This article first appeared in The Edge Financial Daily, on June 10, 2016.

Hartalega Holdings Bhd

(June 9, RM4.04)

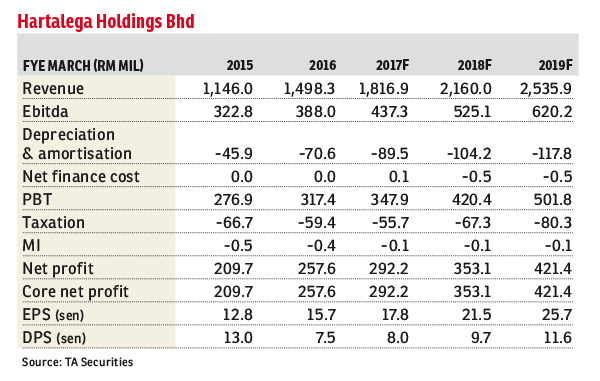

Maintain sell with an unchanged target price (TP) of RM3.90: Hartalega Holdings Bhd posted a surprisingly weak set of results in the fourth quarter of financial year 2016 (4QFY16). Although FY16 core net profit was stronger by 22.4% year-on-year (y-o-y), it plunged 39.9% quarter-on-quarter (q-o-q) and 22.1% y-o-y. Note that this was not due to lower sales volumes, but weaker average selling prices (ASP) of 17.3% q-o-q amid the backdrop of rising costs and the weakening US dollar to the ringgit by 9.6% q-o-q.

Having a concentrated clientele base with top 10 customers accounting for about 60% of sales, and considering the influx of new nitrile glove capacity in the market, the group had weaker bargaining power. Consequently, it had to accommodate a large number of customers’ requests for lower selling prices to tap into price sensitive markets in Europe. Above all, we had seen the group’s margins fall below that of the industry’s average for the first time since its listing.

Going forward, barring unanticipated cost pressures, we anticipate a gradual recovery in the group’s performance premised on several measures it had undertaken. First, ASPs have been revised upwards by 4% to 5% effective 1QFY17 to offset rising operating costs (i.e. natural gas) and the weaker US dollar relative to the ringgit. Although not a full cost pass-through, this would ease the pressure on the group’s margins. Second, its sales force has been ramped up to broaden its concentrated customer base. This measure has also resulted in the group’s utilisation rates trending higher in recent months and hence alleviating any concerns about stagnant sales volume growth in the near term.

Lastly, the commissioning of the Next Generation Integrated Glove Manufacturing Complex’s (NGC) Plants 3 and 4 remains postponed to 3Q of calendar year 2016 (CY16). We are positive on this measure as it would allow any short-term demand and supply imbalances to restore and price competition to taper down.

Our TP for Hartalega is maintained at RM3.90 per share based on an unchanged price-earnings ratio (PER) of 19 times and CY17 earnings per share of 20.6 sen. Although the ascribed PER is at a discount to its five-year forward PER of 20.3 times, it is still at a premium to the sector’s five-year forward PER of 15.9 times. We are positive on the group’s ability to deliver above-average industry margins over time as operations at the NGC are ramped up. — TA Securities, June 9