This article first appeared in Enterprise, The Edge Malaysia Weekly on August 10, 2020 - August 16, 2020

The once controversial Goods and Services Tax (GST) could be making a return. Multiple sources have informed Enterprise that the tax regime could be announced during the tabling of Budget 2021, slated for November.

“In fact, the reason the announcement was moved from its traditional October slot was to pave the way for the possibility of snap polls, either in September or October,” says one person.

That said, the plan now hinges on two factors: the outcome of the upcoming Sabah state election and the risk of a broad second wave of Covid-19 infections.

“Snap polls may not necessarily be a bad idea for the prime minister because he is seen as having handled the Covid-19 situation pretty well thus far. Businesses are also resuming and there is a sense for now that we are returning to some form of normalcy,” he adds.

“Taking these factors into account, he [Tan Sri Muhyiddin Yassin] may just benefit from snap polls. That said, Sabah’s election results will be a key gauge of when the snap polls at the national level will take place.”

Assuming that the Perikatan Nasional coalition wins the election and returns to power with a fresh mandate, it could reintroduce GST during the budget announcement in November, with implementation to take place between mid-2021 and early 2022.

Multiple sources have independently informed Enterprise that concerted moves on the part of the Royal Malaysian Customs Department (RMCD) are underway, with the backing of the federal government. Having learnt from the experiences of the short-lived “GST 1.0” — which came into force on April 1, 2015 — the authorities are working with the private sector to develop a smoother and less cumbersome “GST 2.0” regulatory framework.

“RMCD is looking at previous GST regulations to improve on them and make them more efficient. Simultaneously, the Ministry of Finance has commissioned numerous white papers from the private sector, with a view to improving on past flaws and to figure out a path to better public acceptance,” says another person.

Thus far, the RMCD has declined to comment.

Impressions among businesses

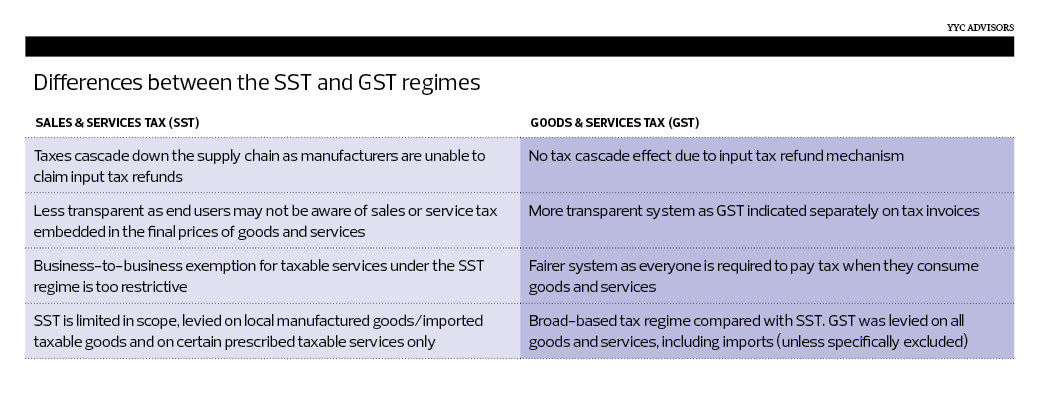

Barely two years on from the introduction of the Sales and Services Tax (SST) regime, the business community is quietly pining for a return to GST. However, this comes with a caveat — that the controversial GST tax refund mechanism, among others, is overhauled and made significantly more transparent and reliable.

Tax experts and business leaders who spoke to Enterprise are unanimous about one issue: In principle, GST is a fundamentally superior and more efficient tax regime than SST. The problems that the business community faced as a result of GST stemmed from poor execution and overzealous enforcement, rather than the tax regime being a basically bad system.

According to Koong Lin Loong, head of the Associated Chinese Chambers of Commerce and Industry of Malaysia’s (ACCCIM) taxation committee and chairman of its SME committee, most businesses — having operated in both SST and GST regimes — prefer the latter. “This is primarily because of the ability to claim GST paid on products that they purchase and subsequently sell in the course of their business,” he says.

According to Malaysian Employers Federation (MEF) executive director Datuk Shamsuddin Bardan, businesses generally consider GST to be a fairer system because of the built-in tax refund mechanism, which does not exist in the present SST regime. This results in an opaque and difficult-to-trace compounding effect on the final prices of goods and services.

Because the tax refund mechanism required businesses to submit regular GST tax returns to RMCD, the authorities could readily verify any refund claims. This resulted in a so-called “closed loop” that consisted of self-reporting of GST collection and tax refund claims by businesses, which could then be verified by the authorities with little to no tax leakages.

For example, if a business’ GST tax refund claim could not be reconciled with its GST tax collection for the month, the authorities could order an audit of the company. Because the SST regime lacked the tax refund mechanism, it also lacked this additional accountability and could not account for possible tax leakages that may have occurred over the last few years.

The tax refund mechanism allowed businesses in the supply chain to claim from RMCD any GST they paid on products that they subsequently added value to and passed along to the next business in the supply chain. Businesses could also claim GST paid on products that they then sold to the final consumer in the chain. GST is considered to be a tax on the final usage and consumption of goods and services, meaning that in all instances, it is meant to be borne by the end-user.

Where the regime went awry was in the execution, says Shamsuddin. “While we view GST to be a more effective tax regime than SST, when it was introduced during the Najib administration, the 6% rate was already considered too high. Furthermore, it was accompanied by the government’s promise that personal income tax rates would be reduced proportionately. However, this promise never materialised.

“As a result, the average taxpayer ended up with a higher overall tax bill when GST was factored in. This was unfair to them.”

For Shamsuddin, any reintroduction of GST must fall well below the previous 6% rate. In addition, he would want to see a proportionate decrease in personal income tax rates so as not to burden the taxpayer. “GST refunds must also be returned to businesses within the prescribed 14-day period, and not perpetually delayed, as was the experience with the earlier iteration of the tax regime ,” he says.

In fairness to the current administration, it has made moves to return at least a portion of GST arrears to businesses. The Ministry of Finance announced in early July that RMCD paid out RM1.264 billion in GST refunds to 4,316 companies. The refunds occurred between June 22 and July 2.

SME Association of Malaysia president Datuk Michael Kang Hua Keong says the broader business community tended to prefer the GST regime, but with significant improvements. “We understood the need for the previous administration to diversify sources of revenue when it introduced GST in April 2015. However, there was a lot of confusion with the interpretation of various GST-related rules and regulations.

“For example, there was a lot of uncertainty among the business community about whether their stock keeping units (SKUs) were considered zero-rated or exempt from GST altogether. Both categories had major taxation responsibilities and implications that businesses struggled to understand.”

Substantial improvements needed

There is a laundry list of improvements that need to take place before a new GST regime can be reasonably expected to be supported by the business community. To start with, the government would be well advised to introduce a three-month tax holiday ahead of any reintroduction of GST.

According to ACCCIM’s Koong, when the country transitioned to GST in 2015, the government implemented a refund period until September that year, whereby businesses would be entitled to sales tax refunds on inventory that they had purchased during the previous SST regime but had yet to be sold by the time GST kicked in in April that year.

“Businesses had until September 2015 to submit sales tax claims to RMCD. This would enable them to be reimbursed for any sales tax they had initially paid. Therefore, the prices of these goods should have fallen because the 10% sales tax would have been reimbursed to businesses and the goods subsequently would have had the 6% GST tacked on,” he says.

“Unfortunately, when it came time for businesses to submit their sales tax refund claims, they found themselves subject to automatic audits at arguably unrealistic thresholds. An audit is a very onerous and difficult process for businesses to undergo.

“For example, if your sales tax refund bill was less than RM10,000, an in-house accountant could sign off on the claim. However, if it exceeded RM10,000 — and realistically, this was the case for many businesses — then it had to be signed off by an external auditor.

“This audit-by-default stance adopted during the Najib administration put off a lot of businesses from pursuing their sales tax claims from the authorities. Many ended up either maintaining the prices of their goods post-GST or just absorbing the losses by selling their goods at a 4% loss [the difference between the 10% sales tax and the 6% GST].”

Going forward, Koong hopes the government will simply do away with this sales tax refund and implement a three-month tax holiday instead. “This will save the government a lot of money in administrative costs, in addition to providing consumers with broadly cheaper goods, as well as boosting business activity in what has been a very traumatic year for the economy so far.”

Deregulate GST to curb inflation

GST was initially introduced and sold to the public as a tax mechanism that would reduce the overall prices of goods and services in the economy. In principle, this should have happened relatively quickly once the regime came into force.

However, Malaysia saw broad increases in the prices of goods and services during the tax regime. Koong attributes this to what he calls “emotional inflation”.

“In the months before the implementation of GST, businesses were worried that the tax would somehow push up the cost of doing business. To be fair, this sentiment was played up by the Opposition parties at the time,” he says.

“A lot of traders pre-emptively increased the prices of their goods to diffuse the future cost increases that would eventually come to be associated with the GST regime. Furthermore, the fact that many businesses did not receive their earlier sales tax refunds until a few years later further limited their ability to control or reduce prices without suffering losses.”

Looking back, Koong believes business owners’ worries were unfortunately justified. As it turned out, the GST regime would go on to be characterised by the sheer volume and complexity of its regulations, the lengthy and difficult to understand exemption and zero-rated lists and, in particular, the Price Control and Anti-Profiteering Act 2011 (PCAPA). Unsurprisingly, the regulatory burdens, among others, imposed significant compliance costs on the broader business community.

“It would be fair to say that one of the main reasons we experienced inflation in the prices of food and necessities during the GST regime was due to the disproportionately high cost of compliance with both GST and anti-profiteering laws,” he says.

Malaysia’s Consumer Price Index (CPI) during the GST regime reflected as much. Prices in the food and non-alcoholic beverages segment tracked much higher than the broader CPI throughout the regime. “While there are many factors that influence prices in the food and non-alcoholic beverages segment, the inability of businesses to offset their costs with GST tax refunds that they ought to have received caused the increased prices during the tax regime,” Sunway University Business School economics professor Dr Yeah Kim Leng tells Enterprise in a statement.

A major contributor to the cost of compliance for businesses was the lengthy and complicated list of exempt and zero-rated goods. A GST-exempt product referred to a product that was exempt from GST altogether while zero-rated goods were simply those taxed at an effective GST rate of 0%.

Although a seemingly minor difference, there were major tax implications for goods in these categories. If a company was manufacturing a zero-rated product, it would not have to collect GST from the sale of the product. However, it would remain eligible for any GST refund that it may have incurred in the manufacturing of that zero-rated product.

Also, a company producing a tax-exempt product would not have to collect any GST from its sale. Crucially, however, it would not be eligible to claim any GST refunds incurred in the manufacture of that tax-exempt product. These represented added costs to the company.

In this instance, the company’s options were limited. It either had to absorb the cost or pass it on to the customer in the form of higher prices. The latter option, however, came with the risk of falling foul of anti-profiteering legislation, which carried stiff penalties.

According to Koong, these lists ended up becoming so granular that there were distinctions between the different types of noodles, which were either tax-exempt, zero-rated or hit with the full 6% GST. This was also the case with the various grades of eggs available in the market. These are just two examples out of countless others.

It is important to note that by and large, the majority of businesses tended to manufacture or trade a combination of tax-exempt and zero-rated goods, as well as those that attracted the full 6% tax. Add on the fact that businesses with annual turnover of taxable supplies in excess of RM5 million were required to file monthly GST tax returns, all this made for nightmarish tax filing responsibilities.

“GST is not supposed to be this complicated. As long as you submit your tax returns on time and in good order, you should be entitled to your refund within the prescribed time period. But given how long and complex the tax-exempt and zero-rated lists became, it was almost unavoidable that businesses would make mistakes on their GST returns,” says Koong.

These mistakes came with expensive penalties. “If you made just one or two mistakes in your monthly GST tax filings, the penalties you would accrue could significantly impact your profit for the year. What is the point of doing business under these circumstances?” he says.

The complexity was further compounded by the anti-profiteering laws as prescribed by the PCAPA. Ordinarily, businesses tended to pass on costs to the end-user in the form of higher prices. This became difficult with the PCAPA in force.

Under the GST regime, businesses had to contend with higher staffing costs, in addition to the requirement to purchase GST-compliant accounting software. In particular, businesses had to contend with deteriorating cash flow positions as they paid RMCD the GST that they had collected from sales while still waiting for their due and proper tax refunds.

In short, it was exceedingly difficult for businesses to operate on pre-GST profit margins. The PCAPA imposed strict limits on the profit margins that businesses were allowed to make on their products. Furthermore, these profit margin calculations proved to be devilishly complex, even by the standards of professional services experts.

“The anti-profiteering calculations were so complex that it would have been very difficult for businesses to accurately calculate without external assistance,” says YYC Advisors CEO Datin Yap Shin Siang.

YYC Advisors is one of the country’s largest home-grown professional services firms. It specialises in advising privately owned small and medium enterprises (SMEs).

According to Yap, the country would be better off without the PCAPA in the long run. “Businesses should be allowed to operate on a ‘willing buyer, willing seller’ basis. If people do not like the prices that are being charged in one store, they are free to go to another. As long as the authorities monitor the markets to prevent price fixing and other anti-competitive or cartel-like behaviour, businesses should be free to charge whatever prices they want.”

But how did these zero-rated and tax-exempt lists become so long and cumbersome in the first place? This was something of a self-inflicted wound, ACCCIM’s Koong concedes. “In the early days of the GST discussion, business associations lobbied hard for their respective industries or products to receive some combination of zero-rated and exempt status. Unfortunately, unlike with the overzealous enforcement of GST regulations and stiff penalties, the government should have been stricter in this instance.”

Herein also lies the solution, says Koong. “Looking ahead to the possible implementation of a new GST regime, I hope the government will reverse its overall approach: adopt a less punitive and more conciliatory approach to businesses’ GST tax filings while being more strict with keeping the list of tax-exempt and zero-rated goods to an absolute minimum.

“The shorter these lists are, the lower the compliance costs will be for everyone. The list of tax-exempt and zero-rated goods should only apply to foodstuff and non-alcoholic beverages as this is the segment of goods that lower-income families tend to spend the most on.”

Responsible, honest accounting of GST refunds

Arguably, the most egregious problem in the entire GST tax regime was the fact that countless businesses never received the tax refunds that they were rightfully owed. This is the single most important improvement that needs to be made. Businesses need to be promptly reimbursed and they should not be subject to audits by default.

According to Koong, the authorities under the Najib administration promised businesses that as long as they submitted their GST tax returns accurately and on time, they would receive their tax refunds within 14 days (if submissions were done online) or 28 days (if done manually).

It has been years and countless businesses have suffered serious cash flow problems because their tax refund claims have been effectively stuck with the authorities since their claims were first filed, says Koong. “Businesses had been informed by the government that they would receive these refunds promptly, so they were never prepared for a scenario in which they would have to write off these refunds as losses.”

YYC’s Yap says roughly 20% of her clients have received only partial payment of their GST tax refunds to date, with the rest receiving their full arrears only in the last one or two years. This caused serious cash flow problems for some of her clients, a number of whom are still feeling the ill-effects.

“About 5% of my clients ended up having to take on some form of additional financing in order to maintain their cash flow. As a result, even today, these clients are more highly leveraged and continue to incur interest and repayment costs as a result of not receiving their full GST tax refunds on time,” she says.

“Going forward, I hope the administration will trust businesses more. We know businesses are willing to abide by GST regulations. We saw evidence of this with very high levels of compliance on GST registrations and tax return responsibilities. I hope the government does not adopt a punitive approach by default. Businesses should be entitled to receive their refunds first, and if at all necessary, to be audited after the fact.

“Additionally, I hope any new GST regime will do away with monthly reporting responsibilities. It is simply too onerous and costly for businesses to undertake on a monthly basis. We should adopt a quarterly GST reporting system, as is presently the case with most countries that have a consumption tax regime.”

According to a report by theedgemarkets.com, as at Aug 3, the government still owed RM4.763 billion in deferred GST refunds. Deputy Minister of Finance II Mohd Shahar Abdullah said all outstanding refunds are expected to be resolved by the end of this year.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.