This article first appeared in The Edge Malaysia Weekly on September 19, 2022 - September 25, 2022

IN early August, the Energy Commission (EC) extended the solar power purchase agreements (PPAs) for the Large Scale Solar Mentari (LSS4) projects to 25 years, from 21 years previously, as soaring solar panel prices threaten the viability of the projects.

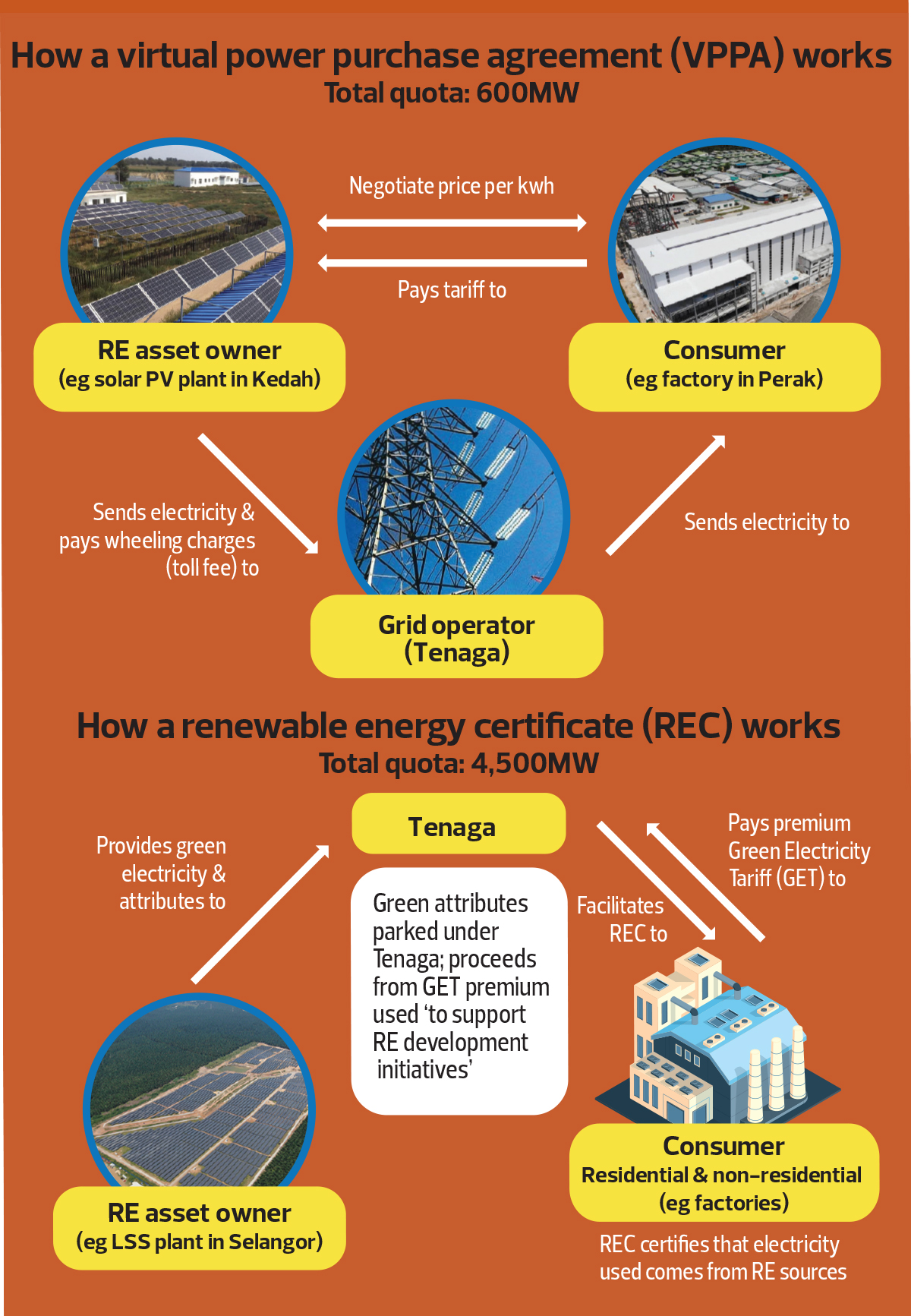

Later in the month, Prime Minister Datuk Seri Ismail Sabri Yaakob introduced a quota of 600mw to cater to those seeking to generate and sell solar energy directly to corporations. The government was also mulling a “solar park” project — similar to the one in Australia — to centralise solar assets in an area with high solar irradiance. This would allow a better sharing of the grid and related infrastructure to improve efficiency.

All this is welcome news to the industry. However, many details have yet to be ironed out in ensuring a smooth progression of Malaysia’s solar industry. This ranges from future project bids to industry policies, as well as steps to address the low take-up rate of the rooftop solar quota among residential consumers and government agencies.

Avoiding future LSS hiccups

One reason LSS4 projects potentially face negative returns amid rising solar panel prices is because of the overly competitive bids, in anticipation of a further decline in solar panel prices. The four-year PPA extension is a life saver as developers would have more time to recoup their investments.

However, despite the extension, the internal rate of return (IRR) is still lower than previously projected, some industry players say. Further, the outlook for some projects remains uncertain. Channel checks show that a number of equity owners have dropped out of the projects. Some have proposed that projects due in 2023 be pushed to 2024 following the delays.

At the time of writing, the EC had not replied to queries from The Edge.

Meanwhile, Samaiden Group Bhd group managing director Chow Pui Hee says underperforming developers or those with no project progress “should withdraw or surrender the quota to be re-tendered”. “Our view is that price competition is not always the most effective strategy that we would like to follow.

“Instead of rewarding the lowest bid submission, the eventual award should refer to multiple aspects such as financial strength, reasonability of project cost assumptions, proposal on the risk mitigation, readiness of the project to take off, land matters and so on.”

Solarvest Holdings Bhd co-founder and managing director Lim Chin Siu opines that the “request for proposal (RFP) for LSS4 itself is actually well structured”. “The criteria stated are very stringent ... Under normal circumstances, it would have been fine,” he says.

“The input price increase was unexpected as it was caused by a combination of multiple factors. We would like to thank the EC for the huge favour to the industry with the extension of the PPAs to 25 years.”

For future bids, Cypark Resources Bhd co-founder and group CEO Datuk Ahmad Daud proposes a mechanism to address fluctuations in the price of key equipment and materials, based on a constructed formula that can be reviewed against established indices such as copper and solar module prices.

Any savings or increases can be imposed through “a fixed tariff adjuster for a given construction period” affected by the fluctuation, he says. “Such an adjustment is nothing new in our power industry. The protection to the fossil fuel players [through the fuel cost pass-through mechanism] has been allowed for the entire 20-plus years of operation. What RE (renewable energy) industry players are asking for is much less — allow a pass-through mechanism for a short period of two to three years [only during the construction period].”

Uzma Bhd, in response to queries from The Edge, agrees to the adjustment of the offer price, but concedes that “this will take more time and add complexity” to the bidding process.

Still, discussions are needed to ensure that the “determination of reference price in LSS bidding is more encompassing” so that bidders can be “more realistic without being pressured to be the lowest”, says Uzma’s new energy division CEO Dr Ahmad Khalid Md Khairi.

Further, financing initiatives such as the Green Investment Tax Allowance (GITA) and the Green Technology Financing Scheme (GTFS) should continue with “more simplified requirements and approval process”, he adds.

Policy frameworks needed fast

Prior to the 50mw cap on LSS4 projects, Peninsular Malaysia had five LSS3 awards between 90.88mwac and 100mwac in 2019, of which three have been completed.

Beyond the LSS awards, the 600mw virtual PPA mechanism will open the door for any solar asset developer to build utility-scale plants (more than 50mw) — as long as it can secure a third-party off-taker.

Such corporate PPAs were previously limited to rooftop solar, an example being the 12mw peak (mwp) grid-connected solar asset atop Proton Holdings Bhd’s facility in Perak. That asset is owned by MFP Solar Sdn Bhd, but the solar energy is sold to Proton.

“We have experienced EPCC (engineering, procurement, construction and commissioning) players in the country with the know-how to implement projects of 100mw capacity and above. On top of that, the financing facilities are available to fund these developments. Perhaps one area to improve is grid connectivity,” says Solarvest’s Lim.

There is a lot of interest, particularly in the south of the peninsula. YTL Power International Bhd’s ambitious 500mw data centre park in Kulai, Johor, will see up to 72mw capacity in its first phase to accommodate anchor tenant Sea Ltd.

Last year, Johor mulled a separate 450mw solar plant that would cost an estimated RM1.4 billion, but called off the ground-breaking ceremony at the last minute, pending federal approval.

Companies were also toying with the idea of establishing solar plants in the state to potentially export to RE-hungry Singapore, but that is currently off the table as the government has banned RE exports (see sidebar: “The race to sell green energy at home and abroad”). Some are venturing overseas to capture bigger projects.

The Malaysian Photovoltaic Industry Association (MPIA) says new models such as virtual PPAs or third-party access (TPA) of the national grid are “good opportunities to accelerate the energy transition”. “These will bring us towards a more liberalised market,” MPIA president Davis Chong Chun Shiong says in an emailed reply to The Edge.

“Moving forward, the government could look at other measures to improve the internal rate of return of utility-scale projects [such as] subsidies for battery storage solutions. This will be a huge catalyst if successfully implemented, as it solves the intermittency issue.”

It is understood that a framework for the virtual PPA policy is still being ironed out. Similarly, a framework for Malaysia’s renewable energy certificate (REC) that was announced in November 2021 has yet to be finalised.

In a nutshell, a company may obtain certification stating that the electricity it consumes is acquired from RE sources by paying a premium for its electricity tariff (dubbed Green Electricity Tariff or GET).

Interestingly, Malaysia has the capacity to provide corporations with RE — companies committed to go 100% renewables under the Climate Group initiative RE100 last reported that 18% of energy they consumed in Malaysia last year was green energy, ahead of Vietnam (14%) and Thailand (13%).

Slow NEM quota take-up by homeowners, government

While RE may seem to be in vogue everywhere, the solar fever has not caught on with homeowners and government bodies.

The two segments received a quota of 100mwac each under the Net Energy Metering (NEM) 3.0 scheme, which offsets electricity tariff with rooftop solar-generated power on a one-for-one basis.

Currently, more property and solar developers are building solar-ready homes, which provide economies of scale and bring down the average cost. Nevertheless, the take-up rate remains low, with 50% and 72% of the quota remaining for homeowners and government bodies respectively (see chart). This compares with the 31% still available to non-domestic users, despite the much higher quota of 600mwac.Players point to challenges like a minimum capital outlay of about RM20,000 for homeowners and the fact that the NEM “credit” is only valid for one year, from two years previously. In addition, NEM participants cannot sell excess solar to the grid after the 10th year of installation — although some argue that battery storage systems may be widespread by then.

“Extending the NEM scheme beyond 2023/NEM contract beyond 10 years will give more value to customers. This is because the usage of electricity among domestic customers is higher at night, compared with during the day when solar is being generated,” Tenaga Nasional Bhd’s rooftop solar unit GSPARX Sdn Bhd tells The Edge.

To spur uptake, the government could grant individual tax exemption for solar installation costs, says Samaiden’s Chow. “Employers can consider providing a soft loan or financing scheme to their employees to encourage the adoption of RE as part of the ESG (environmental, social and governance) initiatives of the company,” she adds.

MPIA’s Chong opines that the existing NEM scheme should continue, while peer-to-peer energy trading could be introduced to provide more monetary benefits to prosumers. “The decentralised P2P platform can promote better operational efficiency in energy distribution and reduce peak demand and grid congestion.”

In any case, lessons should be learnt from Vietnam, whose inadequate policy and poor planning resulted in excess RE energy flooding the grid to the point where supply had to be capped. This prevented asset owners from monetising the electricity generation. Some have threatened to sue the government as a result.

The relatively young solar industry here is also witnessing the closure of a number of solar service providers amid stiff competition. This has resulted in customers being unable to claim warranty and having to fork out additional funds for maintenance from other providers.

Clear frameworks and careful planning will ensure an orderly generation capacity development and will be critical to put Malaysia ahead of its peers in the global race towards net zero carbon emissions.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.