LPI Capital Bhd

(July 9, RM14.38)

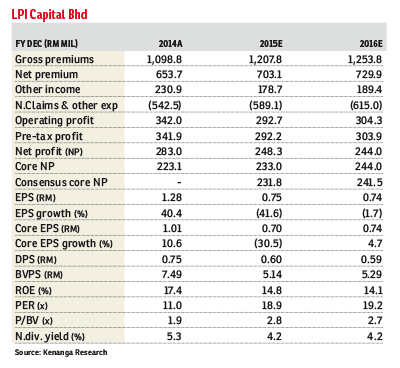

Maintain market perform with a target price of RM14.44: The second quarter of 2015 (2Q15) reported net profit (NP) came in at RM85.7 million, bolstered by a series of Public Bank share sales, bringing first half of 2015 (1H15) NP to RM142.9 million.

Consequently, LPI Capital Bhd’s shareholding in Public Bank was slightly reduced to 1.42% at end-2Q15 (from 1.48% at end-1Q15).

On a core basis, ex-Public Bank share sale gain of RM33.35 million, NP would have registered at RM52.4 million and 1H15 NP at RM109.6 million, meeting expectations at 47% of both our full-year forecast and street estimate.

The first interim single-tier dividend of 20 sen was declared, which will go ex on July 22 and payment will be on Aug 3.

Year-on-year, 1H15 NP surged 40.5% mainly due to hefty capital gains (more than 100%) lifted by a series of Public Bank share sales this quarter.

Excluding the gain, core NP would have grown 7.7%, which is still commendable but more moderate compared to its historical track record of double-digit growth. Core NP growth was supported by advancements in net earned premiums (NEP) (up 3.8% to RM320.9 million) and other income (core) (15.8% to RM102.1million); aided also by a 1.2 percentage points (ppts) reduction in the effective tax rate (core) to 21.3%.

Potential NP expansion was capped by larger claims (ratio: 0.6 ppts) and a higher management expenses ratio (ratio: 2.6 ppts). Consequently, the combined ratio increased to 72.3% (1.1 ppts).

Segment-wise, surplus widened for fire (16.2%), marine, aviation and transit (19.4%) and miscellaneous (1.1%) underwriting.

Surplus in the motor segment, on the other hand, contracted (29.4%) as its claims ratio increased 6.1 ppts to 80.2% negating growth in its NEP (7.6%).

On the upside, reductions were recorded in claims (5.5 ppts) and management expense ratio (0.8 ppts). However, given that net commission expense was seen this quarter (as opposed to a net commission income in the preceding quarter), the combined ratio still inched up to 72.5%.

In terms of strategy, the group is expected to maintain focus on building its agency network while continuing to leverage its bancassurance partnership with Public Bank to expand its insurance business apart from growing its broking and global partnership business.

While LPI is still proving resilient, with core NP growth still registering in the high single-digits for 1H15 amid a challenging economic environment, growth has somewhat moderated from its historical double-digit growth and claims are creeping up. Hence, we remain “neutral”. — Kenanga Research, July 9

This article first appeared in The Edge Financial Daily, on July 10, 2015.