This article first appeared in The Edge Malaysia Weekly on January 11, 2021 - January 17, 2021

THE Employees Provident Fund (EPF) should have no problem paying a 4% dividend for 2020, going by the income it made in the first nine months of last year, The Edge’s estimates show. That’s easily double the prevailing fixed deposit rates offered by banks.

It is likely that the EPF is working hard to pay more than a 4.5% dividend for 2020 to avoid dipping below the 4.5% it paid in 2008 — its lowest on record in the past 12 years.

Going by the RM37.83 billion net investment income that the EPF made in the first nine months of 2020 (9M2020), the provident fund should already have enough to pay a dividend of at least 4.1% for its conventional savings for the full year even if it did not make any money in the fourth quarter, our back-of-the-envelope calculation shows.

Thanks to a stellar investment performance in the second and third quarters of 2020, the EPF should be able to pay between 4.9% and 5.5% dividend for 2020 if it is able to at least match the RM7.5 billion net investment income it made in the first quarter in the last three months of 2020. That’s based on The Edge’s estimate that the EPF would need about RM9.2 billion to pay 1% of dividend for 2020, going by the fund’s growth trajectory the past decade.

In 2019, the EPF — which declared a total of RM45.8 billion in dividends when paying 5.45% to conventional savings and 5% to shariah savings — only needed about RM8.5 billion to pay every 1% dividend.

The amount needed to pay 1% of dividend to its members had doubled in the past decade, mirroring the growth in its fund size to nearly RM1 trillion currently from just below RM500 million at the end of 2012 when the EPF only needed RM4.46 billion to pay 1% of dividend. In 2012, the EPF paid 6.15% dividend, or a total of RM27.5 billion to its members. Its highest ever absolute payout was RM48.1 billion in 2017, when it declared a 6.9% dividend for conventional savings and 6.4% for shariah savings.

While the EPF only needs to deliver a nominal dividend of 2.5% per annum and beat inflation by at least 2% on a rolling three-year basis, expectations regarding EPF dividends have grown the past decade owing to its stellar performance.

Last year, the EPF’s dividend made headlines as being the lowest in a decade as the 5.45% declared for conventional savings was below the decade low of 5.65% paid in 2009. The 5% dividend paid for shariah savings for 2019 was also the lowest in the three years it had been in existence to cater to members who want only shariah-compliant sources for their retirement income.

In the past 15 years, the EPF had traditionally announced its annual dividend between the last week of January and mid-March, usually in February.

What about 2021 dividends?

While the EPF’s gross investment income in the second and third quarters of 2020 were among its best showing in at least 16 quarters, it is not immediately certain how its fund size and asset allocation are impacted by the government’s move to allow more EPF members to withdraw savings meant for retirement.

Owing to the Covid-19 pandemic, additional withdrawals allowed since April 2020 via the i-Lestari Account 2 scheme had seen RM14.41 billion withdrawn by 4.88 million members between April 12 and Dec 18, 2020. That is about 1.5% of the EPF’s investment asset, which stood at RM941.77 billion as at end-September 2020.

Then there was the unprecedented move of allowing withdrawals from Account 1 that was previously off-limits until members hit the age of 55. This age threshold for withdrawals had not been changed even after the retirement age was raised to 60 owing to pushback from the public.

As at Jan 4, the EPF had approved the withdrawal of RM19.62 billion by 2.5 million members from their Account 1 via i-Sinar.

In a statement dated Jan 6, the EPF said the first month’s payout totalling RM10.07 billion for the applications approved so far would be made in stages from Jan 5. According to the EPF, “a majority” of the 1.4 million applications for i-Sinar that had yet to be approved falls under Category 2, which requires members to provide supporting documents. The EPF did not say how much the remaining 1.4 million applicants had asked to withdraw from Account 1.

Collectively, the RM14.41 billion that had been withdrawn from i-Lestari Account 2 as at Dec 18 and the RM19.62 billion approved for withdrawal under i-Sinar Account 1, make up just over RM34 billion, or about 3.6% of the EPF’s investment asset of RM941.77 billion as at end-September.

The EPF’s chief investment officer Rohaya Mohammad Yusof had previously told reporters that the EPF had been preparing its portfolio since March last year in anticipation of higher withdrawals by its members without going into specifics.

It is not immediately certain whether the EPF had raised its holdings in money market instruments, which traditionally bring in less returns than its investment in other asset classes, to have more liquidity to cater to any surge in withdrawals.

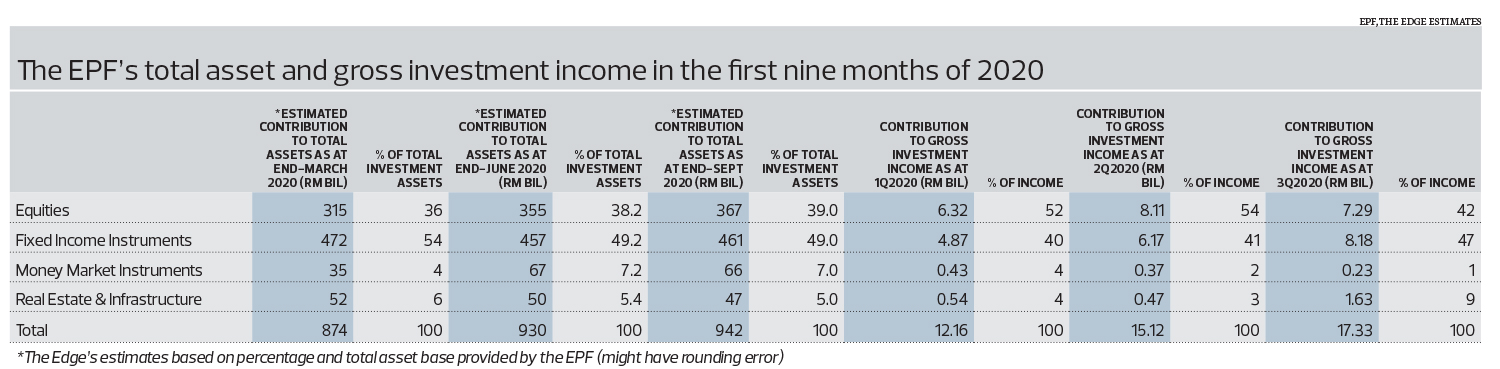

Of the EPF’s RM941.77 billion in investment assets as at end-September, 7% (RM66 billion) were in money market instruments — that’s more than the guidance of 3% allocation in that asset class for capital conservation and liquidity management under its strategic asset allocation (SAA) that seeks to optimise long-term returns within tolerable risk limits.

The EPF’s portfolio as at end-September — 49% (RM461 billion) in fixed-income instruments, 39% (RM367 billion) in equities and 5% (RM47 billion) in real estate and infrastructure — also had less money in real estate and infrastructure relative to its previously guided SAA of 10% for capital conservation and improvement. Its holdings in fixed income instruments were also slightly below the SAA guidance of 51% for capital conservation but it had more money allocated for equities (39%) than the 36% for capital improvement under its SAA.

Some 32% of the EPF’s investment assets are overseas and that contributed 45% of the RM17.33 billion in total gross investment income in the third quarter. That’s up from 30% of its assets that contributed 39% of its RM15.12 billion gross investment income in the second quarter.

Interestingly, the EPF’s stellar investment income performance in the second and third quarters of 2020 was from a much stronger performance from its fixed income investments. Income from its real estate and infrastructure investments was also higher than usual in the third quarter of 2020, a surge that is generally seen in the fourth quarter rather than the third quarter based on its performance in the past three years.

If the EPF can keep up its performance in the fourth quarter, its 2020 dividend would not fall to a new decade low.

Policy action to boost retirement savings

The fund should be in a better position to comment on its growth trajectory once most applications for i-Sinar are processed. Applications for i-Sinar remain open through June 30 this year. The EPF said on Dec 2 that the facility is “open to up to eight million eligible members”. The provident fund has 14.8 million members, about 7.6 million of whom are active (contributing) members.

It is also not immediately known how much the monthly inflow of contributions to the EPF had recovered since the lifting of the nationwide Movement Control Order (MCO) that lasted from March 18 to May 3 last year, during which unemployment spiked to as high as 5.3%, or 826,100 persons, in May.

Bank Negara Malaysia no longer provides the data on its website and the EPF has yet to revert on requests for the latest data on its monthly contribution and withdrawals.

Before the Covid-19 pandemic, the EPF had received roughly RM1.7 billion in net inflow of cash on average every month. Monthly contributions always exceeded withdrawals by RM600 million to RM3 billion a month between January 2015 and December 2019, official data shows. During the five-year period, the EPF received between RM4.6 billion and RM7.2 billion a month in mandatory contributions from its members while withdrawals ranged between RM2.8 billion and RM5.3 billion a month.

Based on the fund’s growth trajectory before Covid-19 hit, The Edge had expected the EPF’s fund size to reach RM1 trillion by end-2021. Based on the assets it had under management in 2019, the EPF was already the world’s 12th largest pension fund.

With many lower-income EPF members exhausting their savings in Account 2 (30% of EPF savings) last year and likely to be applying to withdraw funds from Account 1 (70% of savings), discussions on how policymakers can help more people save enough for retirement will need to pick up speed to come up with the best policy action.

Among other things, the EPF has also yet to comment on suggestions that it implements a tiered dividend income scheme to boost the retirement kitty of those with lower EPF savings.

The youngest of the “baby boomers” — those born between 1946 and 1964 — had already reached the age of 55 in 2019 and will reach the current retirement age of 60 by the end of 2024. Experts at the World Bank are among those who recommend that Malaysia raise its retirement age gradually from 60 to 65 as one of the measures to prepare for an ageing society.

With the average Malaysian projected to live to 75, the EPF’s current basic recommended savings of RM240,000 were derived based on one having RM1,000 a month to spend for 20 years after retiring at age 55. Based on the same assumptions, that basic recommended savings would only be RM180,000 if one were to retire from work at age 60 and RM120,000 if one were to retire from work at age 65.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.