This article first appeared in Personal Wealth, The Edge Malaysia Weekly on August 24, 2020 - August 30, 2020

Shariah-compliant investments are known to be resilient and even tend to perform better than their conventional peers in troubled times. This was proven during the first half of the year, when the average returns of global and Malaysian equity shariah funds were higher than those of their conventional counterparts.

According to data by Morningstar, Malaysian equity shariah funds in the large-cap and mid- and small-cap categories provided average returns of -3.47% and -5.03% respectively from January to June 30. In comparison, Malaysian equity funds in the same categories provided average returns of -5.58% and -8.3% respectively. Shariah funds that invest in the broader Asia-Pacific ex-Japan region returned -1.38% over the same period, compared with their conventional counterparts’ -7.60%.

Year to date (as at Aug 12), shariah funds are still outperforming their conventional peers. Malaysian equity shariah funds in the large-cap and mid- and small-cap categories provided average returns of 7% and 13.11% respectively. In comparison, Malaysian equity funds in both categories provided returns of 5.87% and 6.55% respectively. Islamic funds that invest in the Asia-Pacific ex-Japan region returned 10.85%, compared with their conventional counterparts’ 1.67%.

Meanwhile, global Islamic equity funds outperformed their conventional peers, albeit marginally, according to Lipper’s data for the six months ended Aug 7.

The performance of most asset classes took a big hit in the first quarter of the year as there was almost zero economic activity owing to the lockdowns imposed by governments around the world to stem the spread of the Covid-19 pandemic. Akmal Hassan, managing director of AIIMAN Asset Management Sdn Bhd, says against this backdrop, few asset classes were spared from the volatility.

“Similarly, the performance of shariah funds was also impacted. However, the shariah space fared relatively better due to the exclusion of the conventional banking, gaming, tobacco and alcohol sectors, which took a big hit and are likely to see a delayed recovery,” says Akmal.

Ismitz Matthew De Alwis, executive director and CEO of Kenanga Investors Bhd, notes that shariah funds in general have outperformed due to their lack of exposure to the banking sector and a higher weighting in defensive sectors such as healthcare and telecommunications. “As such, shariah funds in general have outperformed. Going into a recovery, the shariah outperformance could reverse as cyclical sectors such as banks rebound faster,” he adds.

PMB Investment Bhd chief investment officer Isnami Ahmad Mohtar says the performance of its funds, which are all shariah-compliant, was affected by the various market-moving events happening within the year. While the performance of its funds was affected when their net asset value (NAV) per unit declined between 13.44% and 25.39% in the first quarter of 2020, performance recovered in the second quarter, when it increased between 13.66% and 41.92%.

Amid the market volatility, BIMB Investment’s funds have been doing relatively well year to date, says Najmuddin Mohd Lutfi, CEO of BIMB Investment Management Bhd. Its BIMB i Growth fund, for example, returned 63% and 16.94% in the three- and six-month periods (as at June 30) respectively, outperforming the Equity Malaysia category, which gave average returns of 20% and -2.75% in the three- and six-month periods respectively.

Despite the unfavourable market conditions earlier this year, some fund houses did see a significant increase in the assets under management (AUM) of their shariah-compliant funds in the first half of the year. The country’s Islamic fund management industry has managed to maintain its position in terms of AUM and NAV, even though the total size of the capital market has shrunk since the Covid-19 market rout in March, says Akmal.

“Speaking for ourselves, we are in a better position today compared with when we started the year. The total assets under administration of AIIMAN grew 5% from RM17.4 billion at the start of 2020 to RM18.3 billion (as at June 30). We saw some flows returning, especially from the institutional side. Institutional investors were looking for sources of diversification to provide stability in their portfolios through quality sukuk. Hence, we saw some inflows into our fixed income funds,” he says.

A similar trend was also seen within the retail market segment, he adds. According to him, many retail investors are opting for better returns by looking to invest in unit trust funds rather than keeping their money in savings and fixed deposits.

“This is especially as interest rates are expected to stay lower for longer. Hence, many retail investors were taking the opportunity to dollar cost average during the market downturn, which explains the inflows into our shariah equity funds,” says Akmal.

BIMB Investment and PMB also saw significant fund inflows over the past few months. Najmuddin says the AUM of BIMB Investment’s shariah equity funds was up 20% between April and June while Isnami says PMB saw its AUM increase 15.6% from RM1.15 billion in March 2020 to RM1.33 billion in May 2020.

What the funds are looking at

Moving forward, the shariah funds will continue to focus on sectors such as technology and healthcare, as well as industrial (specifically, glove manufacturing) and the internet sector.

As markets approach the recovery period, Akmal says the team will be looking to switch into different sectors that are showing recovery. For the domestic market, the team will be keeping a close eye on how the government plans to further stimulate the economy. Sectors that the fund house will be monitoring include property, e-commerce and manufacturing.

For the Asian market, the fund house favours the internet, e-commerce and technology sectors, says Akmal. This is due to consumers modifying their behaviours and adopting technology solutions such as cloud computing.

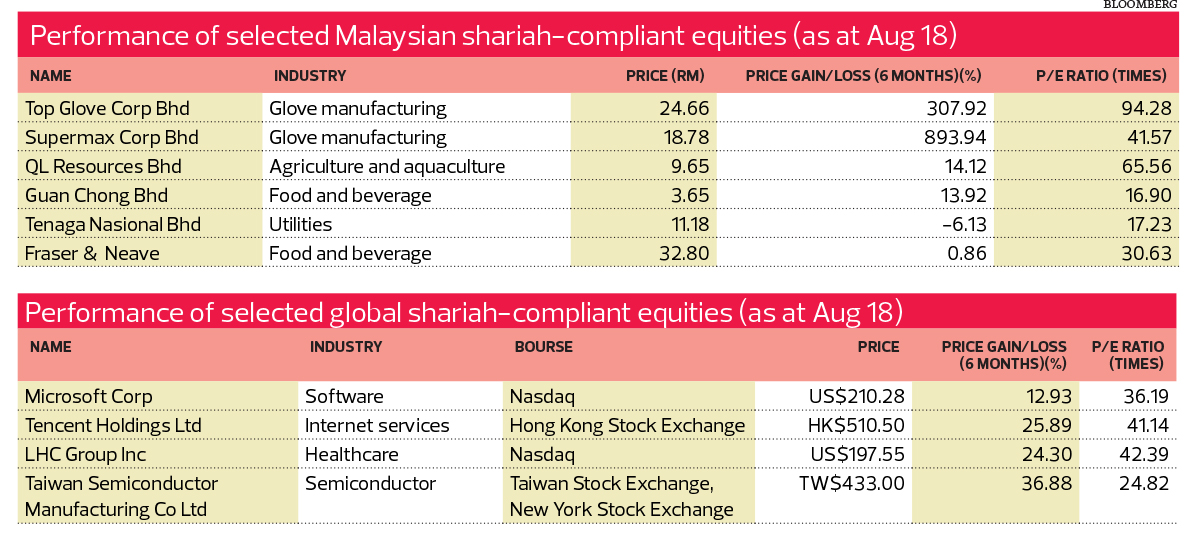

According to Affin Hwang AIIMAN Growth’s July fund fact sheet, the top holdings of the Malaysian Equity Islamic fund were Top Glove Corp Bhd, Supermax Corp Bhd, Tenaga Nasional Bhd (TNB), Axis Real Estate Investment Trust and KLCCP Stapled Group Stapled Security. Akmal says the glove stocks are expected to show earnings growth momentum versus other sectors.

“The recent volatility is mainly due to sentiment being affected by the news of the vaccine from Russia, the contra trading ban by a small broker and high retail participation. Nonetheless, the fundamentals of the glove makers are intact,” he adds.

Meanwhile, TNB, Axis and KLCCP should be relatively stable, given their earnings clarity and stability, says Akmal. He adds that their share prices are also supported by dividend payouts.

For global equities, some of the top holdings of AIIMAN Global Equity fund, according to its August fund fact sheet, are Microsoft Corp, Tencent Holdings, LHC Group and Taiwan Semiconductor Manufacturing Company (TSMC). As Tencent is one of the largest e-wallet and cloud services companies in China, its e-wallet and cloud services businesses will see strong growth in the long term, says Akmal.

Microsoft, on the other hand, will benefit from long-term corporate migration from offline servers to cloud servers. Its software products are highly recurring and sticky, notes Akmal. He also thinks that home health service provider LHC Group will continue to gain market share as its business is highly stable and defensive, even in recessions.

AIIMAN Asset Management is also positive about the outlook for TSMC, a leading-edge global foundry for many international semiconductor companies such as Apple, Nvidia, AMD and Broadcom, says Akmal. “It is also a key foundry partner in enabling semiconductor companies to roll out their products, especially in the 5G era. We are positive on [the stock] in the long term as we enter into a 5G high speed period which requires more chips for data processing and connectivity,” he adds.

BIMB Investment’s Najmuddin says the fund house will continue to rely on its quantitative- and momentum-based investment strategies to sustain the performance of its funds. Through these strategies, investments will be rebalanced either on a daily or monthly basis.

“We see opportunities in the beneficiaries of the pandemic such as gloves, e-commerce and logistics. Additionally, we will also look at beneficiaries of the post-lockdown economic reopening, such as technology and consumer, as well as opportunities in oversold counters which still have strong fundamentals, such as utility and plantation,” says Najmuddin.

According to the BIMB i Growth’s July fund fact sheet, the top holdings of this Malaysian equities fund with an aggressive growth strategy were QL Resources Bhd, JHM Consolidation Bhd and Guan Chong Bhd. These counters were selected as they will benefit from the post-Covid-19 economic recovery, says Najmuddin.

Meanwhile, for BIMB i-Tactical fund, its top holdings were TNB, Fraser & Neave Holdings Bhd and Supermax. Najmuddin says the first two are strong “staple” holdings. Therefore, their share prices are expected to remain steady regardless of the economic situation and shareholders can expect a decent dividend.

“Supermax, on the other hand, benefits from the structural increase in demand for gloves as the Covid-19 pandemic raises hygiene awareness on a global scale. This is in spite of the vaccination story; we believe it might take a while before vaccines can be effectively rolled out to the masses. Whether these specific counters will outperform in the next six months is anybody’s guess, but at this moment, we are happy to have valid reasons to own these counters,” says Najmuddin. This fund with a growth strategy invests in global equities.

As for PMB, besides the recovery play, it will also look at the glove and technology sectors, which it believes still have the potential to provide good returns, says Isnami. “We will continue to monitor developments in the market, as well as listed companies to make changes in our portfolios, if necessary.

“We will actively rebalance our portfolio, taking into account the various factors in the market. We will also continue to adopt a relative strength approach for each sector and counter.”

De Alwis says Kenanga adopts a barbell strategy by taking positions in both defensive and growth sectors. For defensives, the fund house has holdings in the healthcare and glove sectors, with the latter being a beneficiary of the Covid-19 pandemic. He explains that strong global demand for medical gloves has led to strong order visibility and increasing average selling prices.

“Other defensive sectors we like are those which are less impacted by the economic slowdown and offer good dividends, such as utilities and selected real estate investment trusts. We are also overweight in sectors that still see growth.

“The technology sector will continue to benefit from the rollout of 5G, growth in smart sensors and adoption of artificial intelligence, Internet of Things and automation. Should the path to recovery become clearer, we will increase allocation to more cyclical sectors such as commodities and the consumer sector,” says De Alwis.

Despite signs of improving economic data, De Alwis expects the equity market to remain volatile. As the market grapples with the risk of surging Covid-19 infections, governments could be forced to reimpose restrictions on business activities. Nevertheless, he says, asset prices could remain buoyant as policymakers continue to support the economy with aggressive fiscal support and liquidity programmes.

“The healthcare sector currently forms about 20% of the FBM Shariah Index weighting, along with high weightings in the telecommunications and utilities sector. If a vaccine for Covid-19 is successfully developed and widely available in the next 12 months, this could lead to the underperformance of defensive sectors versus cyclical sectors.

“Hence, the performance of the shariah index will be determined by the path of the pandemic and it could underperform the conventional index should a strong recovery take hold in the global economy. Nonetheless, as mentioned before, we will strive to outperform by tactically adjusting our weighting according to the situation and through our bottom-up stock-picking strategy,” says De Alwis.

Great time to invest

Apart from their potential to outperform conventional funds, there are other reasons why investors should maintain or even increase their portfolio allocations in shariah-compliant funds. For instance, these investments are seen to be more defensive in nature.

“Due to the screening process, the nature of the underlying assets of shariah-compliant investments tend to be more defensive in nature. This is because the shariah screening process would take into account financial factors such as gearing levels. Thus, companies with high debt ratios would be excluded,” says Akmal.

“By excluding non-shariah businesses, it can also be said that shariah-compliant funds have a stronger focus in terms of sector allocation. This allows the fund manager to have a stronger grip on the portfolio’s allocation and a better on-the-ground feel of the remaining sectors.”

Investors can benefit from greater diversification in their portfolios to reap better risk-adjusted returns due to the low correlation with conventional asset classes. By creating a portfolio using an array of shariah-compliant funds spanning different strategies and asset classes such as equities and sukuk, investors can better manage risk and achieve optimal diversification, says Akmal.

“With valuations turning attractive, it may even be an opportune time now for investors to gradually build their exposure to shariah asset classes,” he adds.

PMB’s Isnami says more investors are choosing to focus on environmental, social and corporate governance (ESG) investing. As shariah funds can be considered an ESG-based investment, investors who are concerned about the ESG factor in their investments can consider shariah funds as an alternative.

BIMB Investment’s Najmuddin concurs. He adds that the fund house went into the shariah ESG investing space in 2015. To date, it manages more than RM1 billion in ESG AUM, with the Global Shariah ESG Equity fund and Global ESG Sukuk being the largest funds in Malaysia in their respective fund category.

“Shariah investing has many values in common with those of socially responsible investing (SRI), a feature that benefits those who subscribe to this investment philosophy. Due to the selection criteria for the underlying investments, Islamic unit trust funds appeal to investors seeking products that espouse ethical investing.

“SRI-based funds have gained significant traction in the more developed markets, such as the US, with an estimated total AUM of some US$3.07 trillion (RM12.84 trillion). The shariah-ESG funds, from our experience, are able to generate returns on a par with conventional funds or even better. For example, our BIMB-Arabesque i Global Dividend Fund 1 is benchmarked against MSCI ACWI, a conventional index. This will eventually change the general perception of the investing public that shariah funds always underperform conventional funds,” says Najmuddin.

On what can be done to further develop the shariah funds industry, Akmal points out that the biggest challenge for the industry lies within the Islamic financial ecosystem itself, which is very much in its nascent stage compared with the conventional side, which is more mature. From the supply side, the main challenge is the lack of availability of sukuk papers, as well as a limited stock universe to develop diverse thematic shariah funds, he adds.

“While it would be simpler to look into shariah-compliant products with traditional strategies, such as those that provide exposure to pure equities or sukuk, it would definitely be more challenging when these products involve structured instruments,” Akmal says.

However, he believes that on the demand side, the increasing convergence of shariah and ESG principles will help catalyse growth for the industry. The alignment of both principles can draw more attention to ESG or shariah investments, especially among the new generation of investors who are more conscious about wider issues in society and the environment. Akmal says this, in turn, can spark growth for the industry, as demand will grow with broader appeal.

From an exchange-traded funds (ETFs) perspective, there is a lack of innovative shariah-compliant product offerings in this space. For instance, Akmal says, the fund house launched its first ETF — the TradePlus Shariah Gold Tracker (GoldETF) — in 2017. Until today, the fund maintains its status as the first and only shariah-compliant commodity-backed ETF to be listed on Bursa Malaysia’s main market.

“Due to stricter guidelines, trading of the GoldETF units needs to be carried out in cash and on a spot basis. As such, we have come to learn that many brokerage houses have tightened the settings for the account holders, requiring their account holders to contact their broker before being able to trade. This can be a hindrance to investors due to the inconvenience,” says Akmal.

However, the recent mushrooming of digital platforms has eased the process for investors, he adds. Wahed, a shariah-compliant digital investment management platform, enables the public to build their investment portfolios using shariah-compliant ETFs. The recent launch of Wahed’s gold portfolio, which invests in the GoldETF, allows investors to gain exposure to gold via the platform for as little as RM100, and without the hassle of going through brokers, he explains.

“We believe that more innovative trading platforms and the development of a conducive investment ecosystem would be beneficial for the capital market and the investment community as a whole,” says Akmal.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.