This article first appeared in Capital, The Edge Malaysia Weekly on July 5, 2021 - July 11, 2021

Utilities sector – overweight

Petronas Gas Bhd

Target price: RM17.70 ADD

Tenaga Nasional Bhd

Target price RM13.40 ADD

CGS-CIMB RESEARCH (JUNE 29): We view environment, social and governance (ESG) risks for the utilities industry as opportunities, given the rapid growth in renewable energy (RE), rising electricity demand [in future due to digitisation] and continuous investments in the grid [to facilitate energy transition].

Our analysis shows that RE capacity will grow strongly in 2021 to 2028 to comply with COP21 (2015 Paris Agreement), new thermal plant commitments to come in from 2029 and battery energy storage system (BESS) installation to start from 2030F to address the influx of RE. In Malaysia, RE is expected to account for 31% of the capacity mix by a significant increase from the regulator’s projected 17% in 2021. Conversely, coal-based power plants are expected to decline from 37% in 2021 to 22% in 2039.

Utility players are focusing on growing their RE capacity by investing in new RE projects domestically or internationally to diversify coal-based revenue, especially for power plant generators Tenaga and Malakoff. Tenaga has set an 8,300mw RE capacity target by 2025 (32% of capacity mix) to maintain its coal-based revenue at below 25%. We believe that the majority of the RE expansion will come from overseas, given that the domestic RE projects are capped at 30mw to 100mw historically. Malakoff (“add”, target price: RM1.04) secured some small-scale RE projects locally and the acquisition of Alam Flora completed in 2019 provided additional EPS accretion and synergistic opportunities to develop waste-to-energy projects. Cypark Resources (“hold”, target price: RM1) will continue to bid for RE projects and grow its portfolio in the future, according to management guidance.

We upgrade the sector to “overweight” (from “neutral”) on our expectations of EPS growth (CY21-CY22 versus CY20), undemanding valuations (CY21F sector average PER of 13.1 times versus 16.6 times in CY20), decent dividend yield of around 5%, limited foreign outflows as foreign shareholding is near historical lows and overplayed ESG concerns. Tenaga and Petronas Gas, which have better ESG disclosures versus their peers, are our top picks for the sector. Key downside risks are political instability and more power reform in the pipeline.

We believe Tenaga [which could have been penalised by investors for its coal-based revenue (20% in FY20)] could easily tackle its coal exposure by spinning off its non-regulated generation business in future. For investors with concerns about coal plant generation, Petronas Gas could stand out as a good candidate for ESG rotation play, given its better ESG rating versus its peers and comprehensive ESG disclosures. We like YTL Power (“add”, target price: 78 sen), given the potential earnings recovery and dividend yield remaining decent at over 5% for FY21-23F. We like Gas Malaysia (“add”, target price: RM2.97), given the relatively stable net profit and decent dividend (around 5% for FY21-FY23F) as potential rerating catalysts.

SCGM Bhd

Target price: RM3.02 OUTPERFORM

KENANGA INVESTMENT BANK (JUNE 29): FY21 (ended April) core net profit of RM34 million came in within (103%) our estimate of RM32.9 million while DPS of 7.1 sen was within 97% of our 7.3 sen estimate.

Moving forward, we view the 60% workforce limit as merely a hiccup, as we foresee SCGM ramping up utilisation after the lockdown is eased, given the robust F&B packaging and face mask orders, driven by renewed lockdowns and resurgent Covid-19 cases. We believe SCGM will focus on ramping up utilisation and eventually increasing capacity for its high-margin products in FY22.

We increase FY22 revenue and core net profit forecast to RM282.9 million and RM37.4 million respectively to account for a higher-margin product mix. We introduce FY23 core net profit of RM40.2 million. Based on a 40% dividend payout policy, our forecast DPS of 7.8 sen for FY22E and 8.4 sen for FY23E imply yields of 3.2% and 3.4% respectively. Reiterate “outperform” with a new target price of RM3.02 (from RM2.62) based on FY22 EPS of 19.5 sen, using a forward multiple of 15.5 times.

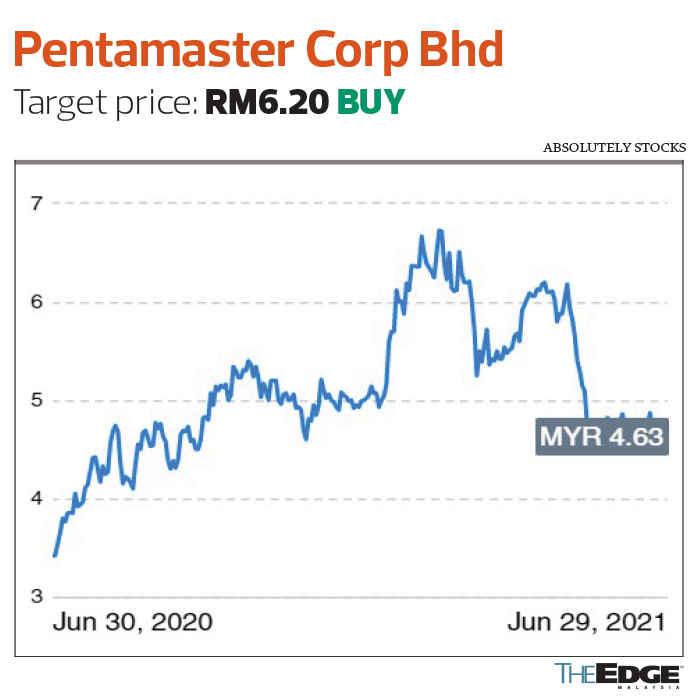

Pentamaster Corp Bhd

Target price: RM6.20 BUY

UOB KAY HIAN RESEARCH (JUNE 29): Pentamaster’s latest order book backlog stood at RM235 million, 18% higher than the normal range last year. Its 1Q21 revenue surged 15% despite being dragged by travel restrictions as well as lower operational efficiency due to a stricter lockdown. This was on the back of a stronger recovery in the smartphone and peripheral markets, although with a narrower net profit growth of 8% year on year.

We like Pentamaster for its structurally well-diversified revenue streams, its core competencies in vision inspection technology (which could drive a more favourable product mix) and decent earnings growth outlook.

The share price has corrected 33% from the mid-February peak of RM6.85. As the stock is trading at a two-year forward PER of 29.6 times against a two-year net profit CAGR of 24%, the negatives have been fairly priced in. This is against the backdrop of the more apparent earnings recovery in 2021, anchored by the acceleration of the capex cycle for the telecommunications, semiconductor and automobile sectors. Maintain “buy”, with target price of RM6.20, based on an FY22 PER of 40 times.

UWC Bhd

Target price: RM7 BUY

HONG LEONG INVESTMENT BANK (JUNE 29): UWC is taking various measures, including leasing a new plant (+10% floor space in Taiping) for expansion and rolling out staff vaccination on June 30 to mitigate Covid-19 risks. UWC may be allowed to operate at 100% capacity once all 740 staff are vaccinated. We remain optimistic about its long-term prospects.

Orders for logic chip testers remain resilient but are expected to trend downwards, replaced by next-generation testers, which is already in the works with mass production target earliest by 2QCY22. Automotive chip testers have the potential to lift its order book by RM30 million and plans to begin production in mid-July coincides with the expected shipment of the robotic arm.

The impact of the Suez Canal blockade, estimated at RM5 million in revenue in 3QFY21, will be recognised in 4QFY21. UWC recently won a project to manufacture 5G V2V autonomous testers.

Reiterate “buy” and retain the target price of RM7, pegged to 50 times CY22 EPS. The escalating trade intensity may eventually benefit UWC, which provides a one-stop solution, as more companies shift production out of China to avoid import tariffs.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.