THE new International Financial Reporting Standard (IFRS) 9, which kicks in from Jan 1, 2018, will have a huge impact on banks and will inevitably affect borrowers too, says PricewaterhouseCoopers Malaysia (PwC).

“Generally, I would expect that loans would become more expensive for the borrower, depending on the credit profile, ” PwC’s leading expert on the new accounting standard, Elaine Ng Yee Ling, tells The Edge in an interview. PwC advises banks on IFRS 9 implementation. Ng is a partner at the firm specialising in financial services.

But what is IFRS 9? It is an accounting standard relating to financial assets, issued by the International Accounting Standards Board, that will replace the current IAS 39 standard from January 2018. Countries that have adopted IFRS, including most major markets like the UK, Hong Kong, Singapore and China, will have to meet that global timeline for IFRS 9 implementation. In Malaysia, its equivalent is known as MFRS 9, and it replaces MFRS 139.

In a nutshell, it will change the way banks book provisions on financial assets like loans and bonds. MFRS 9 requires banks to make appropriate provisions in anticipation of future potential losses, rather than the current practice of providing only when losses are incurred. This means that banks will have to recognise provisions from the day they extend any loan, including undrawn commitments.

“So, basically, banks will have to go from using an incurred loss model to using an expected credit loss (ECL) model,” Ng says.

According to her, this would have far-reaching implications on Malaysian banks, and to some extent, insurers. For one, it will lead to banks,in some cases, having to make substantially higher provisioning, which could hurt earnings and weigh on their capital. It could also potentially affect dividend payouts.

Ng says, based on early simulation exercises by some banks in Malaysia on the Day 1 impact of MFRS 9 adoption, provisioning could potentially jump by more than 50% . This is higher than the 25% to 50% range in a PwC survey of several global banks.

Secondly, she says, in trying to deal with the potentially higher provisioning, banks may reprice or restructure the loans, making it more expensive for borrowers with riskier credit profiles. Additionally, banks will likely be revising their business strategy. For example, they might think twice about extending certain types of loan facilities if they are deemed too risky or no longer profitable, she says. These could include reducing the limit of undrawn facilities such overdrafts.

It is understood that the banking regulator, Bank Negara Malaysia, is also concerned about how the lending landscape may change, post MFRS 9, and has been engaging banks on the matter.

Why the higher provisions

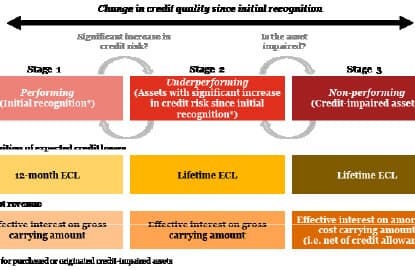

IFRS 9/MFRS 9 outlines a “three-stage” model for provision/impairment based on changes in credit quality since the day the loan was extended.

“Currently, when banks do provisioning, they have impaired and non-impaired accounts. But, under MFRS 9, the non-impaired accounts have to be split into one of two stages — Stage 1, which is what we call a ‘performing’ account, and Stage 2, which is an ‘underperforming’ account. Stage 3 is for impaired loans,” Ng explains.

For accounts that fall under Stage 1, the bank has to provide 12-month forward-looking expected credit losses. 12-month ECL are the expected credit losses that result from default events that are possible within 12 months after the reporting date. Borrowers with good credit risk profile will likely fall under Stage 1.

It is when accounts fall under or get into Stage 2 that it gets more problematic for banks, as this is where the provisioning gets heavier — potentially around four to five times more than that for Stage 1, depending on the product, says Ng.

For Stage 2 accounts, banks have to provide lifetime ECL. Lifetime ECL are the expected credit losses that result from all possible default events over the expected life of the loan. “So, if a mortagage loan has an expected maturity of 20 years and it has gone into Stage 2, you have to provide (over) 20 years ECL, instead of 12 months,”says Ng.

“Also, because now we have to talk about lifetime ECL, a 10-year loan versus a five-year loan will carry different provisioning. With the longer tenure, your provisioning will be higher. So in the past, where banks would give a loan and like to stretch it because it gives them recurring income, now they will have to think it through for borrowers with not very good rating. So for an SME customer, for example, to get a longer tenure loan can be more expensive, going forward,” she notes.

Accounts generally fall under Stage 2 when there is “significant increase in credit risk” since the loan was extended. But there is multiple criteria to determine if an account has to be downgraded to Stage 2.

“The standard has 16 criteria, including if the borrower is 30 days past due, so if you miss your one-month payment, you come to Stage 2. But banks can rebut this, with what we call a 30-day rebuttable presumption, if they feel it doesn’t warrant going to Stage 2 — they basically have to build a model to argue that even though the borrower is one-month past due, but because of behavioural patterns and what not, it may not be 30 days but a little bit more than that [that could be acceptable],” says Ng.

In general, banks are likely to rebut retail loans rather than corporate loans. “If corporates miss a payment, it’s usually not a good sign and an indication that they are underperforming. It would be difficult to rebut corporate and SME accounts,” explains Ng.

To avoid having assets fall to Stage 2 because of a missed payment, the banks’ collection department is going to play an increasingly important role, going forward. “Early payment alert will become a key strategy for banks,” remarks Ng.

It is likely that loans that are currently on banks’ watch list for potentially turning sour, or special mention loans, are likely to come under Stage 2, she says. It is understood that this is likely to include loans from the troubled oil and gas sector.

“If you’ve gone to Stage 2, banks are getting legal advice on whether, based on the existing contract with the borrower, they can ask for additional interest or additional collateral. Basically, banks are exploring what else they can do when accounts go to Stage 2. But the key thing they are looking at now is to ensure that customers don’t go from Stage 1 to Stage 2,” she remarks.

Unlike before, banks now have to make a provision for unutilised lines. “So, for example, overdraft limit and bank guarantees — which are all off the balance sheet — will need to be provided for. So your credit card limit will now carry a provision ...this means banks are going to be very careful about credit card customers and some may consider reducing the limit,” says Ng.

Interestingly, apart from loans, banks will now also have to make provisions for bonds that they invest in. “Bonds also have to be put in Stage 1, 2 or 3. That means that the treasury department also gets affected,” she says.

Ng says most Malaysian banks are still in the midst of assessing as to what extent their profitability will be impacted by MFRS 9. Investors will only be able to see the early impact on the banks from the first quarter of FY2018. Analysts and credit rating agencies say banks have so far been unable to provide much clarity on the impact.

“It is too early to estimate the full effects of IFRS 9 on provisions, profitability and capital, as banks have been reluctant to disclose much beyond acknowledging that provisioning would need to be raised. For some markets, the change in accounting standards is happening at a time when banks are struggling to meet progressive increases in minimum capital requirements as Basel III is phased in,” Fitch Ratings observes in a report last week.

But in some markets, including Malaysia and Singapore, the financial impact on banks could be softened because their current regulatory frameworks either already involve elements of the expected-loss approach, or the banks hold reserves that regulators did not allow them to fully release when IAS 39 was first introduced.

“Regulators in most of these countries have also been progressively forcing banks to hold higher reserves, which will provide a buffer against potential losses. Nevertheless, the impact from moving to ECL is likely to vary from bank to bank even in the most prepared systems, reflecting the underlying riskiness of their assets and their own internal system capabilities,” says Fitch.

According to Ng, Malaysian banks are at different stages of readiness for MFRS 9. “I would say the larger ones would be more ready and started looking closely into the matter only in late 2015.”

Research house UOB Kay Hian Research, in a report on banks on Sept 30, says banks with large regulatory reserves (RR) relative to existing provision buffers will be able to utilise their RR to offset the increase in provision requirement emanating from the IFRS 9 adoption.

“This is of course subject to Bank Negara’s approval. This would place Public Bank Bhd in the strongest position to transit into IFRS 9 as its RR is equivalent to 125% of its total provision balance versus peers’ average of 40%,” it notes.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.