This article first appeared in The Edge Malaysia Weekly on April 18, 2022 - April 24, 2022

SINCE the beginning of the year, Petroliam Nasional Bhd (Petronas) has been in the news for a variety of reasons. The cause for the fanfare includes Brent crude, the benchmark for oil prices, breaching US$120 per barrel in March, its highest level since mid-2014.

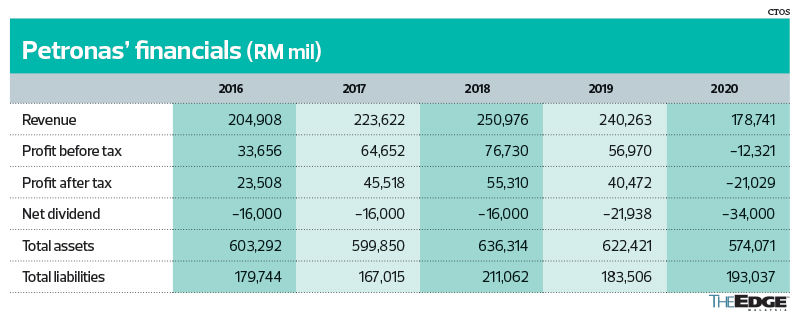

The high oil prices have resulted in a sterling financial performance for the national oil company, which chalked up a profit after tax of RM48.6 billion on the back of RM247.96 billion in revenue for the financial year ended Dec 31, 2021 (see table on FY2016 to FY2020 earnings).

This was followed by news of Petronas being linked to the bailout of ailing oil and gas (O&G) service provider Sapura Energy Bhd, which was subsequently denied.

While most of the news was positive, there were also allegations made by the Malaysian Oil & Gas Services Council (MOGSC) and Malaysia OSV Owners’ Association (MOSVA) that Petronas had been squeezing them to cut corners and, as a result, the national oil company generated huge profits at the expense of O&G players.

Both MOGSC and MOSVA wrote to Petronas in February, stating their grouses. The Edge, which was given a copy of their letters, ran a story on the issues raised by the two organisations last month.

In a recent interview over dinner at the Malaysian Petroleum Club, the company’s president and group CEO Datuk Tengku Muhammad Taufik Tengku Aziz said, “It’s unfortunate that MOGSC wrote to you [The Edge] and shared the letters because, typically, when you have a viewpoint, people will pitch opinions on either side, whether Petronas is brutal, tyrannical, making profits and squeezing everybody to die. But the other side of the story is that we’ve had RM1.5 billion worth of financing, where we work with banks to make it available to over 250 applicants. That dimension didn’t come through.

“First off, philosophy-wise, at Petronas’ board level, there is a very clear understanding. Petronas cannot perform, deliver, continue to exist without a robust and strong OGSE (oil and gas services and equipment) ecosystem.

“You don’t have to worry about us not recognising the fact or thinking, ‘Tak apa lah [It does not matter], whoever offers the service purely on cost competitiveness is what matters to us.’ I want to debunk that.”

Petronas met up with MOGSC officials last month to understand their grouses (see MOGSC’s statement).

MOGSC represents about 500 local O&G companies across the entire supply chain on the local OGSE spectrum. When The Edge met MOGSC officials, a question that was posed was whether they were shooting themselves in the foot by making their complaints public, considering that Petronas was responsible for dishing out contracts to the sector. One of the executives’ response was, “We are left with no choice … We are suffering.”

But how bad is the situation, and how much of their plight has been brought about by Petronas? And are the MOGSC members’ grouses valid?

While MOGSC was guarded in its response to questions from The Edge, some local O&G players say the picture being painted by Muhammad Taufik is a rosy one but the reality is quite different, and industry players are indeed suffering.

Cuts made under Coral 2.0

In early 2015, Petronas initiated a cost optimisation programme — Cost Reduction Alliance, better known as Coral 2.0 — to work with its petroleum arrangement contractors (PACs) and OGSE providers. In a nutshell, Coral 2.0 sought to reduce costs and improve efficiencies.

MOGSC says it played along and its members bit the bullet, as Brent crude traded in a volatile manner over the next few years, even falling below US$20 per barrel in April 2020.

On the cost-cutting exercise under Coral 2.0, Muhammad Taufik says, “Betul [Correct], in 2015, 2016, Coral 2.0 did ask for rate renegotiations. Because at that time, things were so dire that if we didn’t maintain liquidity, Petronas would have had to halt outright and they would have had no jobs at all.”

Now that oil prices have strengthened, MOGSC says Petronas should increase rates and contract values.

In an article on similar issues that was published in The Edge last month, the MOGSC executive committee said, “Ironically, the discounted price given by contractors during the oil price crash, with the intent to help the industry stay resilient, [has] now become a double-edged sword for them.”

MOGSC points out that oil prices have reached their highest level in seven years, but the rates of O&G service and equipment providers have not seen a similar rebound since Petronas made the request to lower rates as part of the Coral 2.0 initiative in 2015. They were looking forward to being compensated when oil prices recovered, but that has not been the case, it says.

To this, Muhammad Taufik says the contracts under Coral 2.0 have all lapsed. “We had Coral 2.0 in 2015. Practically all the contracts during that period lapsed in 2019. So, what we have now is predominantly priced against the market,” he explains.

To put things in perspective, oil prices shot above US$100 per barrel at end-February after Russia, the world’s third-largest oil producer, invaded Ukraine. Brent crude has averaged US$91.82 per barrel year to date, compared with US$51.09 in 2021.

Muhammad Taufik continues, “When oil prices go up, at some point, costs will also go up. But if you tie your rates directly to oil prices, what we lose out [on] would be competitiveness. Because in the region, we have to be competitive as well.

“So, if a contract [value] just escalates [and] de-escalates because of oil prices, where is that competitiveness that we’re trying to bring? We don’t want to have foreign direct investment not coming into Malaysia just because it’s expensive.

“So, I think it goes through — yes, recognising the cost, we also have to benchmark it [against] the region; typically, how much are the rig costs, vessel costs, and those two cannot lari banyak sangat [differ much]. If not, you don’t have a benchmark. Takkan lah [It cannot be that] your cost just goes up because all prices go up? It doesn’t make sense, right?”

Overdue Covid-19 claims

Another grouse that MOGSC has is the delays in Covid-19 compensation. It has been on the record to state that its survey of 30 member companies found direct and tangible Covid-19 costs of more than RM78 million, and indirect and intangible costs of more than RM134 million, but Petronas’ reimbursement was only 13% of direct costs, which has had an adverse impact on cash flows.

However, Mohammed Taufik says, “You’ve got to be fair to us. You submit a single-line indirect costs explanation. How am I going to tell [the other oil companies operating in Malaysia], ‘Ni Covid ni, bayar aje lah’ [Just pay the Covid claims]? … The other thing also is to understand, if you talk about project costs, that project payment is based on progress payment — you hit 80% completion, [then] 80% is paid. All that [has already been] paid.

“These Covid and other claims that are coming are over and above that. You can take all your invoices, related or not, [and] push it in, because this one is over and above the project progress cost. All that goes through a process of validating, and there are just two points: One, is it really for this project? And two, is it [of] a valid nature? — if it’s Covid and so on.

“So, what we’re also trying to do is, technically, let’s say someone claimed Covid expenses, [doing a] Covid test with the PCR [method]. What do you ask? I want to see receipts, names and amounts. It starts with that.”

Companies such as Sapura Energy had racked up as much as RM460 million in Covid costs as at last November. For its financial year ended Jan 31, 2022, the O&G player suffered a net loss of RM8.89 billion from RM4.13 billion in revenue. In the previous financial year, it saw a net loss of RM160.87 million on the back of RM5.35 billion in sales. Sapura Energy had racked up accumulated losses of RM13.52 billion as at end-January this year.

Many ailing O&G players

Other than Sapura Energy, which is 40%-controlled by state-owned Permodalan Nasional Bhd (PNB), the other casualties in the O&G sector include Perisai Petroleum Teknologi Bhd, which was delisted from Bursa Malaysia in January 2020 after failing to regularise its financial condition, and Barakah Offshore Petroleum Bhd, whose stock is still trading on the local bourse but which remains in the cash-strapped Practice Note 17 category. The company has been in PN17 status since May 2019.

Many of the smaller O&G companies that are having financial problems were subcontractors and vendors of Sapura Energy and Barakah Offshore, and have been left reeling as a result of non-payment by the two players.

Another previously high-flying O&G company that is in the doldrums is Serba Dinamik Holdings Bhd, which has been grappling with accounting issues and is now in the cash-strapped PN17 category. Its issues are not related to volatile oil prices, though.

Minister of Finance Inc unit Urusharta Jamaah Sdn Bhd has a 64.45% stake in fabricator TH Heavy Engineering Bhd, which has been in the PN17 category since early May 2017.

Malaysia Marine and Heavy Engineering Holdings Bhd has suffered four financial years of losses. It is a 66.5%-owned unit of shipping company MISC Bhd which, in turn, is a 51% subsidiary of Petronas.

Another O&G company in the PN17 category is Scomi Energy Services Bhd, which was once a politically connected outfit.

Much-needed consolidation

Muhammad Taufik’s predecessors had been beating the same old drum over the past decade or so, pushing for consolidation in the O&G industry. However, apart from the merger between SapuraCrest Petroleum Bhd and Kencana Petroleum Bhd in 2012 (which formed Sapura Energy) and Dayang Enterprise Holdings Bhd taking over a controlling stake at Perdana Petroleum Bhd, there have been no major consolidation exercises in the sector.

In 2017, Velesto Energy, in which PNB — both directly and via its units — has a shareholding of 54.16%, was slated to merge with another government-controlled entity, Icon Offshore Bhd, in which Yayasan Ekuiti Nasional has 56.1% equity interest. However, the deal fell through.

“Maybe I’ve been speaking Hokkien to a Latin-speaking group because I don’t think they are getting the hint [to consolidate]. Not only me, but my predecessors as well,” says.

“Everyone is waiting for the other person to blink first. Nobody wants to come forth and say, ‘I have x assets, you have similar; let’s get together.’ No one is making the first move. So, like I said, we can be encouraging and we can even tell you all the benefits of scale in doing that, but we can’t put you together. If something goes wrong, guess who gets blamed — the matchmaker [Petronas].”

To illustrate, MOSVA has 24 members, but about 80 companies own and operate vessels in Malaysia. Similarly, only a few companies have been given fabrication licences, but there are a number of small players as well.

“Petronas recognises the duty [to nudge consolidation], but it can only go so far. We can only do so much,” says Muhammad Taufik.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.