This article first appeared in Personal Wealth, The Edge Malaysia Weekly on April 8, 2019 - April 14, 2019

Challenger banks have been a trend in markets such as the UK in the last few years, but activity is ramping up in Asian markets like South Korea, Greater China and Southeast Asia, says James Lloyd, fintech and payments leader for Asia-Pacific at EY, in the recently published Citi GPS: Global Perspectives and Solutions report, titled “Bank X: The New New Bank”.

“While we have been supporting emergent players for quite some time, it is in the past year that I have dedicated a large majority of my time to this area. There is a huge amount going on across Asia-Pacific,” he tells the authors of the report.

In Hong Kong specifically, regulatory and infrastructure change is driving a tremendous level of challenger-related activity, says Lloyd. “By way of context, in May last year, the Hong Kong Monetary Authority published a revised Guideline on Authorization of Virtual Banks. In effect, this allows new players to apply for a retail bank licence, with a particular focus on non-traditional players.

“Hong Kong is not the first market in Asia to seek to issue new licences in this way. But it does have particular significance, given the city’s status as an international finance centre, the availability of capital and potential access to the Greater China market.”

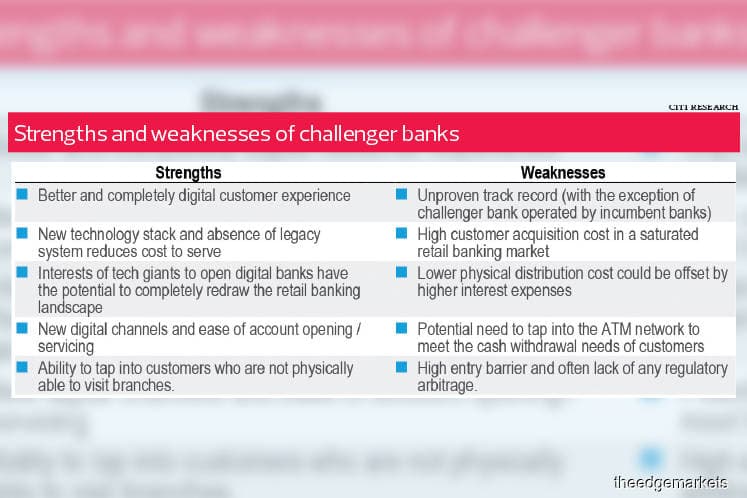

He describes a challenger or virtual bank as a digital-only proposition, one with no branch network. Apart from having an impact on costs, foregoing traditional physical infrastructure, more importantly, also has an impact on the customer experience, he says.

“Virtual or digital banks typically involve online customer onboarding, servicing and engagement. Of course, the specific results, products and services can take many different forms, particularly as a range of different players — from incumbents to platforms — seek to build their own digital-only or challenger banks.

“DBS Bank, for example, has already launched a mobile-only proposition in the growth markets of India and Indonesia. Similarly, CIMB Bank and other regional banks have announced that they are in the process of launching digital-only or mobile-only propositions in markets such as the Philippines and Vietnam. In Hong Kong, Standard Chartered Bank has announced that it is in the process of seeking authorisation for a digital-only virtual-bank proposition.”

According to the report, these new banks are designed around meeting customer expectations, leveraging data insights through agile technology stacks to improve personalisation and offering fully-digital banking experiences. “Challenger banks also tend to be quicker at incorporating new products or processes into their platform and help easily connect with third-party products, offering more choices to the end-user.”

Banks, big tech taking the lead

The authors of the Citi report say challenger banks in Asia are mostly backed by large technology or telecommunications players or traditional banks. For example, WeBank, Mybank and Kakao Bank are backed by tech firms Tencent Holdings Ltd, Alibaba Group Holding Ltd and Kakao respectively.

“Challenger banks originating from start-ups intending to disrupt financial services in Asia (for example, Neat in Hong Kong and Paytm in India) are by far fewer than those originating from start-ups in the UK (for example, Metro Bank, Monzo, Starling Bank and Tandem Bank). A limited regulatory framework for challengers in Asia (with the emerging exception of Hong Kong) and the presence of large tech companies (especially in China) may be some of the reasons Asian challengers are more likely to be an offshoot of a bank or telco,” says the report.

Why are so many traditional banking players coming up with their own challenger banks? Lloyd says the incumbent banks in Asia are seeing first-hand the impact technology-led platform players can have on customer interactions as they expand beyond their anchor use cases and move laterally into financial services.

Many bank CEOs and management teams in the region are re-examining their current propositions and seeking to double down on all aspects of digital customer engagement, says Lloyd. One question to consider is whether to continue investing in existing infrastructure or seek to replace it, either in part or en masse, with a new digital technology stack.

“This is where the opportunity for ‘greenfield’ solutions could be especially powerful — building something off to the side, using components that could perhaps ultimately be brought back into the core proposition. There are huge opportunities associated with building solutions unencumbered by legacy technology, processes and mindsets,” he says.

“That is not to say that all legacy is necessarily bad. Think of the advantages of proven risk management functions, for example. But a combination of both innovative and trusted solutions can be quite powerful.”

In addition to existing banks launching new challenger propositions, other players such as growth-stage start-ups and platforms with an established customer base are also getting involved, says Lloyd. “In the UK, we have seen a range of new start-ups raise funding, build new propositions and begin to organically acquire customers.

“In Asia, platform players are beginning to emerge. Kakao Bank in South Korea, for example, is built on top of the country’s largest mobile messaging service. Similarly, in China, the large internet players have sought to capitalise on their extensive ecosystems by launching a range of first and third-party financial services.”

Lloyd observes a factor that will be especially visible in Asia, that is, building something new provides an opportunity to drive deep strategic partnerships with a variety of players at an equity shareholding level. He says this could be between banks and non-banks, technology players and distribution partners or some combination thereof.

“In fact, I would go so far as to say that a defining feature of challenger banks in Asia will be the emergence of multi-party joint ventures seeking to create true partner ‘ecosystems’ that extend beyond financial services into other areas such as travel, transport, retail and telecommunications,” he adds.

Challenges for the challengers

Lloyd and his team have been supporting the design and development of several “greenfield” challenger banks in Asia. In the last 12 months or so of setting them up, the biggest challenge for new players is getting licensed, he says.

“In Hong Kong at least, the regulator has focused on applicants that can demonstrate sufficient financial, technological and risk management resources to operate a digital-only bank. It has also been necessary to construct a credible and viable business plan, supporting areas such as improved customer experience and financial inclusion.

“Having said that, what I think is going to be different about Hong Kong relative to markets such as the UK is that the strongest new entrants will likely emerge with an established customer base. We will see platforms move laterally into financial services as well as traditional offline networks beginning to leverage their own networks for bank product distribution.”

These players are learning lessons not just from growth-stage UK challengers but also from scale-stage technology ecosystems in mainland China and emergent super applications in Southeast Asia, says Lloyd.

Aritra Chakravatry, founder and CEO of Project Imagine, believes that the biggest stumbling block for incumbents doing challenger banking revolves around people, incentives and organisational structures.

Project Imagine is working to create a second-generation challenger banking and wealth management alternative from scratch. It has been authorised to provide eMoney services as well as distribute, manage and arrange investments for its clients. But is not a bank.

“For instance, if the digital and technology functions of a bank sit outside the finance function and are integrated only at the senior management level, only so much digital-led innovation can take place at the firm. Instead, if technology is embedded in the finance function, it is more likely to offer innovative solutions,” Chakravatry tells the authors of the report.

“There are also product silos — people in a bank looking after only their own product, rather than a customer segment. The people responsible for segments are usually more propositional, so they may talk about the bank’s brand and offerings. But they do not actually make product decisions, which means tailoring products to the customers’ needs is incredibly difficult.”

On incentive structures, Chakravatry says most digital or technological transformations take four to six years to implement, which is quite a big bet with extensive risks for a big bank. In contrast, incentive structures in most banks tend to be driven by yearly performance. So, there is little incentive for individuals to undertake risky transformations at incumbent banks.

Can incumbent-sponsored challenger banks replicate the kind of innovation done by standalone challenger banks? Chakravatry says when an incumbent bank provides its parent brand to its digital arm or virtual bank, or for branding and marketing purposes, it automatically generates interest from management to look over the shoulder of its challenger arm to monitor returns, risk propositions and so on.

“This takes us back to the initial problem of organisational and incentive structures. However, if an incumbent bank can genuinely work at arm’s length, it is possible to replicate the challenger bank model and be equally revolutionary in those areas — with the added benefit of trust from the parent brand as leverage,” he adds.

“It is a race to the finish right now. Will incumbents learn to decentralise decision-making and leverage trust without jeopardising decades of brand value, or will the challengers learn how to consistently deliver, stay funded and win trust while dealing with regulations and governance?

“We will find out one way or another. But ultimately, the customer is likely to win.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.