KUALA LUMPUR (Jan 5): After a tumultuous 2020 following an unprecedented pandemic outbreak, the year 2021 saw continued volatility amid various headwinds, chief of which was still the seemingly endless pandemic threat, which saw the emergence of new variants that sent cases surging and brought back strict lockdown measures.

In Malaysia, there were also political uncertainties to contend with, as well as the bout of "once in 100 years" massive floods that came towards the year's tail end.

These battered the FBM KLCI benchmark index, which contracted 3.67% year-on-year, to close at its decade low of 1,567.53 points on Dec 31.

Investors and analysts are now hoping for a better 2022, fuelled by optimism about the resumption of economic activities and growth in corporate earnings. So, what are the best stocks to have?

Below are 10 stocks that have been chosen by three local research houses — Kenanga Investment Bank Research, CGS-CIMB Research and TA Securities — as their top picks for the year:

QL Resources Bhd

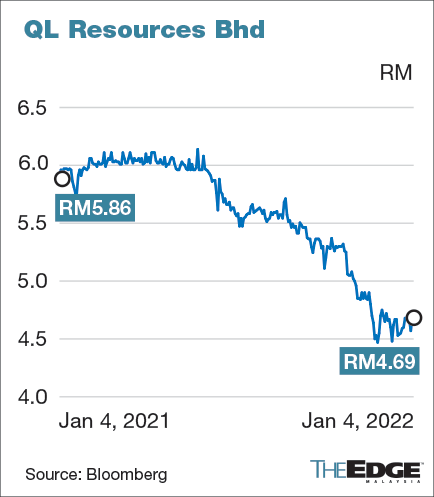

One of the top picks of both CGS-CIMB and TA Securities is QL Resources Bhd, which is involved in marine products manufacturing (MPM), consumer food and integrated livestock farming. QL's share price fell from a high of RM6.14 in May 2021, to a low of RM4.47 in November, before ending the year at RM4.57.

Given the over 20% share price decline in the past 12 months, CGS-CIMB said in a mid-December 2021 strategy note that QL had turned into an attractive proxy for the expected recovery in consumer spending in the first half of 2022.

"We believe the worst is over in 1HFY3/22, with QL expected to record stronger results ahead. This is mainly driven by: i) higher poultry prices to pass on the recent rise in raw material costs (which led to margin compression in 1HFY3/22); ii) higher contribution from its MPM operations (lifting of lockdown restrictions leading to stronger consumer demand and higher production output); and iii) better economies of scale.

"QL should also see higher contribution from its Family Mart business, as QL expects to grow its total store count by 24.4% to 300 by end-FY22F. We also expect consumer footfall to improve in tandem with the lifting of lockdown measures," CGS-CIMB added.

Based on Bloomberg data, QL, with a price-earnings ratio (PER) of 40.96 times, is currently trading at a discount to its five-year average PER of 44.12 times.

Likewise, TA Securities believes QL will benefit from economic recovery as poultry and fisheries, which it is involved in, are among the most sought-after protein sources in Malaysia and the region. Its aggressive store openings planned for Family Mart were also highlighted as another earnings growth catalyst.

CGS-CIMB has a target price (TP) of RM5.50 for QL, while TA Securities has pegged its TP for QL at RM5.90.

On 2022's first trading day, the stock closed five sen higher at RM4.68. It climbed another one sen to settle at RM4.69 on Tuesday, with a market capitalisation of RM11.41 billion.

Hong Leong Bank Bhd

CGS-CIMB and TA Securities also like Hong Leong Bank Bhd (HLB), which CGS-CIMB has highlighted as one of the most defensive banks against credit risks from Covid-19.

CGS-CIMB also likes Public Bank Bhd and RHB Bank Bhd in the banking space, which it has an "overweight" call on expectation of the anticipated economic recovery and a potential rate hike, which will be positive for banks. While it noted banks' CY22F core net profit will be dragged by the one-off Cukai Makmur or Prosperity Tax, excluding this, it expects banks' CY22F core net profit to increase by a rate of 9.4%.

But HLB is its "top pick among Malaysian banks, for its defensive qualities against the credit risks from Covid-19 and good growth prospects from the expected decline in loan loss provisioning, and strong growth in associate contributions from Bank of Chengdu in FY22-23F (which are potential rerating catalysts)".

TA Securities, on the other hand, has highlighted HLB's stellar asset quality against other banks', with its gross impaired loans ratio having improved to 0.48% in 1QFY22 despite a challenging macro environment. Around 22% (versus industry's average of 31%) of HLB's loan base is under the Payment Relief Assistance Plans, it noted, indicating the bank's borrower's profile strength.

Besides its established regional presence, particularly in fast-rising ASEAN countries such as Singapore, Vietnam, and Cambodia, TA Securities also likes HLB for its high environmental, social and governance rating, with a score of 71%, which it noted is one of the highest among its banking peers, with above industry average sustainability efforts.

CGS-CIMB has a RM20.56 TP for HLB, while TA Securities's TP is RM21.70.

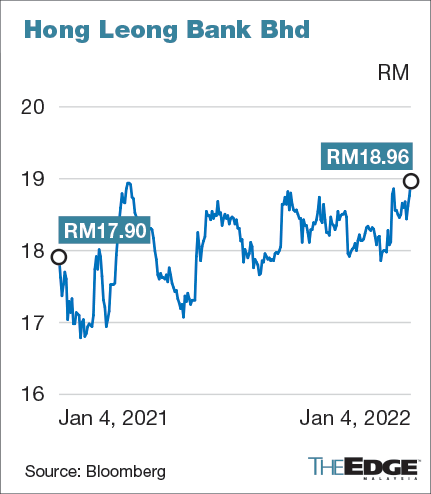

HLB settled 20 sen higher at RM18.96 on Jan 4, valuing the bank at RM41.1 billion. Since January last year, the stock has climbed 7%.

The stock is currently trading at a trailing 12-month PER of 13 times, below the sectoral Bursa Malaysia Finance Index's PER of 14.61 times.

Genting Bhd

Genting Bhd is Kenanga's top pick for recovery play as the research house believes the group's business will recover quickly once cross-border restrictions are relaxed and lifted.

Genting, whose earnings are globally diversified with significant earnings derived from the US and the UK, would also benefit from a stronger US dollar amid a recovery in patronage, said Kenanga.

It added that the new outdoor theme park — Genting SkyWorlds Theme Park — is expected to drive subsidiary Genting Malaysia Bhd's non-gaming revenue.

Over the past one year, Genting shares have climbed 8.98%.

Six analysts have placed a "buy" call on Genting, Bloomberg data showed. Their TPs for the company range from RM5.20 to RM6.92, for an average of RM6.05.

On the sectoral front, the research house believes the gaming sector is poised to be a major beneficiary of recovery play in 2022, with number forecast operators (NFOs) still offering an attractive dividend yield.

"While ticket sales post Movement Control Order have been slow, the worst is over for NFOs as ticket sales should recover to 80% to 85% of pre-Covid level in the first half of 2022.

"The continuous enforcement clamping down on the illegal players is still the key to ticket sales growth," it added.

Shares in Genting finished five sen or 1.06% higher at RM4.78, giving the group a market value of RM18.53 billion.

Dialog Group Bhd

Dialog Group Bhd was one of the worst performing stocks among FBM KLCI constituents in 2021. Its recent earnings saw some decline, dragged mainly by slower downstream activities given the lockdown and slower activity levels.

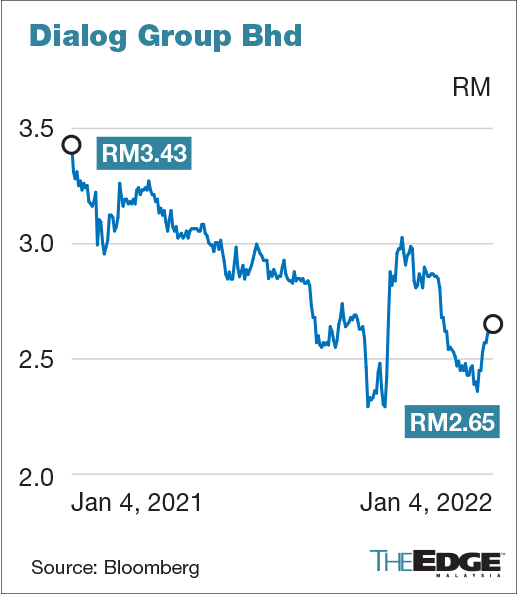

The stock is down by 22.3% since January last year, after declining from a peak of RM3.43 during that month to as low as RM2.29 in September.

Notably, the stock is currently trading below its five-year average PER of 31.73 times, based on Bloomberg data.

On the potential catalyst to the group's share price, Kenanga believes Dialog's stable midstream operations provide a defensive base to cash flows and earnings.

"At current share prices, market is failing to price in any future expansion from Pengerang which we think is likely as Petronas' Pengerang Integrated Complex is set to commence soon, which we believe will help boost prospects for further investments into Pengerang," it said in a research note.

On Jan 4, the stock ended unchanged at RM2.65, valuing the group at RM14.96 billion.

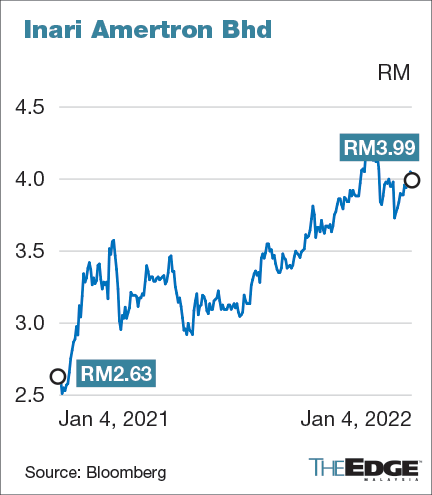

Inari Amertron Bhd

Year 2021 was a remarkable one for Inari Amertron Bhd as its share price rallied by 47% and its net profit doubled in its financial year 2021 (FY21) ended June 30, 2021. Its share price more than doubled from RM1.60 in early January 2020.

CGS-CIMB expects Inari's earnings growth momentum to continue this year on the back of rising 5G penetration and its diversification into auto and industrial sectors.

"We continue to like Inari Amertron Bhd as the largest market cap and most liquid exposure proxy radio-frequency content value. Its recent inclusion in the KLCI index is likely to help catalyst its share price.

"Inari's new system-on-module (SOM) assembly division at P55 is on track to begin production in the first quarter of 2022. We view SOM division as a new growth driver for Inari to diversify and grow its exposure in the automotive and data centre segments.

"In addition, Inari is partnering with China Fortune-Tech Capital Co Ltd to set up a joint venture (JV) for outsourced semiconductor assembly and test manufacturing services in China," it said in a research note.

CGS-CIMB has placed a TP of RM4.95, valuing the company at a forecast PER of 38 times. It believes Inari commands a scarcity premium due to its size and unique position as a FBM KLCI component stock and FTSE4Good Index.

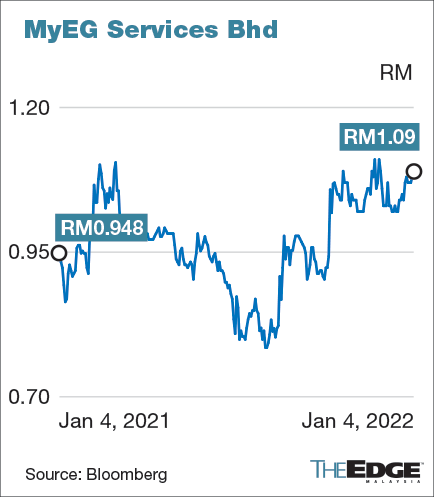

MY EG Services Bhd

CGS-CIMB expects the possible rerating catalysts for MY EG Services Bhd are potential new income stream from Zetrix blockchain JV, higher take-up for its new health-tech services, and expansion of its e-government digital service offerings.

It also said that the group is poised for stronger quarter-on-quarter earnings growth in its fourth quarter of FY21 (4QFY21) ended Dec 31, 2021, driven by higher demand from the health-tech segment, such as private quarantine services for travellers entering Malaysia and the roll-out of Covid-19 breath test systems at major airports nationwide.

CGS-CIMB has placed a TP of RM1.30 and cited that delays in its new e-government services and lower take-up rate for its health-tech services are the downside risks to its "add" recommendation.

The TP of RM1.30 is based on 26 times of the forecast earnings for FY23, which is above its five-year historical PER of 23 times.

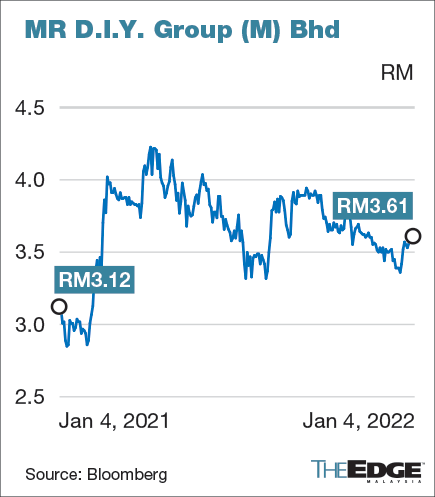

Mr DIY Group (M) Bhd

This is a stock for recovery-theme play on Bursa Malaysia.

With a 15.82% gain for the past one year, Mr DIY is on CGS-CIMB's top pick list as it believes the home improvement retailer is primed for a strong recovery in footfall and average sales per store.

There are 10 analysts having a "buy" call while one has placed a "hold" call, with TPs ranging from the lowest of RM3.39 to the highest of RM4.85.

CGS-CIMB pegs its TP at RM4.40, valuing the retailer at 40 times of the forecast earnings for FY23. The stock closed at RM3.61 on Jan 4.

"We expect its quarterly revenue growth trajectory to continue from its 3QFY21 ended Sept 30, 2021, as most of its outlets are gradually allowed to open, while both consumer footfall and consumer sentiment improve," said CGS-CIMB.

In 3QFY21, the group posted a lower net profit of RM90.35 million or 1.44 sen per share versus RM113.45 million or 1.86 sen per share a year ago due to higher operating expenses from higher store count, while outlets remained closed when Covid-19 movement restriction measures were enforced.

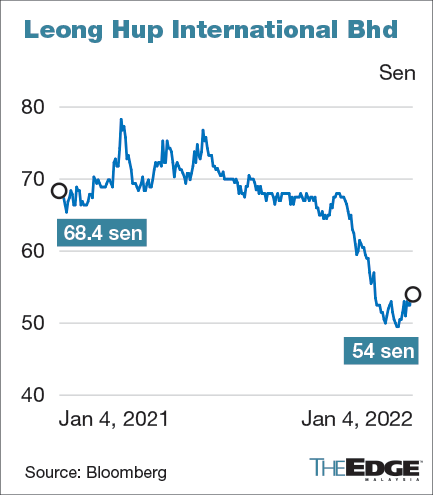

Leong Hup International Bhd

Expectations of better sales at bakery business and higher poultry average selling price (ASP), according to TA Securities, will drive Leong Hup International Bhd's earnings in 2022.

TA Securities noted that Leong Hup is expected to increase the number of The Bakers Cottage stores, which contribute to about 10% of its revenue from home operations.

However, TA Securities cautioned that the key risk factors are volatility in ASP of poultry products, and inability to pass through higher feed and input costs if domestic lockdown is implemented.

Leong Hup's share price rebounded from the low of 49.5 sen on Dec 20, 2021 — the lowest level since the equity rout in the first quarter of 2020. The stock was on a decline starting in June last year, falling from 77 sen.

The poultry firm is another consensus "buy", all the seven analysts tracking the stock are advising clients to invest in Leong Hup. TA Securities pegs its TP at 91 sen, which is substantially higher compared with an average TP of 78 sen. It closed at 54 sen on Jan 4.

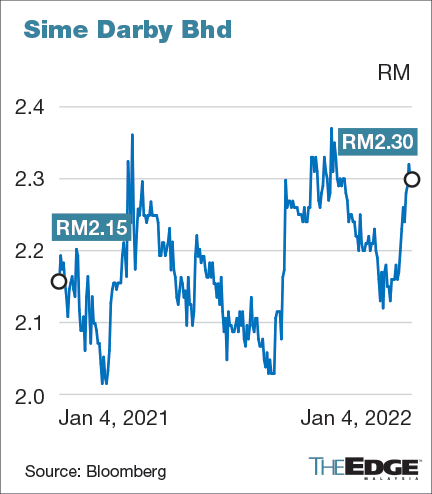

Sime Darby Bhd

Apart from unlocking asset value through divestments, the diversified group is riding on the growing affluence of the middle class in China.

"Sime Darby is reaping the benefits from China's strong rebound in car sales. The car sales in China surged by 29% in FY21 mainly from its BMW China operations.

"We expect the group's motor division to continue delivering compelling results, thanks to rising affluence of the middle class [in China] that spurs the growth in demand for luxury items," said TA Securities.

TA highlighted that Sime Darby is in the midst of divesting non-core assets to focus on its core trading businesses of industrial and motors, and the healthcare business.

"We understand that management is still keen to exit the port business and is working towards divesting its seaport in Weifang, China. This asset had a carrying value of RM963 million as stated in Annual Report 2020."

Besides, it intends to monetise 8,800 acres of plantation land in Labu, Negeri Sembilan, which has been earmarked for the Malaysia Vision Valley project. But the timing of it is not clear.

TA Securities' TP of RM3.02 is based on sum of parts valuation. The highest TP is at RM5.80 among analysts tracking the group.

Telekom Malaysia Bhd

Riding on the 5G roll-out, TA Securities expects Telekom Malaysia Bhd (TM) would get the chance to lease its nationwide fibre network.

TA Securities believes that TM is also poised to benefit from the government's efforts to expand the digital economy. Cloud service is an example. The telco is among the four cloud service providers along with Microsoft, Google, and Amazon that are given conditional approvals to build and manage hyper-scale data centres and cloud services in Malaysia.

"Under the Malaysia Digital Economy Blueprint (MyDIGITAL), the government has outlined plans to shift towards a Cloud-First Strategy which targets to migrate 80% of public data to a hybrid cloud system by end-2022," it said.

On top of that, TA Securities noted that TM's fixed broadband segment is a clear beneficiary of the demand for fixed connectivity driven by the "acceleration in digitalisation" as a result of the pandemic.

TM saw six straight quarters of fixed broadband net adds from 2QFY20 to 3QFY21. "There remains further room for growth in the fixed broadband space, with its nationwide penetration at 39.9% in [3QFY21]," it said.

TM is also another consensus "buy", with 20 analysts recommending it alongside an average TP of RM6.91, compared with its closing price of RM5.47 on Jan 4. The counter soared to a record high of RM6.54 in February 2021.

TA Securities pegs its TP at RM7, based on a discounted cash flow valuation with a weighted average cost of capital of 8.5% and long-term growth rate of 1.0%.

To receive CEO Morning Brief please click here.