This article first appeared in Personal Wealth, The Edge Malaysia Weekly on June 1, 2020 - June 7, 2020

Passive investing has become increasingly popular in recent years, with many investors adopting a buy and hold strategy or putting their money in low-cost index funds. However, the current market volatility presents opportunities to those willing to take on a more active approach as they can pick up stocks whose prices have tanked since March.

In the US, the S&P 500 plunged 29% to 2,257.4 points on March 23 from the start of the month before rebounding to 2,951.65 points on May 19 while on the home front, the FBM KLCI fell 16% to 1,219.72 points on March 19 from the beginning of the month before recovering to 1,421.28 points on May 19.

In fact, investors should consider using both active and passive investing strategies to capitalise on the available opportunities, rather than just sticking to one approach, say industry experts and investors. Their options include investing directly in markets that are less efficient, selecting stocks that they are familiar with or putting their money in a mix of actively and passively managed funds.

Chong Lee Choo, director of Innovation Lab and alternative investment at Affin Hwang Asset Management Bhd (AHAM), says that on a broader level, investors can consider active solutions when there is a potential to add alpha, especially in emerging markets, where there are more opportunities to uncover undervalued stocks. “For developed markets, where outperformance is difficult to come by, investors can look at passively managed funds such as exchange-traded funds (ETFs) to gain broad exposure to them, and to do so more efficiently.”

She adds that investors should emphasise the underlying exposure of their investment strategies, as opposed to merely considering whether a strategy is active or passive. “Active and passive strategies do not need to be mutually exclusive of each other. A savvy investor would seek to blend both approaches.

“Instead of deliberating between active or passive, investors should consider whether they have the right combination of asset classes (such as equities, bonds and commodities) that can provide them with diversified exposure across sectors and geographical markets.”

Chong Kaw Choi (better known as KC Chong), a certified financial planner and the author of Invest like a Stock Market Guru: The Complete Value Investing Guide that Works, says some investors use ETFs to gain exposure to large-cap stocks in developed markets such as the US, which they may not be familiar with. He points out that indices like the S&P 500 are very efficient. Various reports have noted that many large-cap funds that benchmarked their performances against the S&P 500 underperformed the index.

The SPIVA scorecard, recently published by S&P Global Inc, showed that 71% of US large-cap funds underperformed the S&P 500 last year. It also noted that 89% of US large-cap funds had lagged behind the index over the past decade.

KC says this is not surprising as many funds that invest in large-cap stocks in the US use the S&P 500 as their benchmark, which makes it challenging for fund managers to identify good investment opportunities in this space. The existence of high-frequency trading firms that trade US stocks at high speeds and high volumes also makes the market more efficient than others.

“It is hard for US fund managers to consistently find large-cap stocks that have been mispriced. Nobody can make extraordinary returns in such a space unless they take on more risk,” he says.

“[In addition], considering the fees that the large-cap funds in the US impose on investors, many of these funds should underperform the index. It is a no-brainer.”

However, the stock prices of small and mid-cap companies in the US tend to be less efficient and hence, provide more opportunities for active investors to bargain-hunt. There are also many markets around the world, including Malaysia’s, that are not as efficient as the US market. These are some of the areas in which investors can invest actively, says KC.

“Many smaller-cap stocks in the US are not actively followed by many analysts and fund managers. Then, there are the smaller markets around the world, such as Bursa Malaysia, that are less efficient,” he adds.

“For instance, The Busy Weekly, a rather famous Chinese investment magazine, once posted a list of 20 small and mid-cap stocks in Malaysia that generated returns of 1,000% each from September 2007 to 2017. The FBM KLCI gained 52% during the same period.”

Restructure portfolios when markets correct

Meanwhile, Lim Tze Cheng, head of research at EquitiesTracker Holdings Bhd and a former fund manager, says investors who invest directly in stocks “should be the most active” during a market correction to restructure their portfolios.

In March, when the Movement Control Order (MCO) was imposed to contain the Covid-19 outbreak, Lim seized the opportunity to restructure his portfolio. In addition to taking profit and cutting losses, he compared his holdings with other good stocks in the market that he had been monitoring. Then, he sold some of his stocks that had weaker fundamentals due to the outbreak and bought into companies with better potential.

“If you had been investing directly in the stock market before the coronavirus outbreak, there would have been some stocks that you liked but were hesitant to buy due to the high valuations. It is in challenging times that the share prices of these companies fall to a reasonable level,” says Lim.

“In March, I compared my stock holdings with those I had been monitoring but did not own yet. I compared their valuations and fundamentals. When I found some more attractive stocks out there, I sold some of my holdings and replaced them with other stocks that I had been monitoring.”

Lim has been bullish on semiconductor companies over the past few months and he remains so during this period as he believes this sector will benefit from the Covid-19 pandemic. He says the outbreak has accelerated the pace of digitalisation globally and there will be a need for much faster internet speeds in the next three to five years.

“5G technology is the key driver in the semiconductor sector. Some say the implementation of 5G is a luxury project for many countries, [and that] the pandemic will slow down its progress. But I have a contrarian view,” says Lim.

“I think the progress of 5G technology to be implemented will speed up in the next five years as more people realise the importance of having high-speed internet. Things like video conference calls, for instance, are becoming much more popular and they will require faster internet connectivity. Local semiconductor companies, including those that provide outsourced and test services (OSAT) and test equipment, will be the beneficiaries of such a trend.”

Lim considers himself a buy-and-hold stock picker. He says he adopts the Warren Buffett style of investing, where he holds on to stocks for as long as possible, provided that the fundamentals of the companies do not change. However, he prefers to be more “passive” after he has restructured his portfolio.

“By saying that I am a passive investor, I mean that I do not trade stocks actively by timing the market because it is impossible to do so. A very good example of this was how people were trading during the market correction in March,” says Lim.

“If you [are the kind of investor who] trades actively, you would have sold some of your stock holdings when the prices started to fall. This is how the fund managers of some actively managed funds tend to react.

“However, when the market subsequently rebounded, some stock prices recovered quite a lot. Some fund managers may have suffered more losses by not being ‘passive’ and staying put.

“I was a fund manager for a decade. I have learnt that it is impossible to predict whether the market has already bottomed or if it is going to rally. So, it is better to stay invested [in good quality companies].”

KC, an active investor who invests directly in stocks, agrees with Lim’s view that a market correction presents investment opportunities. However, he believes people should not underestimate the impact of Covid-19 on the global economy.

“Many people have died from the virus and it has had a huge impact on the global economy. A vaccine for Covid-19 could still be a long way off,” he says.

“Many economists, fund managers and renowned investors have pessimistic views of how the global economy will perform going forward. Many of them think a deep recession is looming and that some industries and businesses will take a long time to recover while others may not recover at all.”

Thus, active investors who want to take advantage of the current market correction should make a thorough assessment of their financial situation and risk profile, says KC. “They should ask themselves whether they are in a strong personal financial position. Do they have a relatively stable business or career [if a recession occurs]?

“They also need to ask how much cash they have set aside for investment in the years to come. Will they be able stomach market volatility and sleep well if their investments are down 20%? If their answers are yes to these questions, they can consider nibbling in the market.”

However, investors who are not in a strong financial position or have good financial knowledge should avoid investing right now, he adds.

On a personal level, KC likes companies with stable earnings, cash flows and strong balance sheets. He tends to favour stocks in the healthcare, consumer staples and technology sectors. He also likes those that offer high dividend yields, particularly in a low interest rate environment. Meanwhile, he avoids the airline, hospitality and oil and gas sectors, unless the stocks are at exceptionally low prices

Although KC is an active investor, he says passive investing strategies and financial instruments are more suitable for retail investors in general. “The statistics show that 90% of retail investors lose money in the stock market due to several reasons. These include a lack of skill and experience or blindly following rumours or hype. They tend to follow the wrong path and end up speculating or gambling in the stock market rather than investing. I used to be one of them.

“Hence, I believe that passive investing in the global market is best suited for most people if they wish to see better returns from the equity market [in the long run]. Making returns slightly below the index is better than losing money [as a result of speculation].”

Continue to apply dollar cost averaging

Passive investing has been gaining traction. Last year, the assets under management of passively managed equity funds in the US overtook those of their actively managed counterparts for the first time in history.

It should be noted that even Buffett, the legendary value investor and stock picker, has regularly recommended index funds to the everyday investor. In February last year, he was reported to have instructed the trustee in charge of his estate to invest 90% of his money in index funds tracking the S&P 500 for his wife upon his death.

Passive investors and those who have passively managed portfolios should continue to apply dollar cost averaging, says Wong Wai Ken, country manager of StashAway Malaysia. “We advocate such an approach as we do not think it is possible to time the market. It is better to stay invested over the long term. We believe the market will always go up over the long term, so dollar cost averaging will work out well.”

However, investors who have adopted a passive investing strategy can be slightly more active if they have a cash buffer prepared for challenging times and extra money to invest. For instance, those who invest in StashAway and others who invest directly in ETFs can deploy their extra cash into the markets when the indexes of those markets fall to certain levels.

“Let’s say you set a target that when the markets are down 10%, you want to invest more, using your extra cash. Since you are a long-term investor, you would always want to invest more when the markets correct,” says Wong.

“Some of our users who did so in recent months brought their average cost down and will enjoy better returns when the markets rebound to their previous levels.”

As at April 30, StashAway portfolios that invested in multi-asset and global markets had generated returns of between -3.2% and 3.2% year to date. Last year, it saw returns of 16.4% to 33.4%, says Wong.

Recently, StashAway rebalanced the asset allocations of its portfolios to be more conservative and less US-centric. Wong says this more conservative approach was adopted to manage the higher level of global economic uncertainty. The less US-centric approach is based on expectations that the US dollar will weaken and benefit emerging markets in Asia.

“We foresee some devaluation of the US dollar as we expect the US Federal Reserve to continue easing its monetary policy. A weaker US dollar could benefit emerging markets in Asia. We also see that Asian stocks in general are undervalued,” he says.

Additionally, StashAway has bought into an ETF that tracks the performance of China-based internet companies. Wong says the Covid-19 outbreak has had less impact on technology companies and they may see a faster recovery from the economic downturn than companies in other sectors. “We also like the fact that this particular ETF — the KraneShares CSI China Internet ETF — is less dominated by state-owned enterprises.”

StashAway has increased its weightage for gold from about 15% to 20%, depending on the investors’ risk profile. “We already liked gold because of a weakening global economy and US dollar. Now, we love it,” says Wong.

AHAM’s Lee Choo says low-cost and passive financial instruments such as ETFs will remain relevant to investors in the current low interest rate environment, where returns are hard to come by. “It would be prudent for investors to consider the fees and charges they incur when making an investment decision.”

She adds that the passive investing wave has caught on globally in recent years, but Malaysia seems to be lagging behind. For instance, there have only been 16 ETFs listed on the local bourse since 2005. “The poor breadth of product offerings cannot attract sufficient interest from investors.

“It is also due to an overall lack of awareness of ETFs and how they can be employed as part of an investor’s portfolio. This, in a way, has created a vicious cycle. The low interest and participation of retail investors has deterred ETF issuers from listing new ETFs.”

AHAM offers several ETFs, including the TradePlus Shariah Gold Tracker, which is backed by physical gold. As at May 27, its year-to-date return was 17.94% while its one-year return was 38.2%, according to Bloomberg.

How some active and passive equity funds have performed in 2020

As at April 30, 58 of the 82 unit trust funds that invest primarily in Malaysian large-cap companies had underperformed the FBM KLCI year to date, according to data provided by Morningstar Inc, a global financial services firm based in the US. This also means 70.73% of the large-cap funds underperformed the benchmark index in the first four months of this year. The funds’ performances do not take into account the sales charges of up to 6% imposed by the asset management firms and unit trust agents.

The top three performing funds during this period were Areca Dynamic Growth 2.0 (36.28%), Areca Astute Assets (-3.21%) and InterPac Dynamic Equity (-4.4%). By comparison, the FBM KLCI was down 11.39% during the corresponding period.

However, over a 12-month period, 59 out of the 82 Malaysian large-cap funds outperformed the FBM KLCI as at April 30. This means 71.95% of the actively managed large-cap funds outperformed the benchmark index during this period.

The top three performers during this period were Areca Astute Assets (3.06%), Public Islamic Alpha-40 Growth (-3.03%) and Public Islamic Sector Select (-3.7%). The FBM KLCI shed 14.28% during the corresponding period.

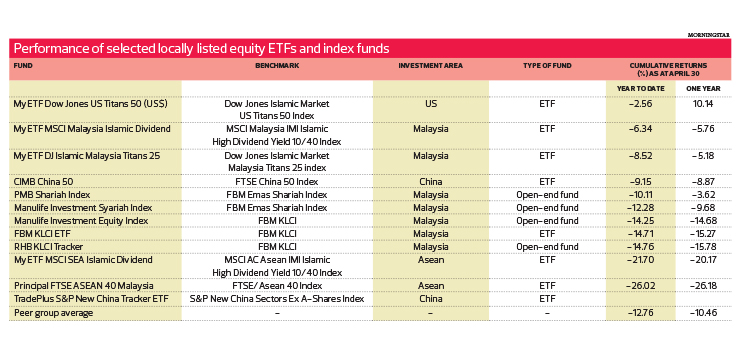

On a separate note, the best performing locally listed equity exchange-traded funds (ETFs) and index-tracking funds year to date (as at April 30) were the MyETF Dow Jones US Titans 50 (-2.56%), MyETF MSCI Malaysia Islamic Dividend (-6.34%) and MyETF Dow Jones Islamic Malaysia Titans 25 (-8.52%).

Over the one-year period, the best performers were the MyETF Dow Jones US Titans 50 (10.14%), PMB Shariah Index (-3.62%) and MyETF Dow Jones Islamic Malaysia Titans 25 (-5.18%).

The other locally listed non-equity ETFs not included in the Morningstar list are TradePlus Shariah Gold Tracker and ABF Malaysia Bond Index Fund. The list also excludes inverse and leveraged ETFs such as the Kenanga KLCI Daily 2X Leveraged ETF, Kenanga KLCI Daily (-1X) inverse ETF, TradePlus HSCEI Daily (2X) Leveraged Tracker, TradePlus HSCEI Daily (-1X) Inverse Tracker, TradePlus NYSE FANG+ Daily (2X) Leverage Tracker and TradePlus NYSE FANG+ Daily (-1X) Inverse Tracker.

Chong Lee Choo, director of the Innovation Lab and alternative investment at Affin Hwang Asset Management Bhd, says inverse and leveraged ETFs have blurred the line between active and passive financial instruments. “These newer types of ETFs provide investors with exposure to overseas markets and are meant to be traded like active instruments.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.