst Gan Huan Wen’s call on Lii Hen Industries Bhd

Malaysian furniture companies were seen as among the beneficiaries of a shift in supply chain as a result of US-China trade tensions. But what makes Lii Hen Industries Bhd worth an even closer look is its net cash position and dividend-paying capability. While Hong Leong Investment Bank’s (HLIB) Gan Huan Wen probably inherited coverage of Lii Hen from the HLIB analyst who unearthed the stock in September 2017 (Rachel Hong), investors who heeded Gan’s recommendation the past year would have profited handsomely.

Closing at RM3.87 on Dec 22, Lii Hen shares were up 26% year to date and had gained 146.5% over nine months, if measured from their 52-week low of RM1.57 on March 19 this year — and that’s just the share price appreciation.

Noting how Lii Hen’s net cash position had risen from 84 sen per share as at end-December 2019 to 88 sen per share as at end-June and 96 sen per share as at end-September, Gan expects Lii Hen to pay a dividend per share of 16.5 sen in FY2020 and 20 sen per share in FY2021, which reflects a 5.17% yield at the time of writing. On Nov 17, Gan raised the target price from RM4.08 to RM4.96 after increasing sales and earnings forecasts following the delivery of higher-than-expected earnings. That implies 28% upside potential if Gan continues to be proven right.

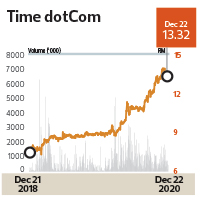

AllianceDBS Research analyst Toh Woo Kim’s and Credit Suisse analyst Danny Chan’s calls on Time dotCom Bhd

It is perhaps little wonder that shares of Time dotCom Bhd are up 48% year to date, with providers of fixed broadband seen as among the beneficiaries as Covid-19-related movement restrictions made it necessary for many to work and study from home. The stellar gains made it the best-performing Malaysian telecoms stock, piping gains seen at incumbent Telekom Malaysia Bhd, while larger capitalised mobile peers skidded.

Of the four submissions on Time dotCom for the awards, the calls by AllianceDBS’s Toh Woo Kim and Credit Suisse’s Danny Chan were among four jointly ranked for top place by Bloomberg, alongside Macquarie Research’s Prem Jearajasingam and BIMB Securities’ Afifah Abdul Malek. They are among seven analysts who still have a “buy” recommendation while three houses (UOB KayHian, Maybank and RHB Research) have downgraded their calls to “hold”, according to Bloomberg data.

Toh and Chan have target prices of RM16 while Macquarie is the most bullish at RM16.70. Those with “hold” recommendations have target prices ranging between RM13 and RM13.70, which implies limited upside from the stock’s RM13.32 closing on Dec 22. It would be interesting to see who will be proven right next year.

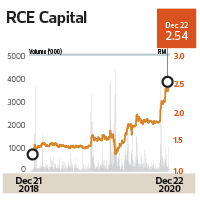

Maybank Investment Bank Research analyst Yin Shao Yang’s and Rakuten analyst Yong Jun Ting’s calls on RCE Capital Bhd

Investors who bought shares of RCE Capital Bhd would have gained a rare combination of decent dividend yield as well as good capital appreciation with the stock price up 53.9% at its Dec 22 closing of RM2.54.

While it was Maybank Investment Bank Research’s Desmond Ch’ng who first initiated coverage on RCE Capital back in September 2016, investors would have benefited from analysis by Yin Shao Yang, who took over coverage from Nov 6, 2019, when the stock price hovered around RM1.45. It was only in FY3/2020 that net profit exceeded the RM100 million mark and the dividend payout ratio began to rise again. RCE Capital, which provides personal financing, including to civil servants, is also enjoying cheaper cost of funds, thanks to the low interest rate environment.

Similarly, Rakuten has maintained a “buy” call on RCE Capital since initiating coverage on Oct 29, 2019, highlighting to clients the latter’s defensive value proposition and decent asset quality. Its target price was RM2.39 as at Oct 8 while Maybank’s was RM2.09 as at Nov 11.

A special mention also goes to KAF Seagroatt & Campbell’s Izzul Hakim Abdul Molob and RHB Research’s Liew Wai Hoong. Izzul has had a “buy” call on RCE Capital since Jan 3, 2018, and a RM2.30 target price as at Aug 18, according to Bloomberg data. Liew, who started coverage on Jan 10, has the most bullish target price of RM2.80 — the only one that had not been exceeded at the time of writing.

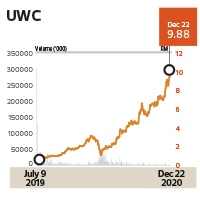

Hong Leong Investment Bank Research analyst Tan J Young’s call on UWC Bhd

The meteoric rise in UWC Bhd’s share price is just jaw-dropping. More so if you are looking at a two-year horizon.

UWC made its debut on Bursa Malaysia’s Main Market in July 2019, at an adjusted initial public offer price of 55 sen. About 18 months later, the share price closed at RM9.88 on Dec 22 — 18 times its IPO price.

For the year to Dec 22, the stock had rallied 363%. The market price has exceeded Hong Leong Investment Bank Research analyst Tan J Young’s target price of RM8.88. During the year, he had raised the target price substantially from RM2.59 in March as the company’s earnings growth gained momentum.

UWC’s quarterly net profit has increased sequentially since it started reporting results for the financial quarter ended April 30, 2019 (3QFY2019). Its quarterly net profit leapt from RM8.82 million in 3QFY2019 to RM21.7 million in 1QFY2021.

Tan is one of two analysts who track UWC, which specialises in the provision of precision sheet metal fabrication and value-added assembly services as well as the fabrication of precision-machined components. The company mainly serves the semiconductor, life sciences and medical industries.

“The escalating [US-China] trade intensity may eventually benefit UWC, which provides a one-stop solution, as more companies shift productions out of China to avoid import tariffs,” Tan wrote in his research note.

A notable mention goes to Nomura’s Kong Heng Siong, who also has a “buy” call on the stock, with an even higher target price of RM10.

AmInvestment Bank Research analyst Jeremie Yap’s call on CSC Steel Holdings Bhd and Scientex Bhd

The steel sector has been off investors’ radar screens due mainly to the structural issues that it is facing such as the flood of cheap imports eating into their profitability.

Still, AmInvest analyst Jeremie Yap managed to find a gem in CSC Steel Holdings Bhd. About a week after the flat steel product maker’s share price plummeted to an all-time low of 50.3 sen on March 23, he made a “buy” call on the stock, with a target price of RM1.09.

Earnings-prospects-wise, Yap had his reservations on CSS Steel amid the disruption brought about by the Movement Control Order (MCO) and the expected weak demand due to the pandemic. Nonetheless, he saw it as a dividend play that offered a high yield of 7% after the sharp fall in share price made the stock attractive in March, given its cash-rich balance sheet.

CSC Steel’s share price rebounded from its trough and climbed to a 2½-year high of RM1.29 on Dec 16, exceeding Yap’s target price.

While many companies are suffering from cash flow problems during the pandemic, CSC Steel’s cash pile has grown, although its net profit shrank 44% to RM15.57 million for the nine months ended Sept 30, from RM27.7 million. The company’s net cash balance increased to RM307.6 million or 83.3 sen per share, which seems to have put it in a good position to declare a generous dividend.

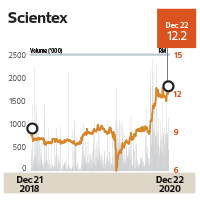

AmInvest’s Jeremie Yap isn’t the first analyst to discover this stock. Nonetheless, the “buy” recommendation that was made on Sept 16 was just in time to ride the second leg of the rally that lifted Scientex Bhd’s share price to a record high of RM12.50 in December.

In roughly three months, investors would have made a capital gain of 36% — a considerably handsome return considering that the company has a market capitalisation of more than RM10 billion — if they had followed Yap’s recommendation. He believed that Scientex would be a good proxy to the growth in global demand for fast-moving consumer goods packaging materials.

To improve its liquidity, Scientex undertook a two-for-one bonus issue plus a free issue of warrants on the basis of one warrant for every five existing shares. This gave the company’s share price a strong boost.

It is worth noting the early birds who advised their clients to add the stock to their portfolios when Scientex tumbled to a four-year low of nearly RM6 in late March. They include Jeff Lye of TA Securities, the UOB Kay Hian team, Brian Yeoh of Affin Hwang and Damia Othman of Kaf Seagroatt & Campbell, according to Bloomberg.

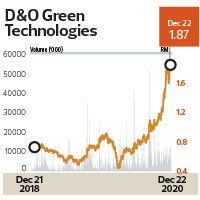

Kenanga Investment Bank Research analyst Samuel Tan and Public Investment Bank Research analyst Chong Hoe Leong’s calls on D&O Green Technologies Bhd

D&O Green Technologies Bhd is not a rubber glove stock, yet its share price has shot up more than four times to an all-time high of RM1.93, after plunging to a year low of 44.8 sen.

PublicInvest’s Chong Hoe Leong and Kenanga Research’s Samuel Tan are the two analysts in town who spotted this gem. They upgraded D&O Green to their “buy” lists in February on the grounds that the automotive LED maker’s orders were picking up and the company was gaining market share in the automotive industry.

Although consumers have tightened their belts as the Covid-19 pandemic has taken a heavy toll on the global economy, surprisingly automotive sales have been better than expected, particularly in China. Hence, D&O Green’s earnings have been rather resilient, with its net profit barely shrinking 8% to RM19.3 million for the nine months ended Sept 30, from RM21 million in the previous corresponding period. Revenue grew marginally to RM366.2 million from RM353.8 million.

Tan revised upwards his target price thrice — to 91 sen in February, RM1.20 in August and RM2 on Nov 25 — as the increase in D&O Green’s share price had gathered steam since late March. Meanwhile, Chong raised his target price to 89 sen in February, RM1.14 in August and RM1.88 in November.

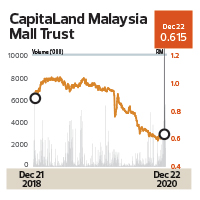

RHB Research analysts Loong Kok Wen and Raja Nur Aqilah Raja Ali’s call on CapitaLand Malaysia Mall Trust

Real estate investment trusts (REITs) are usually perceived as a vehicle for investors to seek shelter in when the economic climate turns harsh.

But RHB Research analysts Loong Kok Wen and Raja Nur Aqilah Raja Ali know quite well that not all REITs are the same. The duo told their clients to offload units in CapitaLand Malaysia Mall Trust (CMMT) in October 2019, when the shopping mall REIT was trading at slightly below RM1. They reiterated their “sell” call in January as they anticipated that pressure was mounting on the REIT’s occupancy rate and rental, noting that the group’s shopping malls in the Klang Valley were not faring well.

The unit price of CMMT lost its footing in February, even before the outbreak of Covid-19 in Malaysia. The REIT continued to slide although the local bourse staged a strong V-shaped rebound after the global equity rout subsided in late March.

Their recommendation was timely. The Covid-19 pandemic that resulted in a drastic drop in footfall at shopping malls has made the REIT’s earnings prospects even gloomier. CMMT fell to a low of 59 sen per unit on Nov 11. As at Dec 22, it had shed 37.5% year to date to 61.5 sen.

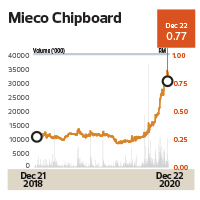

UOB Kay Hian Research analyst Jack Goh Tooan Orng’s call on Mieco Chipboard Bhd

Like furniture companies, particle board makers such as Mieco Chipboard Bhd are also seen as beneficiaries of trade diversions owing to US-China tensions. Demand also rose as more people worked from home.

Investors who paid attention when UOB Kay Hian’s Jack Goh said, in a furniture sector note, that Mieco was worth at least 48 sen, when the shares were at 34 sen on Sept 7, would have enjoyed the 154% share price appreciation in just three months. Mieco shares closed as high as 86.5 sen on Dec 15.

While the share price had run ahead of the 55 sen apiece that Goh said Mieco was worth in a Nov 3 note, he had yet to revise his recommendation at the time of writing. “Mieco is a clear winner in the particle board segment, despite the over 40% share price appreciation since our last report two months ago. Besides nursing itself back to high profitability, Mieco is on course to restructure some of its short-term debts for a healthier balance sheet,” Goh wrote in the Nov 3 note.

We acknowledge this call for the stellar returns and Goh as the only analyst actively tracking the stock, according to data on Bloomberg at the time of writing.

TA Research analyst Wilson Loo Jia Chern’s call on Unisem (M) Bhd

With hindsight, many may deem “buy” calls on semiconductor stocks as something of a no-brainer, going by how well technology stocks are doing globally. Yet TA Research’s Wilson Loo deserves a pat on the back for being the first to upgrade Unisem to a “buy” on Nov 4, 2019, with a RM2.75 target price when the stock price was RM2.28. At the time, all nine other analysts covering the stock had a “sell” recommendation.

The upgrade from “hold” to “buy” followed a selldown, “which has presented improved upside potential”, Loo told clients in a Nov 4 note. At the time, he also expected the closure of Unisem’s loss-making operations in Batam Island, Indonesia, to offload the long-standing drag on earnings.

While Unisem skidded to as low as RM1.53 in March this year following wide-ranging sell-offs when the Covid-19 pandemic was declared, investors who bought the stock in November 2019 would have profited handsomely as the share price tripled in just over a year to close as high as RM6.80 on Dec 18, before retracing to RM6.10 on Dec 22.

Loo — who retained his “buy” call and RM6.52 target price on Dec 14 when the stock closed at RM5.77 — is ranked first among nine analysts tracking the stock, according to Bloomberg data at the time of writing.

BIMB Research analyst Afifah Abdul Malek’s call on GHL Systems Bhd

While her peers had downgraded GHL Systems Bhd amid concerns about its profit margin and high valuation, BIMB Research analyst Afifah Abdul Malek not only maintained her “buy” call but also raised her target price to RM2.15. Her bullish view on the company was simply because of Bank Negara Malaysia’s efforts to increase cashless payment transactions.

“We remain positive on GHL’s long-term business prospects amid continuous efforts by the government to adopt digital payments as well as a rise in the contactless payment trend,” Afifah wrote in her quarterly results review in November.

Judging by GHL’s share price performance this year, Afifah’s “buy” call seems to have been proved right. The stock has doubled since the start of the year, from 90 sen to RM1.80 on Dec 22. It hit a record high of RM2.12 on Dec 2.

The Covid-19 pandemic has expedited the migration to cashless payments due to an increase in online shopping and for hygiene reasons. GHL, which specialises in cashless payment solutions, is riding high on the migration that has helped to mitigate weaker consumer spending. The company’s transaction processing value (TPV) for e-pay and card payment services recorded the highest value in the third quarter ended Sept 30 at RM1.1 billion and RM4.7 billion respectively.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.