This article first appeared in Personal Wealth, The Edge Malaysia Weekly on May 1, 2017 - May 7, 2017

Malaysian individuals and entities that have bank accounts overseas will soon see their financial information being shared with other countries and tax authorities in an effort to boost global transparency and tax compliance. This requirement is part of the automatic exchange of financial account information set out by the Organisation for Economic Cooperation and Development (OECD).

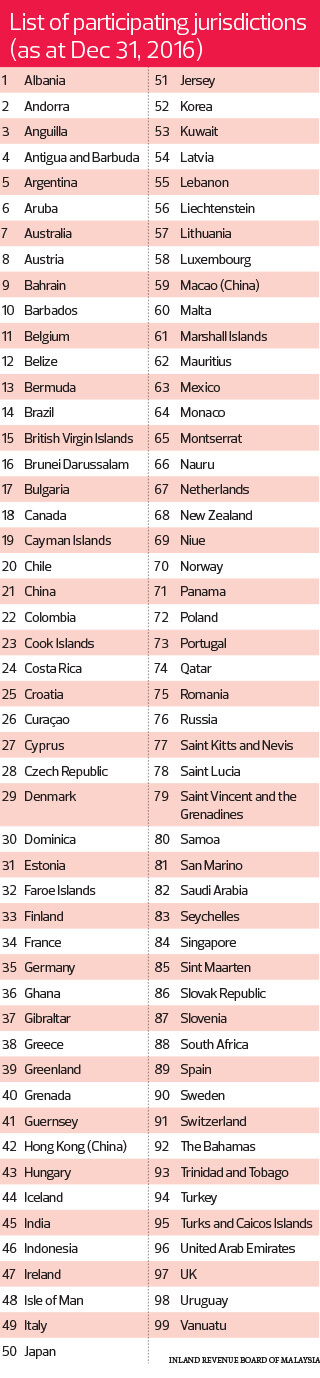

Malaysia is one of 99 countries — including global offshore financial centres such as the British Virgin Islands, Liechtenstein and Luxembourg — that have agreed to implement the Standard for Automatic Exchange of Financial Account Information starting in June. The agreement, which is on a reciprocal basis, allows for the automatic exchange of information related to financial accounts with other jurisdictions on an annual basis.

The standard has two components — the Model Competent Authority Agreement (CAA), which contains the detailed rules on the exchange of information, and the Common Reporting Standard (CRS), which contains the rules for reporting and due diligence. Financial institutions are required to submit the details of pre-existing accounts by June 30 under the CRS.

According to the Inland Revenue Board’s (IRB) website, Malaysia has committed to exchange CRS information from 2018 and will receive the financial account information of Malaysian individuals and entities from other tax authorities. “This will help ensure that residents with financial accounts in other countries are complying with their domestic tax laws and act as a deterrent to tax evasion,” it says. Financial institutions in the country are also required to share the financial account information of non-resident individuals and entities with the IRB.

Financial institutions, including depository institutions such as commercial banks that accept deposits and engage in the ordinary course of banking activities; custodial institutions, such as offshore entities that hold financial assets for others; and fund houses, including those that sell unit trusts, will have to get their customers to sign a self–certification declaration stating their tax residence status to comply with the CRS.

These institutions will then have to conduct the necessary due diligence to see if individuals and entities hold reportable accounts and inform the IRB. Subsequently, the IRB will transmit this information to other participating tax authorities.

“Financial institutions are very good conduits for people to keep money offshore. But moving forward, Malaysian financial institutions will have to do due diligence on the accounts of individuals and entities and check whether they hold reportable accounts,” says Deloitte Malaysia executive director of financial services Chee Pei Pei.

The Ministry of Finance amended Section 132b of the Inland Revenue Board of Malaysia Act last year to allow mutual administrative tax assistance between governments for the exchange of information. While this has yet to be implemented, the agreement has raised concerns about information falling into the wrong hands.

Millie Chan, a senior consultant and lawyer at Borden Ladner Gervais, says high-net-worth individuals who manage their wealth using offshore financial centres — which provide services such as low or zero taxation, moderate or light financial regulation, banking secrecy and anonymity — do so to protect themselves and not all of them are trying to evade payment of taxes.

“Under the standard, the information goes through several channels. So, you want to ensure that it is secure and there are no leakages. If it falls into the wrong hands, it could lead to kidnapping or extortion,” says Chan, who is an expert on holistic global estate planning involving international wealth transfer, asset protection and capital preservation.

“People want to go offshore because of the anonymity, where people do not know anything about you. It has nothing to do with tax evasion. These people pay their taxes fairly. It is just a matter of protecting themselves as a lot of money attracts a lot of evil eyes.

“We must stress that it is not wrong to protect yourself and it does not mean that it is tantamount to hiding from the authorities.”

Chee points out that when Malaysia committed to the CRS framework, the Ministry of Finance also amended the Income Tax Act and put in place stringent data security and encryption measures. “Only when the specifications of data protection are met and there is confirmation that the jurisdiction has appropriate confidentiality and data safeguards in place that the jurisdiction signs the documents.”

Chan and Chee spoke to Personal Wealth on the sidelines of a forum organised by Labuan International Business and Financial Centre titled “The Future of Tax Planning and Wealth Management: Transparency and Substance for all?” last month.

Adopting a wider approach

Prior to the CRS, countries were not obligated to exchange information on the financial assets of non-resident account holders. “With increased access to global financial and cross-border services, you see that wealth held by individuals can be kept outside Malaysia. I can go to the British Virgin Islands or Switzerland to open a bank account,” says Chee.

“Previously, this information was not made known to the tax authorities because I was not required to report it. But then the global tax authorities realised that individuals have kept a huge amount of financial assets outside their respective countries.

“You have heard about cases involving Starbucks, Google and eBay. They pay a minimal amount on tax. I am not saying that it is not legitimate. It is totally legal within the respective countries’ tax laws. But the question is whether they pay the right amount on tax and in the right countries.”

She says the OECD and G20 have found that the US Foreign Account Tax Compliance Act has been effective in collecting information on its citizens who reside abroad. Some countries have already begun collating relevant information as they are among the early adopters of the framework, she adds.

Malaysia has signed the Multilateral Competent Authority Agreement, says Chee. But jurisdictions such as Singapore and Hong Kong have chosen the bilateral information exchange as they get to choose the countries they want to sign with.

“Malaysia has adopted the wider approach. It means that when a financial institution wants to do due diligence, it has to do due diligence on all of its account holders, irrespective of their tax residence status. When financial institutions submit the information to the tax authorities, they only submit the information of the tax residents of participating jurisdictions,” she says.

How does the financial institution determine the resident status? By virtue of the individual’s physical presence in that country for more than 182 days, says Chee.

For clients with financial assets of more than US$1 million, self-certification alone does not suffice. “Their relationship manager will have more questions for them,” says Chee.

What do individuals do when the authorities come knocking on their door? She says it would be wise to keep track of their financial assets and information on the sources of income. “Malaysia operates under a territorial scope of taxation, unlike Indonesia and Australia, which have a worldwide taxation policy.

“For instance, if I disclose my information and it goes to the IRB, will it have the right to claim that the income is taxable? In such circumstances, individuals will need to look at whether the income comes from employment or business activity in Malaysia. If it is not revenue but capital income — for example, income from property I have disposed of — it is not subject to tax other than the Real Property Gains Tax.

“Say an individual placed an offshore fixed deposit of US$1 million back in 2010 and has traded shares and bought properties over the years and the amount has increased to US$15 million. The tax authorities in Australia will have to acknowledge that the person has US$15 million in his account. The individual would also have to keep the right information to determine whether such income is taxable in Malaysia and be able to explain where the money comes from.”

Types of financial information required

According to the Organisation for Economic Cooperation and Development’s Standard for Automatic Exchange of Financial Account Information, the reporting of financial information will be done on a broad scope, covering three dimensions.

The first dimension is the scope of financial information reported, where the comprehensive reporting regime covers different types of investment income, including interest, dividends and similar types of income. It also addresses situations where a taxpayer seeks to hide capital that represents income or assets on which tax has been evaded (for example, by requiring information on account balances).

The second dimension is the scope of account holders subject to reporting. The comprehensive reporting regime requires reporting not only with respect to individuals but also limits the opportunities for taxpayers to circumvent reporting by using interposed legal entities or arrangements. This means financial institutions are required to look through shell companies, trusts or similar arrangements, including taxable entities, to cover situations where a taxpayer may seek to hide the principal but is willing to pay tax on the income.

The final dimension is the scope of financial institutions required to report. The reporting regime covers not only banks but also other financial institutions such as brokers, certain collective investment vehicles and certain insurance companies.

Increased measures bode well for Labuan IBFC

The increased compliance and regulatory requirements arising from the implementation of international agreements such the Common Reporting Standard (CRS) and Base Erosion Shifting (BEPS) will only make Labuan International Business and Financial Centre (IBFC) more attractive, says CEO Danial Mah Abdullah, who brushes aside concerns that complex compliance measures would deter investments as transparency holds greater weightage when it comes to investments.

“The requirements for transparency and the need to conform to initiatives such as CRS and BEPS will be the new normal for all financial centres. For Labuan IBFC, the need to conform to international regulatory requirements has always been our key principle,” he says.

“We believe that as businesses adopt the new normal, the higher transparency requirements, it will be natural for them to consider establishing substance in a well-regulated and cost-efficient jurisdiction to facilitate cross-border transactions and investments, including re-domiciling their businesses. Labuan IBFC’s physical location and accessibility make it ideal for Asia-based companies.”

Tan Hooi Beng, executive director of international tax at Deloitte Malaysia, says the CRS regulations will make it tougher for individuals or businesses to avoid tax. He points out that such laws are bound to change the notion that offshore financial centres are havens for those involved in money laundering or tax evasion.

Labuan IBFC is a mid-shore financial centre that provides corporate and private clients with a wide range of solutions and services, including trust facilities and private foundations for wealth management. According to its website, there were more than 13,000 companies incorporated as at December last year.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.