This article first appeared in The Edge Malaysia Weekly on August 3, 2020 - August 9, 2020

LATE last month, FGV Holdings Bhd’s special shareholder, Minister of Finance Inc, extended the contract of the plantation giant’s chairman, Datuk Azhar Abdul Hamid. Azhar will be the government-appointed director and chairman of the FGV board effective Sept 8.

In the run-up to his contract extension, names had been bandied about to take over the chairmanship, among them, Datuk Seri Shahidan Kassim, an Umno chieftain who is Member of Parliament for Arau (Perlis).

Azhar’s credentials as a plantation man are well known. He spent many years at Pernas International Holdings Bhd, Sime Darby Bhd and Tan Sri Syed Mokhtar Albukhary’s Tradewinds Bhd, which Pernas International had morphed into.

Azhar’s extension could stem from the government realising just how challenging things are at FGV, which has been suffering from financial woes for years.

Another view is that the government is satisfied with the performance of Azhar and other members of the FGV management team.

A possible privatisation

As talk of a snap poll looms, murmurs of a possible privatisation of FGV by its 33.66% parent, the Federal Land Development Authority (FELDA), have resurfaced.

Privatisation is seen as a means for the current government to gain the support of FELDA settlers, who make up the majority of voters in as many as 54 constituencies.

In an email response to questions from The Edge on the possible privatisation of FGV, FELDA replies, “As you are aware, a special task force on FELDA was recently set up, chaired by Tan Sri Abdul Wahid Omar. The setting up of this task force was to study the best possible ways to consolidate FELDA’s finances and sustainability for the benefit of its settlers, which includes exploring various options and avenues to resolve its financial challenges.

“As regards the question on the privatisation of FGV, we are not in a position to comment on the matter at this moment. In the event that any recommendation is made by the task force, it will report its findings and proposals to the government for approval,” it added.

The establishment of the task force in July this year was to help FELDA overcome its weaknesses, which were revealed in the White Paper tabled in Parliament in April last year.

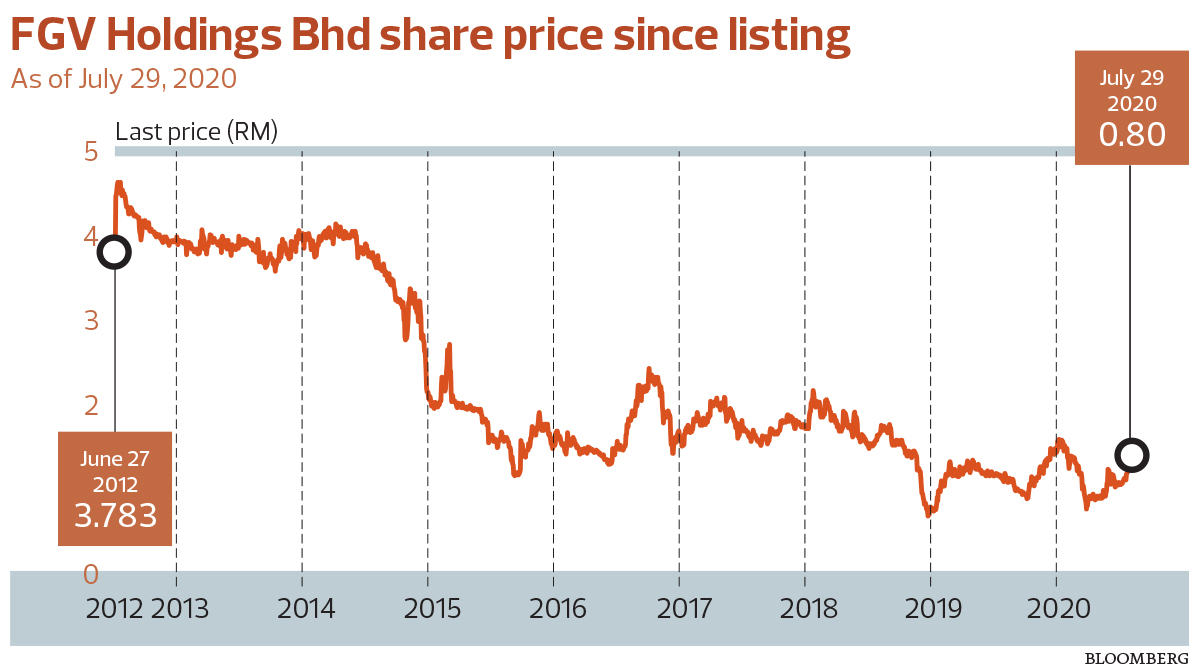

At its close of RM1.27 last Tuesday, FGV’s market value stood at RM4.63 billion. FELDA holds a 33.66% stake in FGV. At RM4.63 billion, the remaining 66.34% equity interest is worth RM3.07 billion.

If the government were to take it private, it is likely to pay a hefty premium to woo the settlers. FGV’s shares were floated in 2012 at an offer price of RM4.55. FELDA pocketed RM5.99 billion from the sale of its shares while FGV raised RM4.9 billion in fresh capital from the listing of new shares. Its initial public offering was the second biggest globally, after Facebook.

When it share price hit its peak in 2012, FGV’s market cap was slightly below RM17 billion.

Turning FGV around

Datuk Haris Fadzilah Hassan has been the CEO of FGV for 18 months. The perception was that he was facing an uphill task as the plantation group was financially stressed, with a dwindling cash pile and ballooning losses.

Haris, who has a three-year contract, tells The Edge he believes the management has done well in terms of resolving the fundamental issues.

“I think in terms of focusing on the basics, we have been doing well.

“All of the plantation numbers are improving. Things that we can’t control still persist. Whatever problems FGV faced before, we are still facing, for instance, LLA (land lease agreement, read FGV will survive even if FELDA ends LLA prematurely) and age profile, the (corporate) culture.

“The culture part is still the main part — it is something that takes a longer time to change, but I am still here working on it,” Haris says.

He divides the restructuring work into three areas, and frankly states that not all are within the management’s control.

“So, divide it in terms of two areas, areas that we can control, which is the operational numbers, [for] which I think we have done a serious transformation, and two is the culture, which is still a work in progress ... and three is to have new sources of revenue, which is what we are doing,” he says.

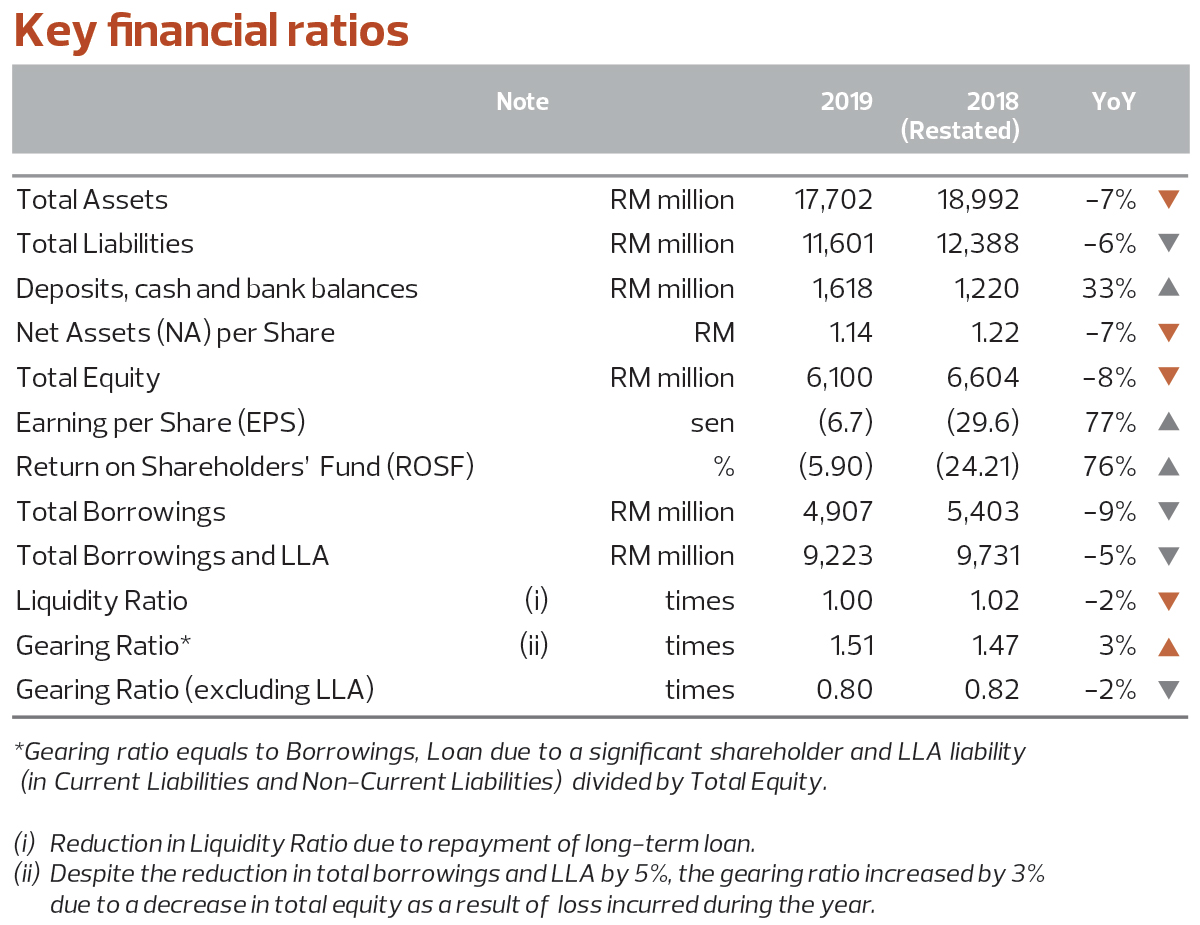

For the first quarter ended March 31, 2020 (1QFY2020), FGV’s net loss swelled to RM142.35 million from RM3.37 million a year ago. Quarterly revenue shrunk to RM2.78 billion from RM3.28 billion. However, the saving grace is that its operating cash flow improved to RM218.27 million in 1QFY2020 compared with RM19.71 million a year ago.

“We have stopped the bleeding, now, we want to sustain that performance and grow selectively.

“All things are on track as far as I see it ... The board is also happy, they have to say if they are not happy. I’m appointed by the board, not by the government, which is a major change in terms of the governance of FGV,” he says.

As at end-March, FGV’s cash pile stood at RM1.38 billion. However, it had short-term debt of RM3.02 billion and long-term borrowings of RM749.29 million. Finance costs in 1QFY2020 came to RM48.16 million.

Haris does not think the multi-billion short-term debts pose any major concern. “Not really ... we are still okay with that.”

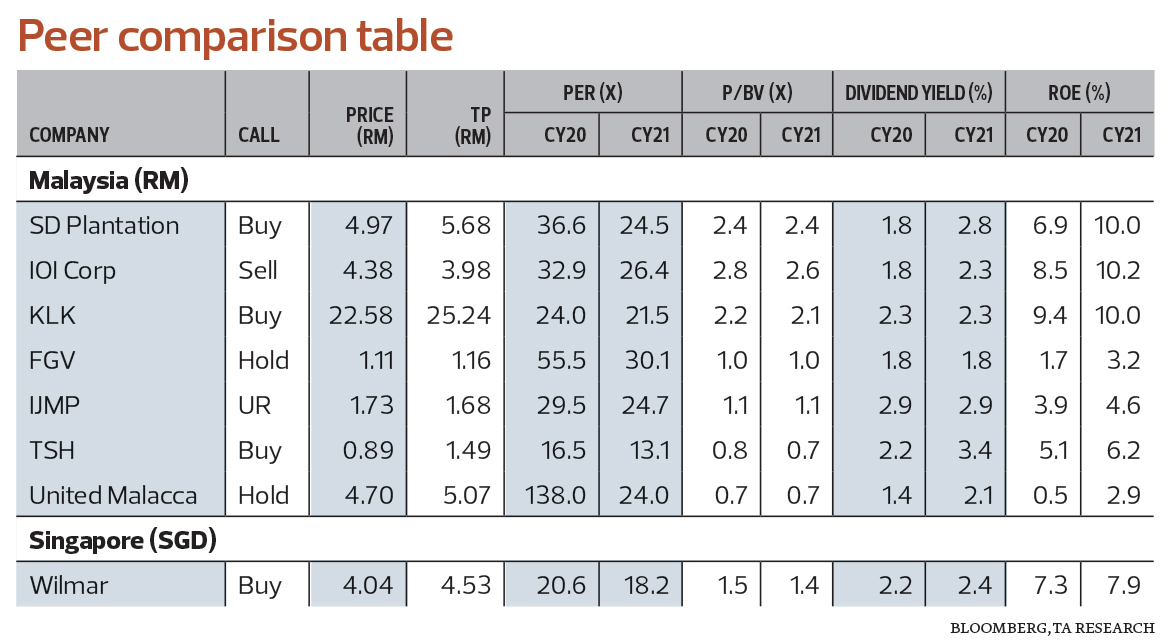

TA Securities plantation analyst Angeline Chin is among the handful who have a positive take on FGV. She has a “hold” recommendation on the stock.

“We now expect FGV to record a lower profit before tax of RM72.9 million and RM134.5 million for FY2020 and FY2021 respectively after factoring in weak 1QFY2020 results, lower FFB (fresh fruit bunch) production and lower margins,” says Chin, who pegs her target price at RM1.16 (see table).

Ivy Ng, head of Malaysia research and regional head of agribusiness research at CIMB Investment Bank, meanwhile, has a “reduce” call on FGV, with a target price of 98 sen based on a 10% discount to FGV’s sum of parts valuation.

In her first-quarter result review, Ng wrote that FGV has been loss-making for the ninth consecutive quarter. “The wider losses, despite efforts to turn around the group, reflect the vulnerability of the group’s current business model to low commodity prices due to its high costs of production.”

Land lease a heavy cost burden

Peer comparisons show that FGV did not fare as well as others like Kuala Lumpur Kepong Bhd, IOI Corp Bhd and Sime Darby Plantations Bhd, all of which were profitable in 1QFY2020.

Haris argues that such comparisons are unfair, largely because of the annual LLA payments of RM248 million.

“The business model itself is different if you want to compare against Sime Darby Plantation or IOI because they own the land. Ours is a lease, so we have to fulfil that lease portion (payment) first, and that itself has a disadvantage,” he explains.

Apart from the RM248 million annual payment to parent FELDA, FGV also has to fork out 15% of its profits to FELDA as part of its LLA.

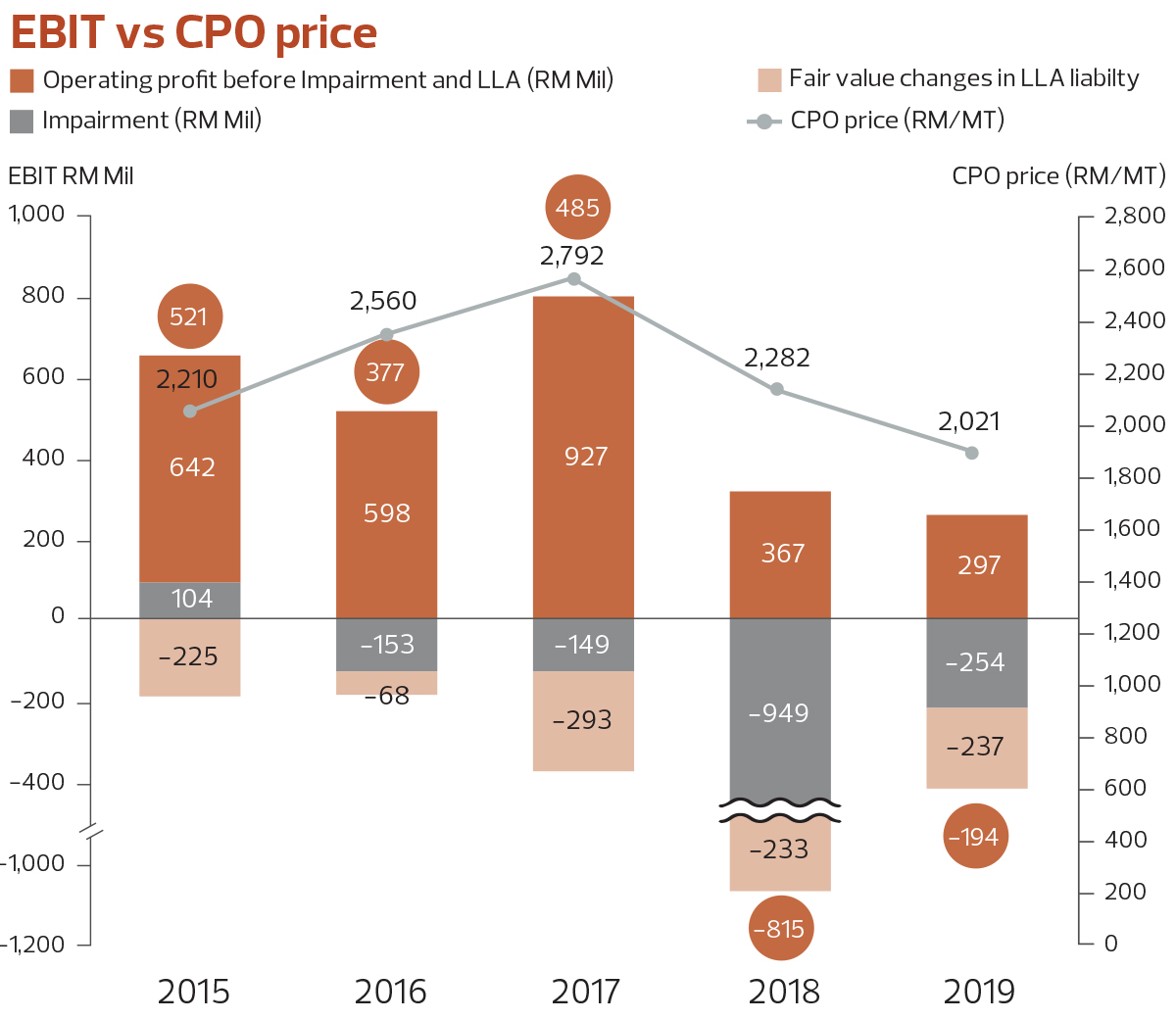

According to Haris, back-of-the-envelope calculations show that FGV has to add RM300 per tonne of CPO produced as a result of the RM248 million LLA payment, which makes it difficult to match its peers’ performance.

“Our previous CPO costs, ex-mill, is RM1,800, so [after] you add [the RM300], it’s RM2,100, so we need prices to be at least around RM2,100.

“What we have done over the past 1½ years is to bring down our costs through efforts on the field. We have brought it down to RM1,500 per metric tonne ... RM1,500 per metric tonne plus RM300 is RM1,800, so we have some headroom there. This really helps in terms of improving the profit of FGV,” says Haris.

Also hanging like an albatross around FGV’s neck is the age profile of its trees. FGV’s prospectus in 2012 indicated that 36% of its plantations were between 21 and 25 years and 16.9% was over 25 years. To put it another way, 52.9% of FGV’s plantations were regarded as old eight years ago.

Today, however, old trees account for one third, or 32%, of its plantations. This has been achieved through a replanting exercise covering 15,000ha a year. This costs about RM300 million a year, or RM2.4 billion in total since 2012.

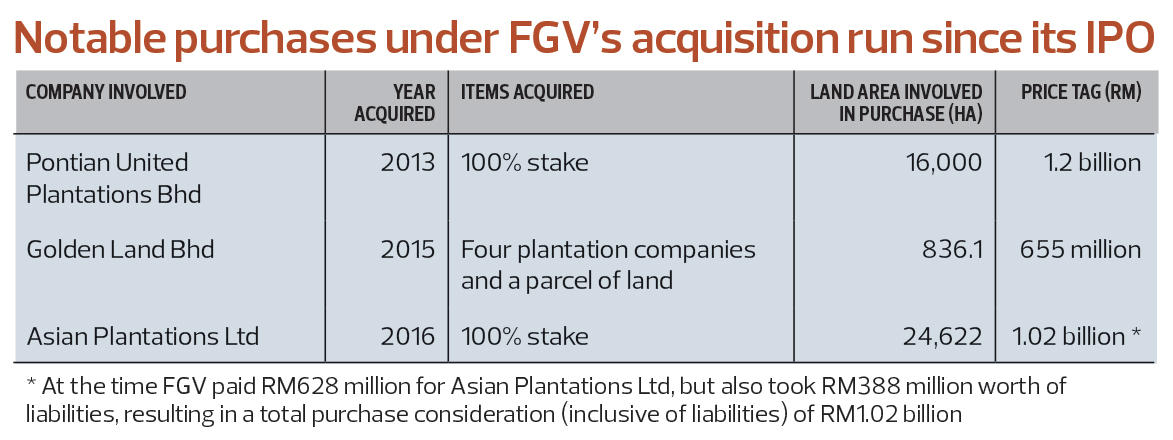

With a war chest of RM4.9 billion after its IPO, FGV was on the acquisition trail to expand its plantations with younger trees.

The acquisitions — including that of Sabah-based Pontian United Plantations Bhd for RM1.2 billion, and Asian Plantations Ltd for RM628 million cash plus assumption of RM388 million liabilities — were supposed to help reduce the age profile of FGV’s trees. Unfortunately, the goal was not achieved even after the coffers were nearly empty (see table).

“This is why in 2018, we had to take close to RM1 billion in impairments of investments that were made between 2012 and 2014. These are some of the reasons why we have it much harder compared with other plantation companies,” says Haris.

FGV owns good assets too

According to its FY2019 annual report, FGV is top of the class in many areas. For instance, it is the largest palm oil mill operator in Malaysia with 68 mills.

In 2019, FGV’s CPO output rose to 3.07 million tonnes annually, from 2.82 million tonnes previously, making it the largest CPO producer in Malaysia. In the downstream business, FGV’s Saji is the top refined cooking oil brand with a 34% market share, while its Seri Pelangi brand is the No 1 selling margarine with a 40% market share.

For seedlings, FGV’s Yangambi germinated seed is the biggest seller in Malaysia, with a 44% market share.

In edible oil storage, FGV has 844,400 metric tonnes of capacity — the largest in Malaysia and second largest in the world. FGV also has the largest compounded fertiliser production, with a capacity of 730,000 metric tonnes per year.

The largest selling refined sugar brand in the country, Gula Prai, with a 61% market share, is produced by FGV’s 51%-owned subsidiary, MSM Malaysia Holdings Bhd.

According to its FY2019 annual report, FFB production rose by 5.6% to 4.45 million metric tonnes, compared with 4.21 million metric tonnes in FY2018. FGV’s FFB yield in FY2019 was 18.44 metric tonnes per ha, while OER (oil extraction rate) was higher at 20.61%.

FGV’s average palm tree age profile was 13.8 years in 2019, compared with 16.25 years in 2012, according to its annual reports. Such improvements, perhaps, will be a great help in addressing the root cause of FGV’s issues as younger and more productive trees will generate better earnings and cash flow.

“Within one company we have so many things going for us, yet we are not able to capitalise on it,” Haris says.

With 1½ years of his planned three-year stint over, can Haris do the necessary to turn FGV around?

Read also:

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.