Loan growth to accelerate this year, boosted by demand from businesses when the economic recovery starts to gather steam.

KUALA LUMPUR (Feb 11): Most banks pulled the brakes on declaring dividend in the first three quarters of 2020 globally given the unprecedented uncertainties that the Covid-19 pandemic has brought to the world.

However, analysts are inclined to believe that Malaysian banks are likely to declare dividends, albeit lower, when they release the fourth quarter financial results. The view is formed on the premise that most local banks have demonstrated their financial strength to withstand the current economic crisis.

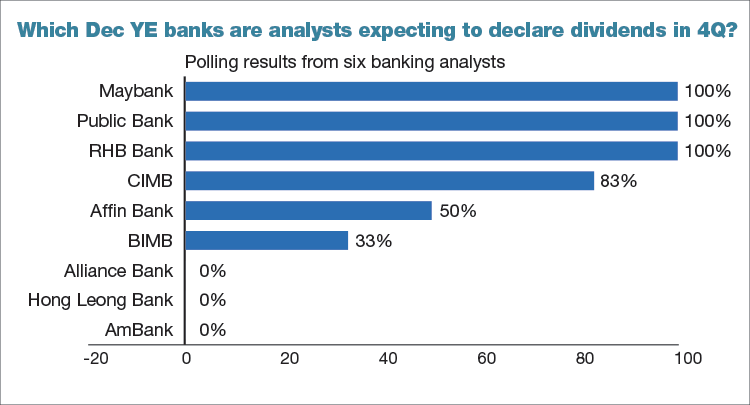

Except for Malayan Banking Bhd (Maybank), BIMB Holdings Bhd and RHB Bank Bhd, all other listed banks did not declare any interim dividends in the January-September period.

Nomura head of equity research Tushar Mohata said banks that are reporting full-year results this month should be able to declare dividends as they have healthy capital buffers and banks have taken measures to preserve asset quality through assistance measures.

Furthermore, Tuushar said the overall increase in credit costs was manageable in 2020. Hence, most banks will remain profitable but with much lower return-on-equity (ROE).

“[For] banking stocks, being a large holding for local asset managers and pension funds, a minimum level of dividend payout is important for the latter’s investment income,” said Nomura.

However, he believes that the quantum of dividend payout should be lower than pre-Covid days in the spirit of conservatism, adding that some banks might also resort to dividend reinvestment plans (DRPs).

AmInvestment Bank Bhd analyst Kevin Ong explained that the pause on dividends from the banks was due to the blanket moratorium imposed last year, which in turn clouded the earnings visibility as well as the banks’ loan performance.

“When a substantial portion of your loans is under the automatic blanket moratorium, it is not very clear about the capability of repayment from these borrowers,” said Ong, noting that at least 80% of SMEs were under the blanket moratorium.

The current targeted assistance will enable banks to have a better gauge on their loan portfolio. Consequently, banks would be more comfortable to declare dividends compared with six months ago.

According to Ong, the CET-1 (Common Equity Tier 1) ratio of all the banks has exceeded the minimum requirement, which puts them in a comfortable position to declare dividends. For the conservative banks, they may opt for a higher portion of DRPs instead of handing out cash dividends as they would want to retain their capital position.

A banking analyst, who declined to be named, commented that if the CET-1 ratio is comfortably at above 13%, there should not be much regulatory push back against the backdrop that banks have managed credit risk reasonably well.

The analyst noted that Maybank, Public Bank Bhd and RHB Bank have the largest capital buffer among those with financial year ended Dec 31.

Banking sector’s prospect still intact for now

While the Government has reimplemented a Movement Control Order (MCO 2.0) in all States, except Sarawak, currently, analysts do not expect the impact on the economy to be as great as the previous MCO.

MIDF Amanah Investment Bank Bhd research head Imran Yassin expects banks’ earnings to rebound this year given that bad loan provisions might lessen. Besides, net interest incomes have stabilised among the banks, which will provide support to earnings.

“We expect loan growth to accelerate this year, boosted by demand from businesses when the economic recovery starts to gather steam. This is despite the MCO 2.0 as it is less restrictive than the MCO we faced last year,” said Imran.

“We may fine-tune our earnings expectation lower, but overall, we opine that the earnings prospects remain intact,” Imran added.

Hong Leong Investment Bank Bhd banking analyst Chan Jit Hoong concurred with the view, noting the impending Covid-19 vaccination rollout as positive for the banking sector.

“It is only a matter of time when the market looks forward again to economic activities returning to the path of normalcy. Thus, we remain positive on the sector and would advocate buying on dips — valuations are undemanding and there is ample liquidity in the market,” said Chan.

Nomura’s Tushar expects a V-shaped earnings recovery for banks in FY21, due to the absence of day 1 modification loss, flat to positive margin trends as overnight policy rates stabilise, and lower absolute provisioning required given the front-loading of the bulk of the provisions in FY20.

“However, our preference remains towards retail banks as we believe based on our stress test that their asset quality faces less downsides from the Covid-19 pandemic, and they are likely to enjoy more tailwinds from the modification-loss unwinding,” said Tushar.

He added that the recent stress test by the Central Bank also points to the bulk of impaired loan formation in 2021 to come from businesses, along with about 90% of incremental Covid-19-related credit costs. Nomura’s top picks are Public Bank, Hong Leong Bank and RHB Bank.

Meanwhile, Affin Hwang Capital analyst Tan Ei Leen views that banks have been cautious of high-risk segments since 2020 and had set aside some pre-emptive provisions, adding that banks may continue to expect a certain degree of asset quality deterioration in 2021.

However, the research firm continues to maintain an elevated provision level, though lower at 62bps versus 80bps in 2020.

“We believe that even if MCO 2.0 is extended to a period of one to two months, it may not necessitate a significant downward revision in our earnings forecasts (unlike the previous year),” said Tan.

However, should the MCO last more than three months, Tan said this could raise the net credit cost (NCC) assumption by another 10bps.

“The estimated impact on sector earnings is -5.9% with a 10bps increase in NCC, -11.8% with a 20bps increase and -17.7% with a 30bps increase,” Tan noted.