This article first appeared in Capital, The Edge Malaysia Weekly on July 26, 2021 - August 1, 2021

Automotive sector — overweight

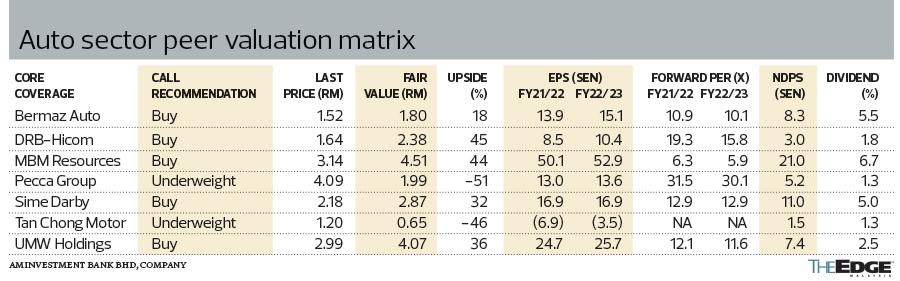

MBM Resources Bhd

AMINVESTMENT BANK (JULY 19): We remain “overweight” on the auto sector with an unchanged total industry volume (TIV) projection of 575,000 units (+9% y-o-y growth) for 2021. We expect TIV growth in 2H21 to be supported by a sustained strong performance of national marques, namely Proton and Perodua, owing to the more attractive pricing and value proposition for their products in the domestic auto market.

We expect the auto sector to resume operations (assembly, manufacturing and reopening of showrooms) in either July or August as the nation gradually moves from Phase 1 of the National Recovery Plan. With the acceleration of the vaccination drive and gradual easing of the stringent measures in phases, we anticipate consumer spending (on big-ticket items such as passenger vehicles) to remain robust in 2H21, with sentiment gradually improving. The Sales and Services Tax (SST) exemption — 100% and 50% on locally assembled and fully imported car models respectively — has been extended until Dec 31, 2021, and we believe this will continue to spur vehicle sales until the end of the year.

We are expecting a strong finish to the year as auto players usually offer additional promotional discounts or cash rebates for year-end clearance and the festive season in 4Q21. Also, consumers would want to lock in their purchases to enjoy the reduction in car prices ranging from 1% to 6% — depending on car models — from the SST exemption until year end.

Potential risks that could prompt a downgrade to the sector are: (1) a rise in the number of new Covid-19 cases, which will prolong the lockdown; (2) heightened global trade tensions, which could lead to a steep weakening of the ringgit against the US dollar, compressing companies’ margins and requiring a hike in car prices to maintain profitability levels; and (3) a tightening by banks on vehicle financing, which will directly constrain auto demand.

Our top pick is MBM Resources Bhd (fair value: RM4.51/share) and DRB-Hicom Bhd (FV: RM2.38/share). We also have a “buy” call on Bermaz Auto Bhd (FV: RM1.80/share), Sime Darby Bhd (FV: RM2.87/share) and UMW Holdings Bhd (FV: RM4.07/share).

Malayan Banking Bhd

Target price: RM9.40 BUY

HONG LEONG INVESTMENT BANK RESEARCH (JULY 21): After listening to more of Maybank’s sustainability efforts and environmental, social and governance (ESG) transformation journey during its virtual Investor Day recently, it further reaffirms our view and analysis that it is a leader in this space. Basically, the game plan is to develop sustainability-focused products and services, foster financial inclusion, cultivate good governance practices and to shy away from ESG-vulnerable sectors. At end-March, 5.4% of its loan exposure was classified as ESG-vulnerable sectors: palm oil (2.3%), forestry and logging (0.7%), coal (0.2%), oil and gas (2%) and mining (0.2%).

Maybank is looking to: (i) mobilise RM50 billion in sustainable finance (includes direct lending or investment and services, which will integrate ESG criteria); (ii) improve the lives of one million households across Asean (providing greater financial inclusion for vulnerable communities); (iii) achieve carbon neutral (own emission) and net zero carbon equivalent positions (direct and indirect COe) by 2030 and 2050 respectively; and (iv) shaping a sustainability culture among employees. The progress of these key performance indicators will be monitored by an enhanced exco sustainability committee and newly formed board sustainability committee.

Tenaga Nasional Bhd

Target price: RM13.40 ADD

CGS-CIMB RESEARCH (JULY 19): From the recent ESG engagement session with Tenaga’s management, we gather that investors’ major concerns are the group’s carbon emissions, the affordability of electricity access and the government’s growing emphasis on environmental sustainability. Tenaga is currently working on its sustainability pathway, which is expected to be announced in 2H21, where more details such as its long-term commitments and key performance indicators to monitor its sustainability performance annually could be disclosed.

The majority of investors are constantly engaging with Tenaga to understand its efforts to address the ESG issue; only a few funds are shying away due to the group’s coal-related exposure. Tenaga is ranked average among its regional peers and slightly slower than some of its leading peers in terms of ESG progress due to its business model, where it has to balance sustainability, affordability and security of the electricity supply. Tenaga has set up a dedicated team and hired external consultants to specifically look at ESG issues and identify business opportunities (such as batteries) from energy transition.

Tenaga is proposing a regulated capital expenditure (capex) of RM25 billion for the upcoming regulatory period 3 (RP3, 2022-2024), which is higher than RP2’s approved capex of RM19 billion, with more regulated capex to be allocated to facilitate energy transition (from RP2’s 12% of total capex to 19% for RP3).

Digi.Com Bhd

Target price: RM4.30 HOLD

MAYBANK INVESTMENT BANK RESEARCH (JULY 19): Digi’s 2Q21 net profit of RM280 million (-3% y-o-y, +6% q-o-q) brings 1H21 net profit to RM545 million (-12% y-o-y) — 47% of our and consensus full-year forecasts. Revenue in 2Q21 was supported by the government-led data/device subsidy programme (Prihatin) for the B40 segment, without which a sequential contraction could have occurred. A second interim dividend per share of 3.6 sen was declared (-3% y-o-y, +6% q-o-q), again representing a 100% payout ratio.

Service revenue in 2Q21 was largely stable sequentially (+0.2% q-o-q, 1.7% y-o-y) on marginal growth at both prepaid (lower subscribers, higher ARPU) and postpaid (higher subscribers, lower ARPU) segments. Digi noted strong take-up for its Prihatin prepaid and postpaid bundles, which led to increased device sales and higher reported revenue. Meanwhile, costs were up sequentially on higher cost of goods sold (increased device sales). Consequently, 2Q21 Ebitda margin contracted by 1.6 percentage points q-o-q to 45.9%.

As the movement restrictions continue, management is mindful of potential near-term challenges in the postpaid segment (channel restrictions, collection challenges). Management is maintaining its FY21 guidance (low-single-digit revenue decline and mid-single-digit Ebitda decline).

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.