This article first appeared in Capital, The Edge Malaysia Weekly on December 27, 2021 - January 2, 2022

SINCE the Covid-19 pandemic broke out in late 2019, the prices of most commodities have moved north, which was evident in 2021 with the Bloomberg Commodity Index (BCOM) — which tracks 23 energy, metals and agriculture futures contracts — hitting a 10-year high of 105.84 in October.

Compared with a year ago, and up to Dec 17, the index has surged 25%. ING head of commodities strategy Warren Patterson and senior commodities strategist Wenyu Yao say in a December note to investors that recovering demand following Covid-19, supply chain disruptions, government policy and adverse weather have all contributed to tightening in markets this year, which has propelled prices higher.

“Going into 2022, we expect the disruptions we have seen in supply chains to improve, while the balances for several commodities will look less tight than in 2021. This should mean that prices edge lower from current levels. But, importantly, we still expect them to remain above long-term averages.

“So overall, while we see some marginal downside risks across the commodities complex in 2022, on a historical basis, prices are likely to trade at elevated levels for another year. The key risk, of course, is the coronavirus pandemic. Overall, we’re keeping the faith,” they wrote.

While metals such as gold and iron ore had a stellar performance last year, their performance in 2021 was muted in comparison. However, it was a very good year for energy, with surging prices in crude oil and natural gas, as well as for agricommodities, with the prices of wheat and coffee trending upward. The prices of crude palm oil (CPO) — an agricommodity that is not part of the BCOM but one which is vital to Malaysian exports — also surged to new highs.

We take a look at the performance of crude oil and CPO in our accompanying stories. Here, we revisit the performance of some of the other commodities, and take a look at their outlook for the coming year.

Surging natural gas prices

Compared with a year ago, spot Asian LNG (liquefied natural gas) prices measured by the Japan-Korea marker (JKM) have more than tripled year on year to US$45 per metric million British thermal unit (MMBtu).

ING’s Patterson says spot Asian LNG has largely traded at a healthy premium to that of Europe, with natural gas prices in Europe surging on account of tight inventories, and therefore there has been a clear incentive to send cargoes into Asia.

“China’s LNG imports are up 23% year on year over the first 10 months of the year, and have overtaken Japan this year to be the world’s largest importer [of LNG]. Chinese demand has been supported by strong industrial demand along with growing demand from the power sector. China’s ambitions for [carbon] emissions to peak before 2030 should continue to prove supportive for LNG demand in the coming years,” he says.

Reuters reported in June that state-owned enterprise China National Petroleum Corp (CNPC) expects China to cut its coal use to 44% of energy consumption by 2030 and 8% by 2060 as the country aims to use more natural gas to achieve its climate change goals.

“Looking at the forward curve, the Asian market is at a premium to Europe all the way through 2022, with the premium being at its widest early next year. Therefore, do not expect the [Asian] LNG market to solve Europe’s tightness. The region will need to continue to compete against Asia for spot LNG through 2022,” says Patterson.

OCBC Bank economist Howie Lee says LNG prices have remained heavily elevated in Europe and Asia, with both the TTF (Title Transfer Facility) — a virtual trading point for natural gas in the Netherlands) and the JKM trading in excess of US$30/MMBtu as at December this year — more than double the price traded at the start of the year.

However, he expects LNG prices both in Europe and Asia to return to US$25 per MMBtu by the end of next year.

“While that represents a year-on-year decline, it remains substantially elevated by historical standards,” he says.

Muted performance from metals

Gold prices, which started out the year peaking at US$1,950 per ounce in January, have since retreated to as low as US$1,683.54 in March on the back of a strengthening US dollar. Compared with a year ago, gold prices have declined 4% to US$1,802.41 per ounce on Dec 17.

OCBC’s Lee expects gold to trend lower next year, at an average of US$1,500 per ounce.

“Most central banks have now listed taming inflationary pressures as one of their core priorities in 2022, which means the global interest rate environment is likely to tighten sharply on aggregate next year. The aggressive pace of rate hikes may outweigh demand for gold as an inflation hedge, resulting in a net bearish effect on gold,” he says.

Fitch Solutions, in its commodities outlook report, also sees gold prices averaging lower in 2022, as the greenback strengthens and bond yields continue to recover.

“We see prices averaging US$1,700 per ounce in 2022 with continued bouts of volatility, compared with our forecast of US$1,800 per ounce for 2021. Gold will remain supported in the near term as inflation runs at a multi-year high, which will maintain the appeal of gold. However, this will be balanced by rising risks of the US Federal Reserve raising interest rates at a faster and stronger pace than currently expected by market participants,” says Fitch.

Iron ore prices, which had a phenomenal run in 2020, saw a drastic decline this year. Prices had peaked in May at US$227 per tonne following the suspension of the China-Australia Strategic Economic Dialogue, which led to Chinese steel mills rushing to pile up supplies in the event of potential trade restrictions between the two countries.

However, iron ore’s fortunes quickly turned and prices headed south, hitting the lowest point this year at US$86 per tonne in November, on the back of dismal demand outlook for steel products and raw materials in China.

“Lower steel production has failed to lift steel mill margins in China, which had turned negative in the fourth quarter of 2021 due to weaker demand from the downstream property sector and slower activity from others owing to frequent power shortages.

“The China policy landscape at the macro level, including moves toward decarbonisation, remains a cap over the medium-term demand outlook for iron ore. As such, China’s steel production is unlikely to return to the levels seen in the first half of 2021,” says ING’s Yao.

ING expects iron ore prices, which were trading at US$118 per tonne on Dec 17, to trend lower in 2022, averaging US$100.

“On average, we expect prices to slide to US$100 per tonne over 2022, with the main upside risks still being potential supply chain disruptions in light of the Omicron variant,” says Yao.

Copper prices quoted on the London Metal Exchange on the other hand have increased 19% year on year (y-o-y) to US$9,437.5 per tonne.

OCBC’s Lee expects copper prices to peak further at an average of US$12,000 per tonne next year.

“Copper demand is expected to enter its second year of expansion, especially after the recently concluded COP26 (2021 United Nations Climate Change Conference) demonstrated an increasing willingness by governments to prioritise clean energy. Unresolved supply chain bottlenecks, which may persist until the second half of next year, are also expected to keep prices supported,” he says.

LME tin prices have surged a whopping 94% y-o-y to US$38,840 per tonne. Prices had earlier reached a record high of US$41,073 per tonne in November. Malaysia Smelting Corp Bhd, the world’s third largest producer of tin, attributed the record tin price to the current global landscape of promoting environmental and sustainability initiatives, photovoltaic installations, electric vehicles and growth in electronics, which bodes well for the demand for tin.

Fitch Ratings, which expects tin prices to ease slightly from spot levels to US$32,500 per tonne next year, says tin is anticipated to remain on a firm upward trend in the coming decade to reach US$35,500 by 2030 — nearly double its average price of US$18,729 per tonne from 2016 to 2020.

“We expect tin demand to continue outstripping supply, pushing the market into deficit by 2026. On the supply side, a thin pipeline of tin mining projects will tighten the tin concentrate market, leading to increased competition among smelters and constrained ore feed for refined output growth.

“On the demand side, the global use of tin will increase rapidly through the metal’s use in electronics (especially as electric vehicles increasingly contain greater amounts of electronics in their body) and solar panels (in photovoltaic cells), cementing tin’s status as a commodity of the future. Ultimately, this will allow the market to tighten and return to a production balance deficit by 2026, which will only grow deeper over the years,” says Fitch.

Agricommodities surge

Wheat prices have surged 25% y-o-y to US$7.72 per bushel on Dec 17, as a result of a series of droughts and heatwaves around wheat-producing regions.

“Export taxes were also introduced and later raised in Russia, a key exporter, at a time when importing countries were competing for available wheat,” says Rabobank in its Agri Commodity 2022 Outlook Report.

Rabobank expects wheat prices to trend higher in FY2022, at US$8.10 per bushel in the second quarter of 2022, before moderating to US$7.50 in the fourth quarter.

“Our base case for 2022/23 shows a small surplus in the global balance sheet after two years of deficits, but it will take more than half a year for this to materialise. Despite excellent prices, production is expected to increase only marginally, and it will be the drop in demand for feed wheat that will allow that surplus to emerge,” says Rabobank.

Coffee prices had a phenomenal run in 2021, with Arabica coffee prices increasing 85% y-o-y to US$2.35 per pound on Dec 17, due to logistical issues such as the shortage of containers that led to panic buying of the commodity.

“Panic buying is likely to be alleviated after Christmas, allowing prices to drop,” says Rabobank, which expects Arabica coffee prices to drop to US$2 per pound in the first quarter of 2022, before retreating to US$1.66 in the fourth quarter of next year.

ING’s Patterson expects Arabica coffee prices to average around US$1.95 per pound in 2022.

“Demand is expected to outstrip supply. This will be driven by a combination of further growth in demand, along with a Brazilian crop weighed down by frost and possibly drought. However, much will depend on precipitation in the coming months. There are some who are forecasting a deficit of as much as seven million bags. The expectation of a deficit [next year] and the uncertainty on how big this deficit could be suggest that prices should remain well supported,” he says.

Meanwhile, cocoa prices have increased by 6% year on year to US$2,547 per tonne on Dec 16 as a result of expected lower production. Rabobank expects cocoa production to decline in 2022 as a result of lower input and poor weather at the start of the season, and forecasts prices to trend slightly higher at US$2,580 per tonne in Q1 2022 before further increasing to US$2,710 per tonne in 4Q2022.

A record year for palm oil prices

By Supriya Surendran

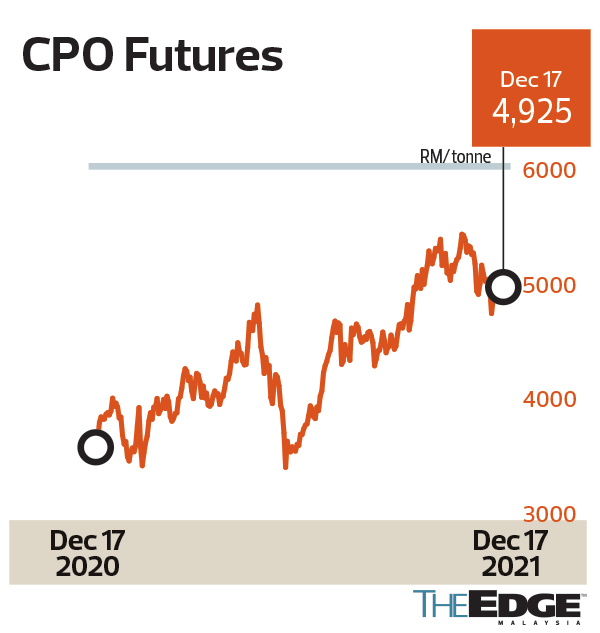

A record year for crude palm oil (CPO) prices — that’s one of the economic positives 2021 will be remembered for, with CPO futures surging to an all-time high of RM5,446 per tonne in November on the back of tight edible oil supplies. As at Dec 17, the price of CPO was RM4,925 per tonne, an increase of 37% from a year ago.

Rabobank in its agri commodity outlook report says palm oil prices will be supported by the expectation that global vegetable oil inventories will remain in deficit next year.

“The combination of a less-than-optimal palm oil production increase and minimal year-on-year biodiesel demand increase in 2022 in Southeast Asia will result in a slight surplus situation for palm oil globally in 2022,” it says.

Rabobank notes, however, that the y-o-y decrease in global soft oil inventories next year will be larger than the increase in palm oil inventories. It attributed this to “an expectation of increasing y-o-y global soy oil demand” amid rising demand from the renewable diesel industry and lower y-o-y global rapeseed oil production.

Rabobank expects CPO prices to trend lower at RM4,700 per tonne in the first quarter of 2022 (1Q2022) before further declining to RM4,300 per tonne in 4Q2022.

CGS-CIMB Research in a Dec 12 note to clients says CPO prices could remain high until 1Q2022 before trending lower when palm oil supply recovers and crushing activities of oilseeds improve.

“The strong CPO price and expectations of a gradual return of foreign workers are positive [points],” it explains, though also noting, “These are offset by concerns over rising fertiliser costs.”

CGS-CIMB expects CPO prices to trade at RM3,600 per tonne in 2022.

Dr Sathia Varqa, owner and co-founder of Palm Oil Analytics, a Singapore-based independent, online publisher of palm oil market news, thinks prices should start easing from March 2022 as production improves, “based on the assumption that there is no major weather disruption and workers are ready for harvesting [work] in May”.

Sathia expects the CPO futures active month contract to trend at RM4,200 to RM4,400 per tonne this month before trading higher in January and February next year.

“Prices are expected to lower again from the end of March 2022 onwards to RM3,900 to RM4,200 per tonne,” he tells The Edge.

OCBC economist Howie Lee sees palm oil trading at an average of RM4,750 per tonne next year, with production expected “to return in earnest next year in both Malaysia and Indonesia”.

Further, “our expectations of higher soy prices mean the palm complex is also expected to be lifted higher.”

Soybean oil, a more expensive alternative to palm oil, has seen a 50% increase in the price of its futures contract to US$0.54 per pound.

Rabobank says in the US, biodiesel demand growth has been overwhelming, with soybean oil being its primary feedstock.

“Strong biodiesel prices, Covid-19 convalescence and supply risks provide support for soy oil to remain [at] record highs in the year ahead,” it says.

Rabobank expects soybean oil to trade at levels of US$0.60 per pound in 1Q2022 before moderating to US$0.58 per pound in 4Q2022.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.