This article first appeared in Capital, The Edge Malaysia Weekly on March 15, 2021 - March 21, 2021

FOR older investors, the rally in local equities last year may have brought back memories of the rip-roaring bull run of the 1990s.

The similarities between then and now include a buoyant market, high daily trading values and volumes, and almost everyone discussing what stocks to buy. But aside from the absence of the internet and social media then, there is one glaring difference: the strong presence of foreign funds in the local bourse then compared with now.

Tan Ting Min, former head of research at Credit Suisse, recalls attending nine meetings to promote Malaysian equities in New York City to various foreign funds in a single day at the peak of the bull market more than 20 years ago. But this is just a memory these days, even pre-Covid.

Private investor Andrew Lim concurs that the strong presence of foreign funds seen in the 1990s is missing from the local equity market. Most headed for the exit during the Asian financial crisis (AFC), with the imposition of capital controls and the Central Limit Order Book (CLOB) issue aggravating sentiment. Today, there are many foreign funds invested in Malaysian companies — even in mid-cap ones — but to these investors, local companies are just not as attractive as before when there are many more choices out there.

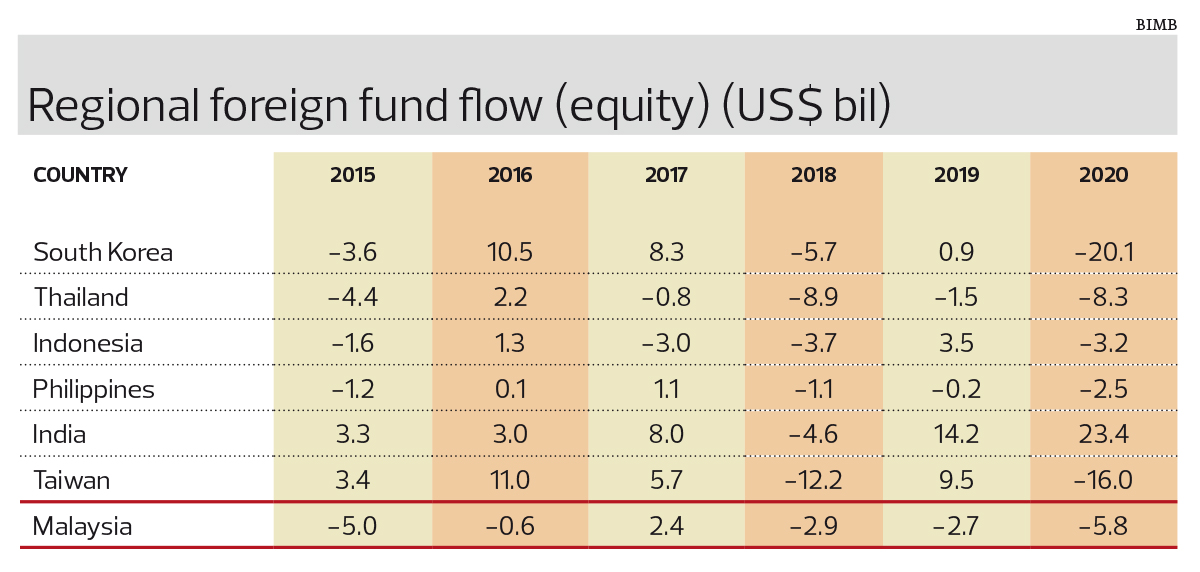

Indeed, if you follow the weekly fund flow reports from research houses, it seems that foreign investors are selling Malaysian stocks more than they are buying.

In 2020, according to MIDF Research, foreign funds were net sellers of local stocks to the tune of RM24.75 billion. In fact, foreigners were net sellers in all but one of the last six years (see table).

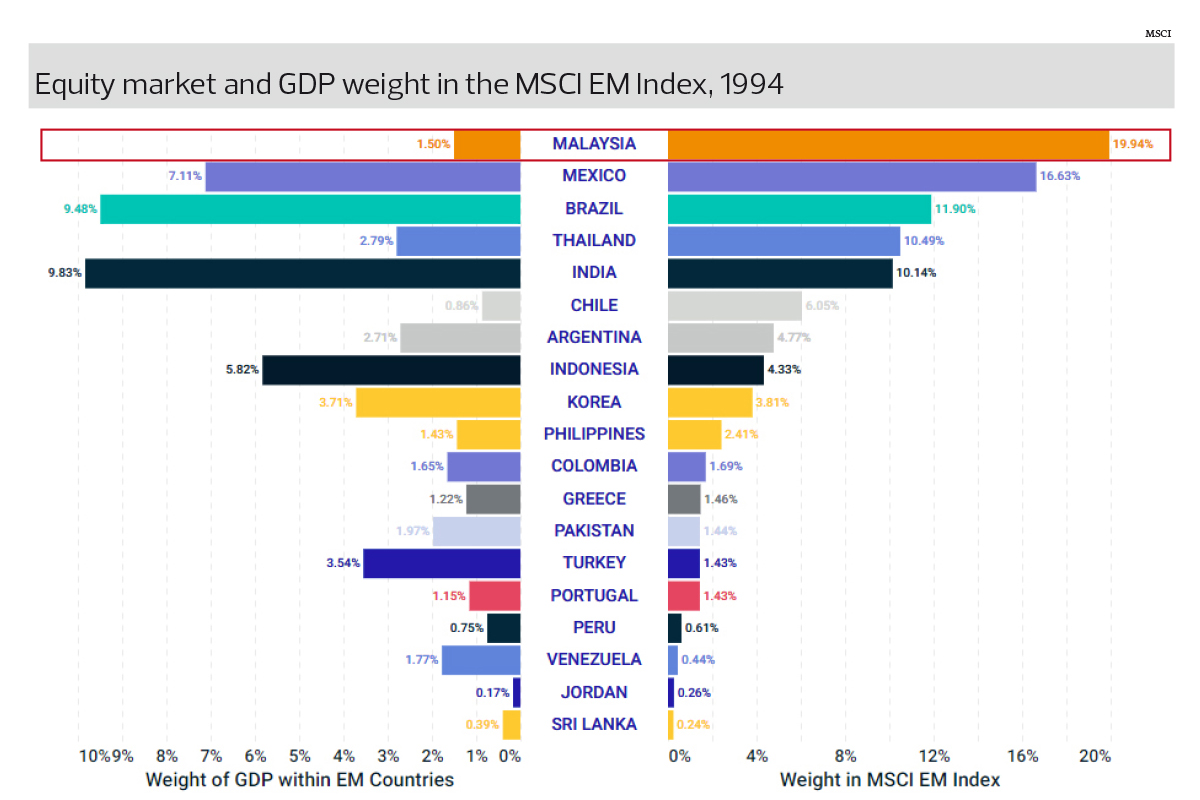

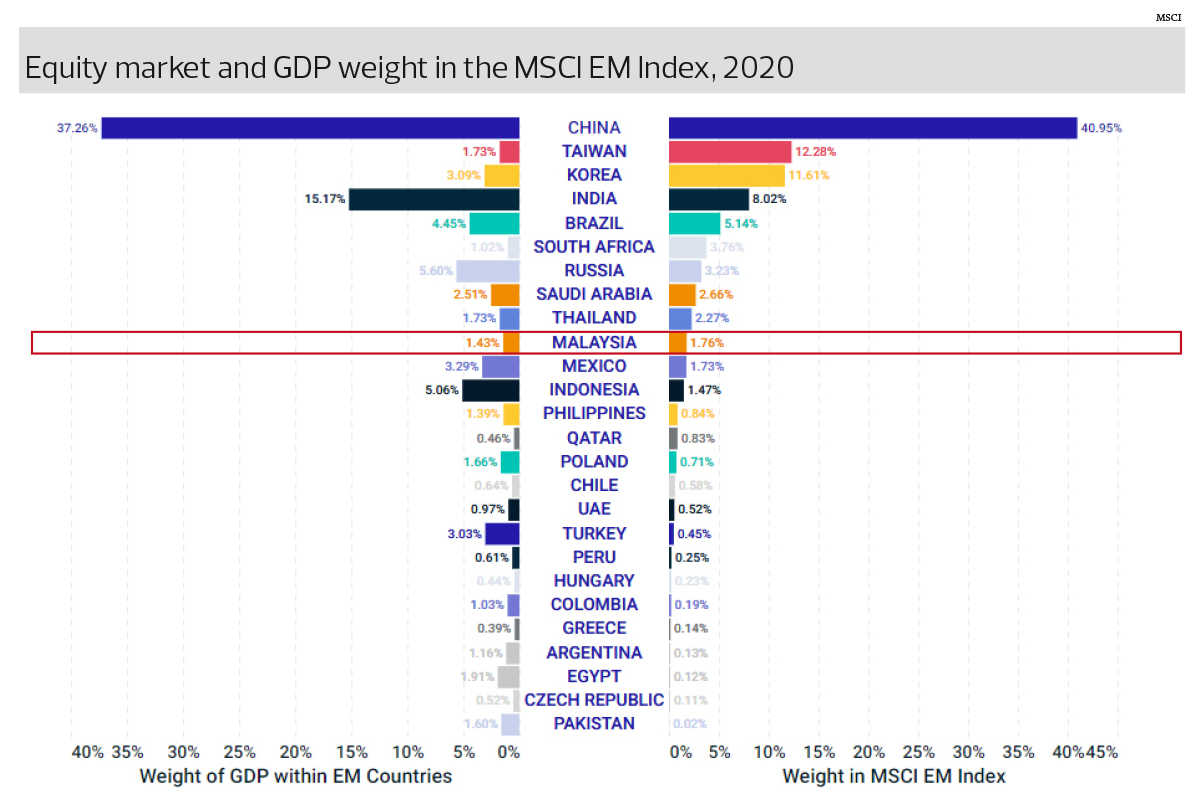

That Malaysian stocks are no longer sought after by foreign funds is not new. The country’s weightage in the MSCI Emerging Markets Index has been declining from 19.94% in 1994 to 1.76% in 2020. However, the corresponding decline in the weight of Malaysia’s GDP among EM countries has not been as steep, changing from 1.5% to 1.43%.

Why are Malaysian stocks so unloved by foreign funds?

“Malaysia’s falling weightage in the MSCI EM indices is primarily a function of Malaysia’s economy failing to keep up with other countries that are advancing. In the early 1990s, Malaysia was the ultimate Asian tiger, with economic growth that was unrivalled, matched with the fact that the Indian and Chinese markets were unimportant then.

“Today, the rise of China and India means that Malaysia’s market has been dwarfed and, therefore, its weightings will continue to deteriorate. The rising fear is that Malaysia will become a rounding error for foreign equity investors who don’t have to be in Malaysia. Sadly, we have seen a continuous outflow of foreign funds for many years,” says Tan.

At a weightage of only 1.76%, the risk of the country becoming a rounding error, which means funds can choose not to have any exposure to Malaysian equities, is very real.

Yeoh Keat Seng, a fund manager at fund management company Kumpulan Sentiasa Cemerlang Sdn Bhd, sees the irrelevance of Malaysian equities to international investors as one of the challenges facing the local bourse.

“A market that accounts for around only 2% of the Asia ex-Japan index is irrelevant because an international fund manager can afford to have zero weightage in this market and yet not risk benchmark tracking error because 2% is just too small a difference. Older investors will recall a time back in the 1990s when Malaysia accounted for 20% of the Asian index — that’s when Malaysia was relevant, but today it’s not,” he explains.

Tan, who left Credit Suisse in 2017 and now sits on the board of two listed companies, says foreign investors have been complaining about Malaysia’s unattractive earnings growth (a function of the stock market being primarily old economy), high valuations (as local institutional funds, especially the government-linked investment companies, are natural buyers in the local market) and poor liquidity (listed stocks are usually tightly controlled by entrepreneurs or GLICs).

And, recently, there was another complaint — the constant revamp of government policies with frequent changes in ministers and working teams.

Bank Islam Malaysia Bhd economist Adam Mohamed Rahim concurs, saying one of the reasons international investors seem to stay away from Malaysia’s equity market is the uncertain political landscape.

“Key reforms (economic and institutional) that could unlock further growth potential in Malaysia are likely to face risks of delay in a highly fluid political landscape. Because of this, foreign investors would then have dim prospects in terms of corporate earnings as fewer contracts are awarded to industry players. As such, international investors would go for markets that have a sense of stability as it would likely translate into predictable growth in corporate earnings,” he explains.

Lim notes that the many scandals in corporate Malaysia, such as 1Malaysia Development Bhd (1MDB), as well as the recent appointment of politicians to the chairmanship of certain government-linked companies, may be putting off foreign funds too.

“Foreign investors would hesitate to invest here because of a perceived lack of corporate governance. If we’re not careful, we will become irrelevant as we’re competing with Thailand, Indonesia and Vietnam. It shouldn’t be that way; we’re a big enough economy with a sizeable population,” he says.

A silver lining

Yeoh, however, sees a positive side to the problem.

“We have such a low weighting, with foreign fund managers being so underexposed to Malaysia, that just a small flow or spillover to emerging markets, Asia and Malaysia, will make a whole lot of difference, and that’s what we hope will happen this year,” he says.

To make Malaysian stocks more attractive to global investors, their fundamentals have to be a lot better.

“That means quality of business, earnings growth, calibre of management and so on. There are so many areas that could be done better — encouraging businesses to be competitive internationally instead of sticking to the 1980s/90s model of import substitution, having protected industries, monopolies and cartels [as well as] political patronage; meritocracy in management; less government and political involvement in listed companies and so on.

“Many of our KLCI index companies and some of our largest companies can claim to have significant foreign shareholdings, but I would say in most instances, that’s due to their size rather than inherent business or growth appeal. The companies that have done the best in recent years have almost all been private sector-driven, exporters or have international businesses and are competitive on their own accord without government support or subsidies. I don’t think that’s a coincidence,” says Yeoh.

Tan is less optimistic and sees an uphill task in making the Malaysian stock market more attractive to foreign funds.

“Although it is very difficult to make Malaysia attractive relative to the developing giants of India and China, individual sectors or stocks can be interesting enough to attract foreign money, for example the glove sector during the pandemic. In the early 1990s, the gaming (as Macau and Singapore were still small) and the plantation sectors (before environmental, social and corporate governance factors were in the spotlight and fake news trumped science) were seen as unique and interesting sectors to invest in in Malaysia,” she says.

Since the AFC, Malaysia has increasingly become a bottom-up market where stock picking is particularly important, rather than a top-down market, Tan adds.

Tan started analysing Malaysian equities in the 1990s and remembers the heyday when stocks on the Kuala Lumpur Stock Exchange (before it was demutualised and renamed Bursa Malaysia) were highly sought after by foreign funds.

“In the early 1990s, stocks would rally at the mere whiff of an MoU (memorandum of understanding) rumour with China or an expansion into gaming or timber businesses in exotic places. Then, Malaysia’s moment in the sun was when its stock market volumes were higher than the New York Stock Exchange,” she recalls.

But today, retail investors are far more discerning, with information readily available on the internet and in widely distributed equity research reports, making it easier for them to make educated decisions on stocks. “Moreover, I have not heard any stock tips from taxi drivers or wet market vendors yet, so I believe the market is less exuberant or speculative than it was in the 1990s,” she quips.

For Yeoh, the strong surge in retail account openings today compared with then is one of the key differences observed. Also the demographics of the new investors are different — much younger and with relatively less trading experience. Moreover, a significant portion of these retailers trade online (thanks to the emergence of online brokerages such as Rakuten Trade and i*Trade@CIMB), unlike their dependence on remisiers in the past. Also, brokerage is a lot lower today.

Interestingly, he notes that the level of syndicate involvement and speculation seems to be substantially lower today compared with in the 1990s.

As to where Yeoh is putting his money, he is bullish on China.

“I think China has increasingly become and will continue to be one of the most important markets in the world for many reasons: robust economic growth, world-class companies and leadership in many sectors, including e-commerce, technology, renewable energy, electric vehicle batteries and EVs,” he says.

In addition, foreign funds continue to flow into China as the country’s weighting in global indices such as the MSCI Asia ex-Japan and MSCI EM continues to increase, owing to the growth of these companies, the continued listing of multi-hundred-billion-dollar companies such as Ant Group and Kuaishou, as well as the return of many Chinese companies currently listed as American depositary receipts (ADRs) to the China and Hong Kong markets, Yeoh explains.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.