This article first appeared in The Edge Malaysia Weekly on October 11, 2021 - October 17, 2021

Latest 51% bumiputera equity requirement adds to the uncertainty

COUNTRIES are increasingly investing heavily in logistical infrastructure to provide public services, beef up national defence and facilitate the flow of goods and services for the economy. The importance of logistics to a country’s economy cannot be overstated, which is why recent developments in Malaysia’s logistics sector are a concern to stakeholders.

“Logistics is like the lifeblood for trade in Asean. If you somehow make the arteries a bit more clogged, trade doesn’t flow so easily,” says Ruben Maximiano, senior competition expert at the Organisation for Economic Cooperation and Development (OECD) in a recent interview with The Edge.

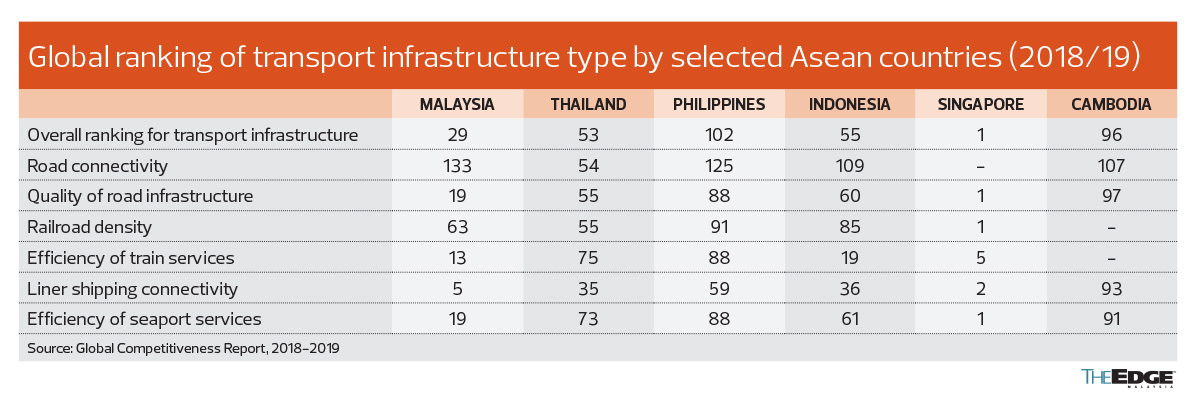

According to the World Bank’s Logistics Performance Index (LPI) 2018, Malaysia’s logistics performance dropped to No 41 in the world, even behind Vietnam in Southeast Asia.

How did we get here, and what needs to be done to ensure that the logistics industry is improved so that it can become more competitive and bring benefits to our economy?

“Our policy keeps changing. It is not that we don’t know how to change for the better, we do, but we backtrack. You cannot keep backtracking on your policy ... that is very wrong. You are sending the wrong message to investors and companies,” says a logistics operator who declined to be named.

To Maximiano, who led the OECD Competition Assessment Reviews on Malaysia’s logistics sector, the country’s slide down the LPI is due to other countries catching up and upgrading their regulations to bring them closer to international best practices.

“What we see is that from the infrastructure perspective, Malaysia is still quite strong within the region, and even the world, as it ranks significantly higher in this aspect than it does as a whole within the LPI context. So, there seems to be a lag here, or a difference between the quality of the infrastructure and the quality of the services provided on that logistics infrastructure,” he says.

He adds that it is time for Malaysia to get its logistics regulatory environment up to speed with international best practices, so that the length of time needed to deliver a service, as well as the cost, can go down. “That is what we’ve seen, that Malaysia has very high-quality infrastructure, but the services on that infrastructure could be better. We are making some proposals on how to improve those logistics services so that you can climb up the ranking once more and become the logistics hub that you aspire to.”

Where are we now?

The OECD report was derived from the mandate provided by the Asean Competition Action Plan 2016-2025 (ACAP).

In order to increase awareness of the benefits and role of competition in Southeast Asia, the ACAP provides for an assessment to be conducted on the impact of non-tariff barriers on competition in the markets of Asean member states and followed by recommendations.

According to the OECD report citing Mordor Intelligence, the transport and storage sector accounted for 3.8% of Malaysia’s GDP in 2019, with a gross value added (GVA) of RM57.2 billion.

The sector employed 667,600 people in 2019, representing about 4.4% of the employed population. The GVA of the land transport and water transport sub-sectors was RM14.5 billion and RM6.7 billion respectively.

The GVA of support activities for transport and postal/courier services stood at RM9.3 billion and RM2.7 billion respectively, according to Mordor Intelligence data cited by the OECD report.

Transport and storage services recorded a gross output value of RM120.7 billion in 2017 compared with RM109.2 billion in 2015, with an annual growth rate of 5.1%. Looking at these numbers, it is clear that the logistics industry is one of the most important in Malaysia. In fact, without an efficient logistics industry, other sectors may suffer from high cost and inefficiencies.

The Malaysian government and the private sector have invested billions of ringgit in the effort to improve logistical infrastructure — highways, ports, airports and railway lines — in the country.

However, the country’s logistics performance has been sliding on the LPI, according to the World Bank. The 2018 ranking of No 41 out of 160 countries was a big drop from No 25 and No 32 in 2014 and 2016 respectively.

Prior to the 2018 edition of the World Bank’s LPI, the performance of Malaysia’s logistics sector was the second best among Asean member states after Singapore. However, with an overall LPI score of 3.22 in 2018, Malaysia is now behind Thailand and Vietnam while Indonesia (No 46) is fast catching up.

Where did we go wrong?

According to the LPI, efficiency of the clearance process is the most challenging area in Malaysia’s logistics industry. However, in addition to scoring relatively high in infrastructure, the country also scored relatively well in international shipments.

Malaysia’s slide in the world ranking of logistics performance has a lot to do with its regulatory environment, rather than its infrastructure, says Maximiano. While the country has spent a lot on infrastructure, its regulations have not kept up with the rest of the world.

“In a competitive environment, many countries in the region have actually been doing some very good work in this field. And so, it is not that Malaysia is uncompetitive or hasn’t been doing a good job traditionally, it is just a matter of keeping up to date,” he adds.

“If you want to continue to be the important hub that you’ve been and keep attracting investments in the future, you will need to upgrade your regulations to international best practices. Otherwise, you will slip behind.”

Recently, there has been much debate on social media over the directive by the Royal Malaysian Customs Department requiring integrated international logistics services (IILS) companies to have 51% bumiputera equity by the end of the year.

The issue is not new to IILS players as this has been a longstanding requirement in the industry. However, back in September 2016, the Ministry of Finance (MoF) gave an exemption to local IILS licence holders and freight forwarders that had secured their licences prior to 1976 from the requirement, until Dec 31, 2020.

Then in 2018, according to a letter sent by the Federation of Malaysian Freight Forwarders (FMFF) to the Ministry of International Trade and Industry (Miti) dated Sept 18, 2021, the MoF said local IILS players do not have to meet the bumiputera equity requirements when renewing their licences.

In the letter, the bumiputera equity requirements for the freight forwarders and IILS licence holders were as follows:

1. Customs licences registered before 1976 — no bumiputera equity required

2. Customs licences registered after 1976 and before 1990 — 30% bumiputera equity required

3. Customs licences registered after 1990 — 51% bumiputera equity required

4. IILS Customs licences registered — no bumiputera equity required

On Dec 22, 2020, the MoF provided an extension until Dec 31, 2021, for the local IILS players that are not listed on any bourse to fulfil the bumiputera equity requirement.

Then in January this year, the MoF issued a letter stating that all Customs licences must comply with the bumiputera equity requirement, but no percentage of bumiputera equity was specified. All IILS companies have to comply but majority foreign-owned and public-listed ones were exempted.

This caused confusion among the IILS players and FMFF wrote to the MoF asking for a clarification on the bumiputera equity requirement. According to FMFF, the MoF responded by saying it would engage with other government agencies before coming to a decision on that matter.

As the deadline for the IILS players to fulfil the bumiputera equity requirement draws near, and the letter written by FMFF to Miti was leaked to the public, an uproar ensued among the public and certain politicians as it was seen as unfair for a non-bumiputera company to have to sell a majority of its equity to bumiputera investors.

As the requirement was supposed to be enforced by the end of this year, IILS players that do not meet the bumiputera equity requirement are concerned that they may lose their licences. According to some estimates, IILS licence holders could lose between 20% and 30% of their business if they lose their IILS licence.

According to FMFF president Alvin Chua, there are 218 IILS licence holders, with only 26 companies being wholly owned by bumiputera investors. There are 48 foreign-owned IILS licence holders.

“It is hard for IILS players to meet the 51% bumiputera equity requirement. There may not be enough bumiputera investors who are able to acquire the stakes at fair value. Over the years, many of these IILS players have built up their businesses and now, they are being told to sell the majority of their equity to someone else,” he tells The Edge.

“The government should come up with a solution. Who is going to take up the equity?”

Meanwhile, member of parliament for Bangi and assistant political education director for the Democratic Action Party (DAP) Dr Ong Kian Ming said in a Sept 25 statement that the relevant stakeholders need to sit down and explain the details of these issues and find long-term solutions to the challenges.

“The decision by the Ministry of Finance to postpone the enforcement of this equity rule to 2022 does not solve any of the problems highlighted in the long run. It merely kicks the can down the road,” he said.

“What is sorely needed is for the relevant stakeholders, including Miti (and the Malaysian Investment Development Authority), Ministry of Transport, the port operators, the logistics operators, business chambers (both local and foreign), financial institutions and politicians from both sides of the aisle to sit down and have a proper dialogue and discussion.”

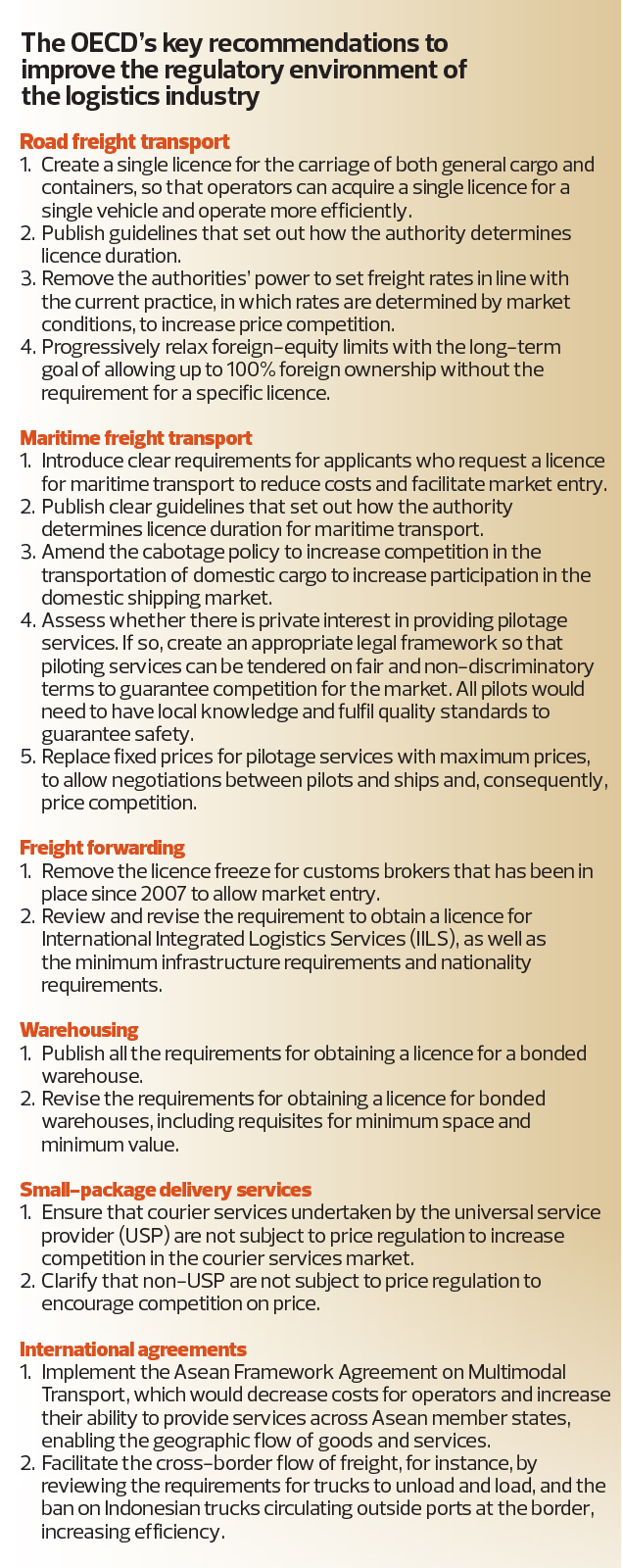

This is an example of restrictive regulations that have kept Malaysia’s logistics industry from improving. The OECD team that conducted the assessment on the logistics industry found 76 regulatory restrictions in Malaysia and made 63 recommendations. For example, in road freight transport, there are minimum capital requirements to enter the goods vehicle sector.

According to the Land Public Transport Agency’s (APAD) guidelines, an operator applying for a carrier Licence A must have accumulated capital of 30% of the cost of the vehicle to be purchased. For individuals and partnerships, private limited companies, limited companies and cooperatives, the paid-up capital must be not less than RM250,000.

In order to be granted a container licence, the paid-up capital must be not less than RM500,000 and the accumulated capital must be equivalent to 30% of the value of the vehicle to be purchased.

The OECD opines that this provision may increase the entry cost of new companies and may discourage investment and market entry, reducing the number of operators in the market. Notably, it may restrict the entry of small and medium enterprises (SMEs) and may have a discriminatory effect in favour of larger operators, and have a direct impact on choice and product quality for consumers.

As for the bumiputera equity requirement in IILS, industry players are saying that it seems that the government is signalling that it is allowing Malaysian entrepreneurs to exit the country, set up their headquarters in a foreign country and acquire the local companies with the IILS licence in order to keep their businesses. That is because foreign-owned IILS players are exempted from meeting any bumiputera equity requirements.

The industry players also say the enforcement of the bumiputera equity requirement would cause existing players to remain small operators and not venture outside the country to provide logistics services.

Meanwhile, the OECD says in the market competition assessment report that the restrictions on foreign equity participation in trucks for hire prevent or make it more difficult for foreign companies to enter the market, and hence reduce competition.

Trucks for hire are required to have 51% Malaysian equity, including 30% bumiputera equity participation. An additional restriction on these foreign equity limitations is that APAD’s licensing committee has discretionary power to approve the amount of foreign equity.

Foreign equity restrictions do not exist for other freight transport licences, such as those for courier service providers and commercial vehicles carrying their own cargo, for which up to 100% foreign equity is allowed, even if it remains at the discretion of the licensing board.

The OECD opines that the board’s discretionary powers lead to uncertainty and discourage market entry.

In other Asean countries such as Myanmar and Thailand, approvals must be sought for new foreign direct investment (FDI) acquisitions of more than US$100 million, or if the amount is greater than 50% of the total equity. In Cambodia, there are no FDI restrictions in the road freight transport sector, while in Indonesia and Laos, foreign equity is limited to 49%.

In Australia, freight transport operators can be 100% owned by foreigners. Freight transport is defined as a “sensitive business”, however, which permits the government to review foreign investment proposals against the national interest on a case-by-case basis. Foreign persons must receive approval before acquiring a substantial interest (20% or more) in an Australian entity valued above A$261 million.

While there could be justifications for these equity requirements and policy restrictions, the world is becoming even more borderless with the proliferation of the internet and competition between countries becoming stiffer. As can be seen in the World Bank’s LPI report, countries that were once leaders in the logistics industry could slip behind others that have been responding faster to the changing global economic environment.

“Facing a competitive international environment, other countries are upgrading their infrastructure and regulations. They are learning from others. We have seen that already during the three years that we have been doing this project, some countries have already started implementing our recommendations,” says Maximiano.

“Indonesia has already started implementing some of our recommendations, and they are not the only ones. So, it is a bit like you are running the race and you are running quite fast, and then suddenly someone runs faster. You would need to put in more effort to run a bit faster as well.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.