CHANGE is in the air for tobacco players that have traditionally matched each other when it comes to pricing cigarettes. Each cost increase or tax hike is usually followed by a rise in selling prices across the sector to defend profit margins.

But British American Tobacco (M) Bhd recently reversed a price hike — the second reversal in just over half a year — after its 50 sen per 20-pack raise was not matched by competitors.

“This could be a sign that BAT is losing its price leadership in Malaysia and I don’t discount a price war brewing,” an analyst with a local bank-backed research house tells The Edge.

“This time around, Philip Morris (M) Sdn Bhd and JT International Tobacco Sdn Bhd (JTI) did not follow BAT’s lead and it shows that they might be wanting to break the tradition of BAT being the price setter.”

BAT (fundamental: 1.35; valuation: 1.7) had raised the price per 20-pack by 50 sen following the implementation of the Goods and Services Tax on April 1 while Philip Morris had gone for a lower 40 sen mark-up per pack. Surprisingly, JTI maintained its selling price.

BAT (fundamental: 1.35; valuation: 1.7) had raised the price per 20-pack by 50 sen following the implementation of the Goods and Services Tax on April 1 while Philip Morris had gone for a lower 40 sen mark-up per pack. Surprisingly, JTI maintained its selling price.

BAT, the only listed company among the three, then cut the price per pack by 20 sen — 10 sen below Philip Morris’ price (see table).

Some corners cite the Malaysia Competition Commission’s greater scrutiny since January last year and fears of running afoul of the Competition Act 2010 for tobacco manufacturers bucking the price trend.

But most believe that it is simply a sign of competition heating up to capture a larger slice of the shrinking pie.

“Philip Morris might decrease prices in response and decide to absorb the cost of GST in the process,” the analyst says, adding that producers now seem open to taking a cut in profit margins in order to defend their market share.

The few sen difference will have an impact, especially in the value-for-money segment where consumers are more likely to switch brands because of price considerations, the analyst comments.

BAT learnt this lesson in September last year when it raised its selling price by RM1 per pack but was only matched by JTI.

“In September 2014, BAT’s sales volume fell 10% year on year as it lost market share due to the disparity between its selling prices and those of its competitors in the two weeks before it reversed its decision,” CIMB Research analyst Eing Kar Mei says in an April 13 note.

This time, if Philip Morris decides on a price reduction as a countermove, BAT may need to embark on another round of price cuts to maintain its market share, she adds.

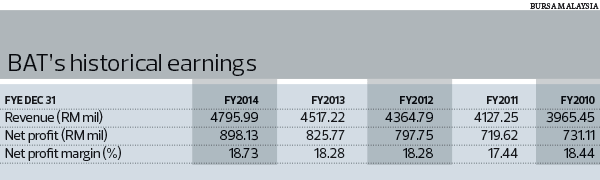

Eing, who has lowered BAT’s target price to RM58, recommends that investors reduce their exposure to the stock in view of regulatory and competition risks. BAT closed at RM68.28 last Thursday.

As of now, BAT is estimated to command 62% of the total legal market while JTI and Philip Morris have 22% and 16% respectively, according to data by AmResearch.

Analysts expect the pie to shrink, no thanks to the growing illicit trade as regulatory enforcement moves at a slow pace. In 2013, the contraband market made up 35.7% of the total industry.

“The legal market is shrinking. The pie is getting smaller and you cannot always push for higher prices,” says another analyst with a local research house.

“People like to think that the tobacco market is inelastic but there is a threshold. People might reduce their buying now that cigarettes are so expensive and incomes are not rising. They could stop smoking altogether or even turn to illicit cigarettes or e-cigarettes.”

The consensus expectation is for volume to continue to decline this year. “We maintain our forecast for industry volume to contract 10% this year mainly due to the steep excise duty-led price hikes of 12% to 14% imposed in November 2014,” UOB Kay Hian Research analyst Vincent Khoo says in an April 13 note.

The November price hike, however, should keep margins fairly insulated this year, says the analyst with the local bank-backed research house.

“In fact, we could see a slight expansion this year because of that price increase. But if volumes fall by 15% to 20%, producers might not be able to absorb the cost,” she says, adding though that this is unlikely.

“In any case, BAT seems to be in a more comfortable position to weather a margin compression than the other two because of its sizeable market share.”

At press time, The Edge had yet to receive comments from BAT, JTI or Philip Morris.

This article first appeared in The Edge Malaysia Weekly, on April 20 - 26, 2015.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.