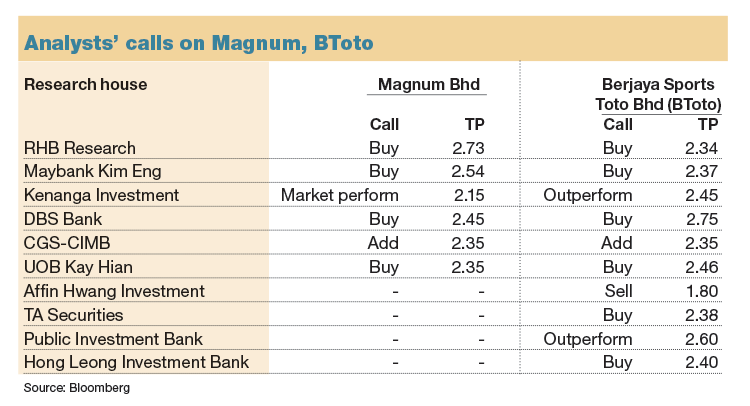

KUALA LUMPUR (May 12): RHB Research remained bullish on number forecast operators (NFOs) Magnum Bhd and Berjaya Sports Toto Bhd (BToto) despite the nationwide Movement Control Order (MCO 3.0) that comes into force today, which could impact ticket sales.

In a note today, RHB Research analyst Loo Tungwye said the lockdown is expected to slow down the path to full ticket sales recovery for Magnum, as punters may exercise caution during this period and avoid going to crowded places.

He added that some may buy from illegal operators due to the ease of transaction, and this may chip away some revenue from the legal NFOs.

“However, ticket sales should recover strongly under a normalised business environment, given the fairly inelastic nature of the business,” he said.

For the first quarter of 2021 (1Q21), the analyst said ticket sales hovered at 20% of pre-pandemic levels during MCO 2.0, when most outlets were temporarily closed from Jan 13 to Feb 15, although ticket sales were able to recover swiftly since outlets reopened on Feb 16 to around 80% to 85% of pre-pandemic levels.

Based on its jackpot prize compilation, the research house estimates that Magnum’s 1QFY21 average jackpot ticket sales fell 18% quarter-on-quarter (q-o-q) and 32% year-on-year (y-o-y) despite a bigger average jackpot size.

Meanwhile, BToto’s average jackpot sales for the third quarter ended March 31, 2021 (3QFY21) is estimated to have fallen 29% q-o-q and 53% y-o-y, partly due to a lower average jackpot size.

Loo said the 3QFY21 prize payout could be higher as the Supreme 6/58 lotto game, with a RM48 million prize money, was won in early January 2021.

Post earnings changes, the research house lowered its target price on Magnum to RM2.73, although it continues to like the stock for its attractive FY22 forecasted yield of 7.6%, with the counter remaining as its preferred pick for being a pure-play NFO. It maintained its "buy" call on the stock.

RHB Research is forecasting Magnum to record net profit of RM207 million for the financial year ending Dec 31, 2021, on the bank of RM2.39 billion in revenue, versus last year’s net profit and revenue of RM21 million and RM1.67 billion respectively.

Meanwhile, it cut its FY21 to FY23 forecasted earnings for BToto by 2.1%, 8.2% and 3.6% after lowering its ticket sales assumptions, with a lower target price of RM2.34.

For FY21, the research house expects BToto to post net profit of RM193 million, on the back of RM4.92 billion in revenue.

It maintained its "buy" call on the counter, backed by the attractive 7.9% dividend yield for FY22 and FY23.

“While MCO 3.0 is expected to disrupt the ticket sales recovery, these are just short-term hurdles, especially with the rollout of vaccines. Once the vaccination curve steepens and Covid-19 cases [lessen], we expect ticket sales to recover strongly under a normalised business environment.

“NFOs are known to be resilient and demand is fairly inelastic, even in a dull macroeconomic environment,” Loo said.

At 11.30am, Magnum fell one sen or 0.47% to RM2.10, giving a market capitalisation of RM3.02 billion.

BToto dipped two sen to RM2.01, translating to a market capitalisation of RM2.74 billion.