It is without a doubt that the Covid-19 situation has impacted global markets. It is an unprecedented event and many – including businesses – have been taken by complete surprise with the way things have been unfolding.

For example, the global aviation sector is forced to scale back their operations as people are no longer travelling. Non-essential businesses including real estate, construction, automotive, travel agencies and retail outlets have been forced to close.

Many businesses are now finding it hard to keep up with their monthly expenses. To help ease the burden, Bank Negara Malaysia (BNM) announced a six-month moratorium period for loans and mortgages.

However, even with the relief from lenders, it is envisaged that many individuals and businesses will still struggle to make ends meet. It is no longer business as usual, and the seriousness of the domino effect towards the end value chain i.e. households, must be recognised. When households are no longer spending, that’s when more businesses start to fail.

Below are some of the symptoms and issues a business may face:

- Downward trend in sales, earnings and free cash flow;

- Increased inventories - leading to obsolescent inventories;

- Increased supply chain risk;

- Tightening cash flow and strained working capital;

- Breaches in banking covenants;

- Creditor build up and non-payment of statutory debts;

- Deteriorating customer relationships and increasing risks of bad debts;

- Deferred payment of staff salaries; and

- Default notices for non-payment of loan, rent and/or leases, etc.

Cash flow management

Cash is king, and even more so in times of crisis. Liquidity will now be at the forefront of a company’s list of issues due to the exceptionally poor trading conditions. Given its importance, companies should immediately develop a treasury plan for cash management as part of their overall business risk and continuity plans. We set out below, 13 key priorities for consideration:

- Ensuring robust framework for managing supply chain risk – review the supply chain network and understand the financial risks of key trading partners, customs and suppliers who may be affected by the financial impact. For example, a company may want to consider acquiring its supplier who is in trouble to keep the supply chain and keep the goods and services going.

- Focus on cash-to-cash conversion cycle – with attention to three areas such as receivables, payables and inventory. The key is to minimise working capital requirements, where necessary.

- Keep financing options open – undertake cash flow scenario planning to understand how much cash the business needs. This includes taking the opportunity to actively engage financiers and explore possibilities with venture capitalist/funding agencies/private equity firms for new financing.

- Revisit capital investment plans – consider what is really necessary in the near term.

- Receivables management – early and proactive engagement with customers, shorter payment terms for discounts, debtor financing and factoring.

- Payables management – develop payable strategies such as eliminating early payments, prioritising critical suppliers, re-negotiating terms and supply chain financing.

- Inventory management – realigning inventory strategy i.e. push vs pull approach, consignment strategy, discounting slow moving/obsolescent stock and eliminate production bottlenecks to reduce WIP.

- Audit payables and receivables transaction – ensure that you are paying the right amount for goods and services procured, and collecting the right amount for goods and services sold.

- Alternate or non-traditional revenue streams – consider ways which the business could temporarily or permanently replace that revenue. For example, if you have assets you use to generate revenue, consider thinking how those assets are used to generate alternate revenue sources.

- Convert fixed to variable costs, where possible – review the need to swap fixed costs for variable costs i.e. sale and leaseback arrangement. Other considerations may include contract manufacturing, freight outsourcing and third-party warehousing.

- Review non-core assets/underperforming businesses – evaluate options when contemplating an exit strategy for underperforming and/or non-core areas of a business – whether to fix, sell or close. The amount of cash raised through divestment activities may be used to reinvest in other parts of the business.

- Stimulus package – consider whether your business is eligible for the various reliefs from the stimulus packages announced by the government.

- Corporate rescue mechanisms – consider the need to restructure debts by leveraging on corporate rescue mechanisms which are available in Malaysia (details covered below).

Corporate Rescue Mechanisms (CRM)

CRM can be broadly divided into two categories in Malaysia:

| Formal Process1 | Informal Process |

|

|

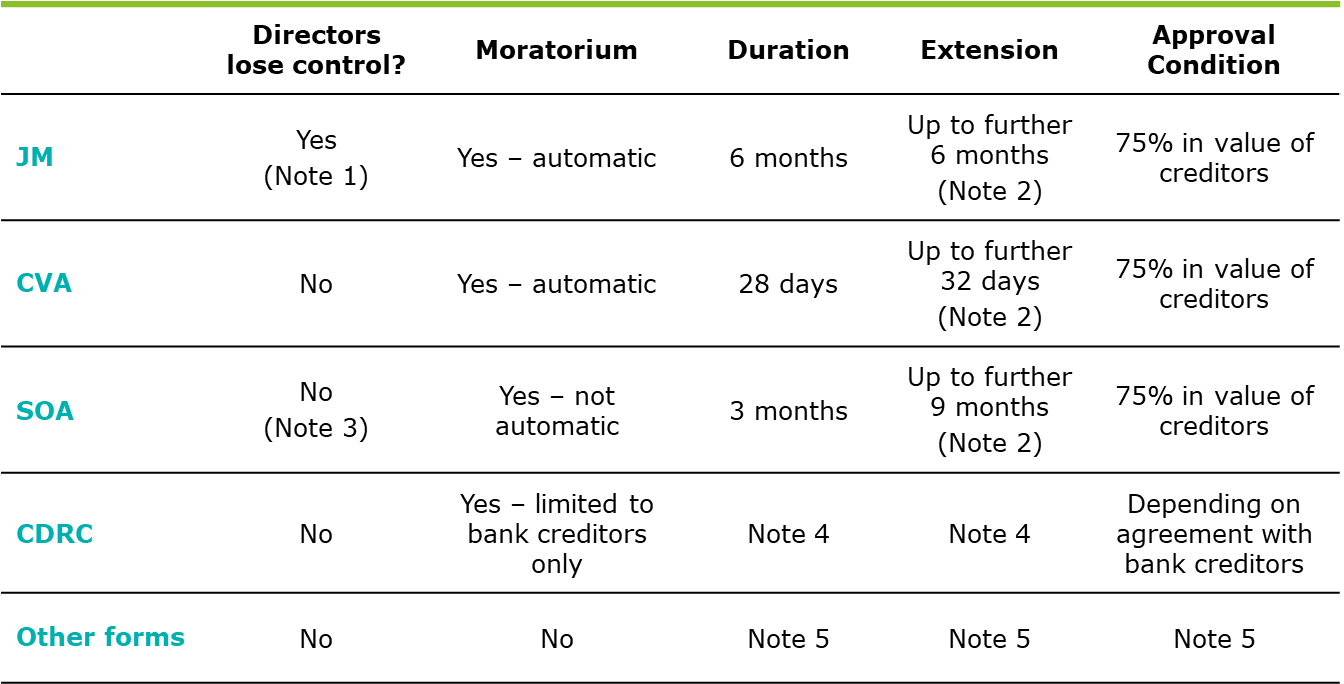

What is Judicial Management (JM)?

JM offers a way to rescue companies which are viable for financial rehabilitation, by giving the companies breathing space via an automatic moratorium and protection from legal proceedings. Essentially, a company under JM will be placed in the hands of an independent insolvency practitioner known as a judicial manager. The judicial manager, who is appointed by court and empowered with wide powers akin to that of a liquidator in a winding up by court, must possess among others a strong business acumen and risk management qualities as he/she aims to turnaround the business. One of the first priorities of a judicial manager would be to assume power and control from the directors and ensure that business disruptions are kept at a minimum while he/she formulates a restructuring proposal for the creditors’ approval.

A JM order has an initial term of six months. As such, the restructuring proposal must be put forward for the creditors’ approval during this period. If the judicial manager requires more time to do so, he/she may make an application to court for an extension of time of up to six months.

More importantly, the objective of the judicial management is to achieve the survival of the company, or the whole or part of its undertaking as a going concern. It also allows the company to achieve a more advantageous realisation of the company’s assets compared to a winding up situation.

Based on the Companies Act 2016, JM does not apply to companies regulated by the Central Bank of Malaysia and the Capital Markets and Services Act 2007. In addition, secured creditors can veto the application of JM order.

What is Corporate Voluntary Arrangement (CVA)?

As compared to JM, CVA is meant to be a quick and cost-effective rescue mechanism, with minimal court intervention. Companies are given an automatic moratorium of 28 days upon filing necessary papers, including terms of the voluntary arrangement proposal, to court.

Under CVA, the company shall appoint a nominee i.e. an insolvency practitioner, to work as a trustee or supervisor for the purpose of supervising the implementation of the voluntary arrangement. Essentially, the nominee’s powers and duties are confined to monitoring the company’s affairs for the purpose of forming an opinion as to whether the proposed voluntary arrangement has a reasonable prospect of being approved and implemented, and whether the company is likely to have sufficient funds available for the company during the proposed moratorium to enable the company to carry on its business.

Unlike JM, directors of companies under CVA still retain their powers to run the business during the moratorium period. If the company requires more time, it may request for an extension of up to 32 days (total of 60 days from commencement of moratorium). The relatively short time available to obtain an approval from creditors would mean that, companies need to work with the nominee and prepare the necessary ground work, even before the CVA application is filed to court.

Based on the Companies Act 2016, CVA does not apply to a public company, companies regulated by the Central Bank of Malaysia and the Capital Markets and Services Act 2007, and a company which creates a charge over its property or any of its undertaking. In view of these criteria, it appears that CVA would only be applicable to private companies without any secured borrowings.

What is Scheme of Arrangement (SOA)?

SOA is a rescue mechanism that has long existed before JM and CVA. Similar to that of a JM order, an SOA allows a company to propose a work out arrangement with its creditors in a court-ordered meeting. The stark differences would be that companies undertaking an SOA exercise do not enjoy an automatic moratorium (an application for a restraining order is required) and that the directors will still continue to be in the driver’s seat (only if the company is not under JM or under insolvency administration i.e. liquidation and receivership) to run the business, whilst formulating a restructuring proposal for the creditors’ approval.

A restraining order – once granted by court – has an initial term of not more than three months but it may be extended up to a further nine months. A company undertaking an SOA exercise will typically work with consultants including a restructuring advisor to turnaround the business.

Unlike JM and CVA, an SOA applies to all companies in Malaysia.

What is Credit Debt Restructuring Committee (CDRC)?

CDRC is a platform established in 1998 by BNM for companies to work out a debt restructuring plan with financial institutions, without having to resort to legal proceedings. In such situations, CDRC will act as a mediator between the borrower company and bank creditors. Should an application for mediation be accepted by CDRC, a standstill (for bank creditors only) shall take effect accordingly. It is understood that, as long as the file stays with CDRC, bank creditors i.e. participating institutions shall observe the standstill period in accordance with the CDRC Participants’ Code of Conduct. However, the borrower company may still face claims from other non-bank creditors, as the standstill does not apply to these parties.

When formulating a restructuring proposal, it is common for borrower companies to work with an Independent Financial Advisor (IFA). This usually provides certain comfort to the bank creditors – due to the IFA’s independence – and that the IFA comes in with a fresh pair of eyes to ascertain the issues faced by borrower companies and thereafter provide the recommended remedial steps, for the turnaround exercise.

In terms of eligibility, the CDRC route is applicable for listed PN17 or GN3 companies who has debts with financial institutions. It is also applicable for private companies who meet certain criteria set by CDRC i.e. the company must have at least two bank creditors and minimum bank debt of RM10m, amongst others.

Other forms of voluntary arrangement?

These relate to other informal arrangements which can be simple and cost effective to implement.

Examples would include entering into written arrangements via letters or agreements with one or certain groups of creditors to defer payments, reschedule payments, provide discounts, waiver, etc. This arrangement does not bind all creditors of the company unless the business is very small and the company is able to control all of its creditors.

CRM at a glance

Click / Tap image to enlarge

Regardless of which CRM a company may adopt, the company should ensure that it possesses a good business case for a restructuring exercise. A good business case may be established via performance improvement measures undertaken by the company, new money from white knights or investors, etc.

What’s next? Respond, Recover and Thrive

It is clear that the Covid-19 pandemic will have a devastating impact on the Malaysian economy, more so, the global economy. While it is uncertain as to when the pandemic will end, analysts are foreseeing that this impact will stay on for months or even years to come.

It is important that companies respond quickly and appropriately to minimise impact, recover, and emerge stronger as they thrive for success. In terms of responding – perhaps a good start would be to consider the 13 key priorities for cash flow management described in this paper and consider the need to leverage on an appropriate corporate rescue mechanism, if necessary.

Time is of the essence, and businesses should not take the sit and wait approach. As Sir Winston Churchill once said, “He who fails to plan, is planning to fail”.

By Malek Said, Executive Director, and Eddie Goh, Associate Director of Restructuring Services at Deloitte Malaysia. The views expressed above are solely theirs.

#dudukrumahdiamdiam and get the news at theedgemarkets.com.