This article first appeared in City & Country, The Edge Malaysia Weekly on August 23, 2021 - August 29, 2021

Prospective homebuyers have the option of purchasing a property on either the primary or secondary market. Since buying a house is one of the largest purchases one makes in life, what do they need to know about the two types of properties?

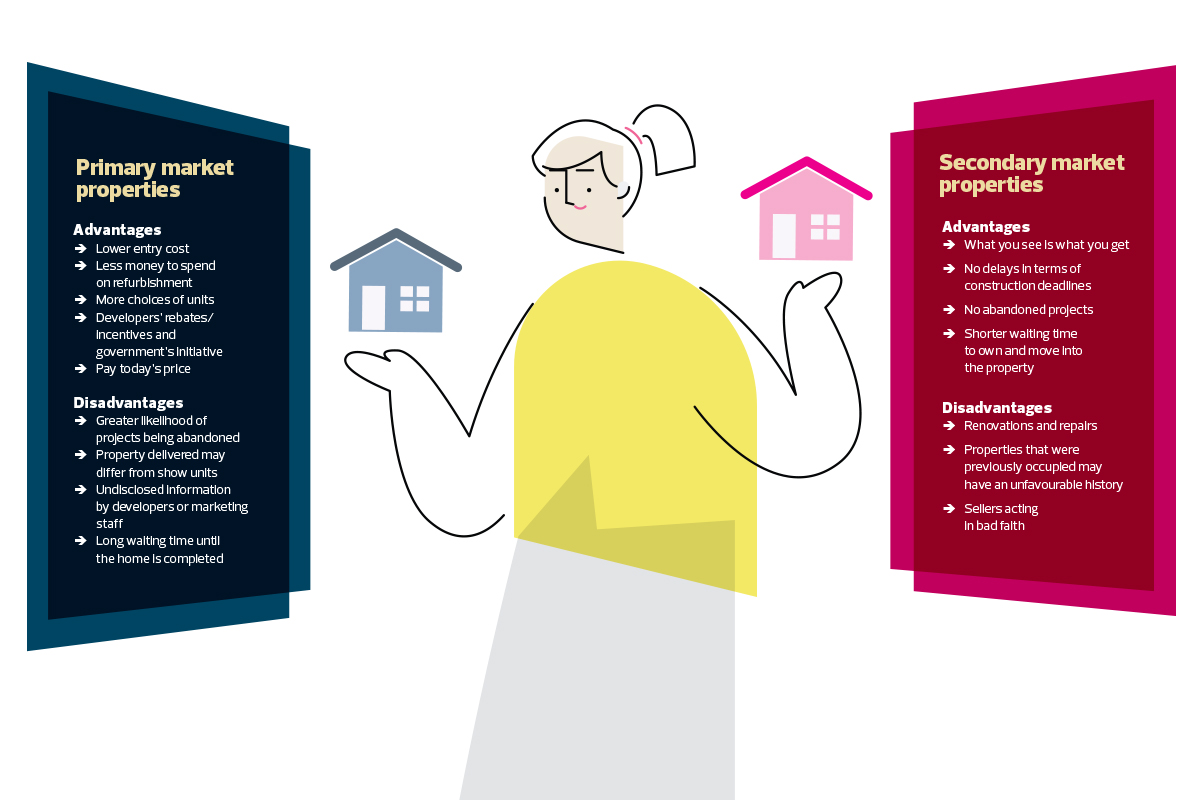

According to Metro Homes Realty Bhd executive director See Kok Loong, the primary market refers to brand-new properties, which are usually offered to buyers at a launch event or as part of an ongoing project by the property developer.

“The sale and purchase agreement (SPA) is governed by the Housing Development Act (HDA) and it comes with a defect liability period clause, also known as a warranty period. This refers to the period of time from the date buyers receive delivery of vacant possession and keys to their property, during which the developer is responsible for fixing any defects,” he says.

Under the HDA, the defect liability period is 24 months and 36 months for individual and strata-titled properties respectively, starting from the date of their vacant possession. During this period, homebuyers are required to check for any damage, defects or faulty workmanship on the property and report these issues to the developer to get them repaired free of charge.

Meanwhile, the secondary market refers to subsale properties, or those that were previously owned, in mature locations and established residential areas.

“These properties are introduced into the market for rent or subsale, and will be either rented or occupied by subsequent owners. The transaction is between the initial buyer and the subsequent buyer, and this can be repeated many times. The SPA, which is governed by the Contracts Act 1950, is the end result of the negotiations of the terms and conditions between the buyer and seller,” says See.

Whether you are buying a property on the primary or secondary market, each has its advantages and disadvantages.

See says one of the advantages of buying properties on the primary market is the much lower cost of entry compared with subsale properties. Many developers offer discounts and absorb certain costs such as legal, loan agreement and stamp duty fees. These properties are usually priced lower or at market value by developers. So, buyers are likely to enjoy a healthy capital appreciation, sometimes even before the property is completed.

“A lot of real estate speculators look for capital appreciation, and it is no surprise that they are among those who prefer primary market properties. Buying properties from the developers at a relatively lower price and later selling them at an appreciated value on the secondary market drives them to make such purchases,” says See.

Since properties on the primary market are brand new, less money is required to be spent on refurbishment, he notes. Buyers can also choose their desired units (if available) and take advantage of developers’ rebates or incentives and the Home Ownership Campaign, which was extended until Dec 31 this year by the government.

However, the downside of buying such properties is that projects are sometimes abandoned when developers run into financial troubles.

“In this case, buyers would have to pay instalments for 10 to 15 years for an uncompleted project, or may even lose their deposits and still not have their property. As such, it is crucial to check the developer’s financial standing, track record and reputation before signing on the dotted line,” says See.

Sometimes, the actual property does not turn out the way it was portrayed in the show units/houses. “This can be quite disappointing and if the specifications do not meet the buyer’s expectations, it can be something that he or she does not want, which ultimately makes it difficult to sell in the future,” he says.

“There may also be information undisclosed by the developer or marketing staff on approved future products or infrastructure that will bring adverse impact to a project, such as having an elevated highway in front of the development, or a cemetery or sewerage treatment pond next to it.”

Unlike properties on the secondary market, where buyers can get the keys as soon as the SPA is completed, those who purchase properties on the primary market are paying today’s price, but the delivery will take three to four years. On the other hand, if the market price increases at 10% a year, the price of the property may have appreciated 30% to 40% by the time the buyer collects the keys. “For instance, if you are placing 10% and leveraging a bank loan, you can earn a gross profit of 300% to 400% if you are able to dispose of it,” says See.

Similarly, buying properties on the secondary market has its pros and cons. “With properties on the secondary market, it is a case of ‘what you see is what you get’ because the property is tangible and generally has lower risk, as the buyers can see exactly what they are getting into. They will know the exact location, surroundings, neighbours and amenities. They can also inspect the unit as well as the maintenance level and facilities,” he says.

At times, buyers can get great value-for-money deals if good agents show them houses that are going for possibly 30% below market value.

Unlike buyers of properties on the primary market, those purchasing properties on the secondary market will not face problems such as delays or abandoned projects, as the property has been built and you can move in anytime once the legal documents are done.

On the other hand, there are usually repairs and renovations to be made to the property. The buyer may need to redo the electrical and plumbing works and make extensive renovations if the unit is old or badly maintained.

See advises those considering properties older than 10 years to set aside a fair amount of money for renovation and refurbishment. They should also be aware that some properties may have an unfavourable history.

There are also times when a buyer purchases the property from an irresponsible seller. “This is when the buyer almost gets the house at the final stage of the deal process, but receives a last-minute message that the seller has decided not to sell the property due to a better offer from another buyer,” he says.

Consequently, the decision to purchase a property on the primary or secondary market would depend on the buyer’s stage of life, needs and financial readiness.

In the current market conditions, See suggests that buying a property on the secondary market would be a better option as many homeowners are unable to service their loans due to financial difficulties as a result of the pandemic and would be willing to sell their properties at a lower price.

Considering that many of those who bought properties in 2018 and 2019 are being pressured to sell them on the secondary market at a lower price than when they purchased the units, one may be able to get a brand-new completed home on the secondary market, he opines.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.