Tan Chong Motor Holdings Bhd

(May 14, RM3)

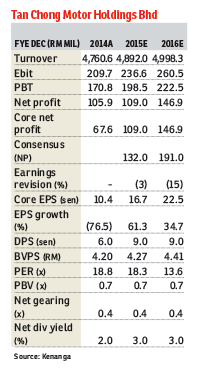

Maintain underperform with a higher target price of RM2.87 from RM2.80: For the first quarter of financial year 2015 (1QFY15), Tan Chong Motor Holdings reported core net profit of RM23.9 million (more than 100% quarter-on-quarter [q-o-q], 41% year-on-year [y-o-y]) which made up 21% of our but only 18% of the consensus full-year estimates.

Note that 1Q core profit after tax and minority interests (Patami) has been adjusted by excluding provision and write-off of receivables and inventories totalling RM2.6 million, gain on disposal of property, plant and equipment (PPE) amounting to RM1.7 million, and some other non-material one-off items amounting to RM3.3 million. As expected, no dividend was declared for the quarter.

The key result highlights reveal that y-o-y, 1Q revenue increased by 25% mainly driven by higher vehicle sales in its passenger segment (+14%).

In terms of market share for non-national passenger vehicle segment, Nissan regained its No 2 position from Toyota compared with a year ago. The new sales of its flagship B-segment model Nissan Almera facelift and new Nissan X-Trail mainly underpinned this.

While revenue recorded stellar growth, earnings before interest and tax declined by 24% with margins being corroded by 2.3 percentage points (ppts) to 3.4%. This indicates higher completely knocked down (CKD) kits cost arising from unfavourable foreign exchange, and aggressive offers and incentives given to clear old stocks prior to the implementation of the goods and services tax (GST). With a better product mix coupled with the group’s sales realignment strategy, earnings before interest, taxes, depreciation and amortisation (Ebitda) margin improved by 1.5 ppts to 5.5%.

Although Nissan CKD models saw some price reductions following the implementation of GST, we do not see it as a strong rerating catalyst for the group as the small price reductions of 0.3% to 2% are insignificant compared to the total cost of ownership.

We view that its operating environment in 2015 will continue to stay challenging on lacklustre consumer sentiment on the back of rising cost of living, tighter financing requirements, which dampen vehicle purchases, intense domestic competition as well as higher operating costs from marketing campaigns, and higher import cost on unfavourable currency fluctuations.

Post-results, we fine-tune our FY15 Patami forecast by -3% to RM109 million for housekeeping purposes.

We also cut our FY16E (estimate) Patami by 15% after accounting for lower vehicle sales and higher imported CKD costs as we had been overly optimistic on the group’s FY16 outlook. — Kenanga Investment Bank Bhd, May 14

This article first appeared in The Edge Financial Daily, on May 15, 2015.