KUALA LUMPUR (July 6): Malaysia's central bank is expected to effect additional overnight policy rate (OPR) increases in the remainder of the year, which may result in slower economic growth as higher borrowing costs weigh on corporate earnings and consumer spending, but economists are of the view the impact is likely to be bearable for borrowers.

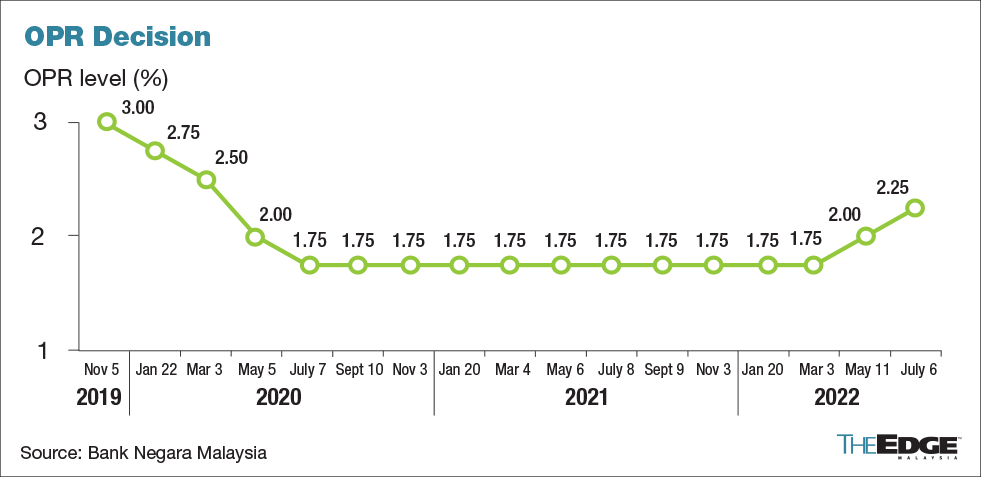

Bank Negara Malaysia's (BNM) Monetary Policy Committee (MPC) raised the OPR by 25 basis points (bps) on Wednesday, pushing the benchmark interest rate to 2.25% from 2.0%. This is BNM's first back-to-back OPR hike since mid-2010.

BNM's two back-to-back rate hikes have only partly reversed the 125 bps cut during the pandemic, UOB senior economist Julia Goh pointed out when contacted.

"Bank Negara cast a positive view of the economy despite rising global headwinds. They sounded confident that the economy can absorb the rate hikes, which is to recalibrate monetary policy in line with the economic recovery," she told theedgemarkets.com on Wednesday.

"In other words, the economy is out of a crisis and keeping rates at ultra-low levels is no longer necessary," she added.

The latest rate hike was in line with Goh's expectations, and she anticipates the central bank to deliver another 25 bps OPR increase in September.

CGS-CIMB's head of economics Ahmad Nazmi Idrus also said a 25 bps hike is not significant enough to hurt consumer finances, as the policy rate is low compared to pre-pandemic levels.

"I think consumers can take it. The purpose of the rate hike is to move away from what Bank Negara has called the 'crisis mode'. Because of this, they will consider the impact on recovery and whether the OPR remains accommodative. If Bank Negara assesses otherwise, [I] don't think they will hike," said Ahmad, who is projecting another 25 bps of rate hike in September as well.

The central bank said the latest hike was consistent with the MPC's view that the unprecedented conditions that necessitated a historically low OPR had continued to recede, and that at current OPR level, the stance of monetary policy remains accommodative and supportive of economic growth.

Bank Islam Malaysia chief economist Mohd Afzanizam Abdul Rashid said while normalisation of monetary policy could post some challenges to highly geared businesses, it is not likely to derail post-pandemic recovery.

"There would be knee-jerk reactions among consumers as well, especially those who are looking to buy a house or vehicle," he said, adding that the central bank's latest move was not a surprise and he, too, is expecting another 25 bps rate hike in September.

"By then, more monetary stimulus would have been ended, and thereby would lead to a slower inflation rate especially when there is no major subsidy removal during this year," he said.

Capital Economics senior Asia economist Gareth Leather also said with the economy recovering, further hikes are likely, but provided inflation remains low, the tightening cycle is unlikely to be aggressive.

Leather pencilled in two more 25 bps rate hikes for the year, and expects one further 25 bps hike in early 2023, taking the OPR back to the same level (3%) as it was on the eve of the pandemic.

"Inflation in Malaysia is much lower than in the rest of the world, with generous subsidies — set to be worth US$11.5 billion (3% of gross domestic product) this year — helping keep the headline rate low. However, the central bank cannot afford to be complacent amid signs that underlying price pressures are rising," he said.

The fact that BNM was not more aggressive with a 50 bps hike on Wednesday also showed the central bank's heavy preference for a "gingerly approach" in tightening, said OCBC Bank's economist Wellian Wiranto.

"In gist, even as Bank Negara is keen to continue normalising its policy rate away from the pandemic-era lows, partly because of the domestic inflation pressure, it does not see the need to adopt a more 'ballistic' 50 bps move at this point, especially given the increasingly uncertain global growth outlook," he said.

"To us, the move strikes the right balance between contending with the two biggest bugbears of the global economy at this point: inflation and recession risks. Going forward, we see at least one more 25 bps hike this year, that will be seen as a further normalisation of policy rate rather than outright tightening," he added.

Read also:

BNM raises OPR by 25 bps to 2.25%