“Overall, we expect AirAsia to continue running its business as a going concern, in anticipation of a liquidity boost from new loans and equity raising(s). Nonetheless, the business environment remains very challenging and we expect AirAsia to continue reporting losses in the coming quarters.” — Isaac Chow, Affin Hwang Capital Research analyst.

KUALA LUMPUR (July 7): AirAsia Group Bhd posted a record quarterly net loss of RM803.85 million for the first quarter ended March 31, 2020 (1QFY20).

Based on a simple back envelope calculation to annualise the latest quarterly figure, the no-frills airline’s net loss would come to RM3.2 billion.

Analysts, however, will not agree with such simple calculations as there are many variables that would dictate the quantum of AirAsia’s losses in FY20, for instance its hedge on jet fuel, aircraft leasing fees, passenger load and yield, and how soon countries will open their borders for travelling. Furthermore, 1QFY20 is unlikely to be the worst quarter as it did not capture the full impact of Covid-19 outbreak.

Nonetheless, the one thing that is certain is the market consensus view expects AirAsia, whose share price dropped 2.8% to 87 sen at noon break, to post its largest-ever core losses of no less than RM1 billion in FY20, and as its cash flow is getting tight, its management has to fix the problem soon.

At the trading price of 87 sen, AirAsia is valued at RM2.91 billion.

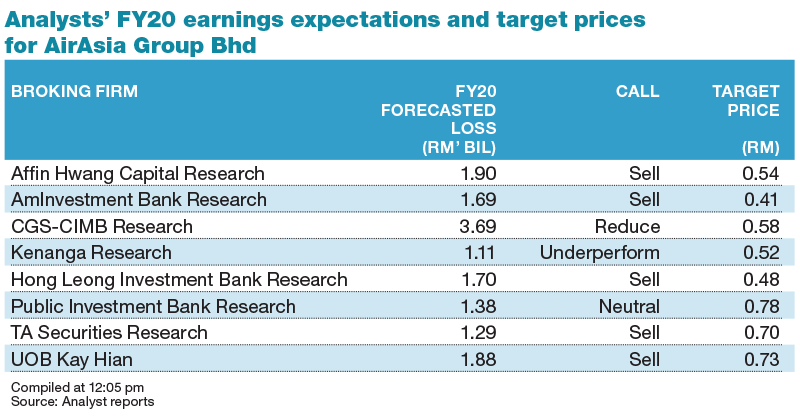

CGS-CIMB Research’s Raymond Yap is forecasting AirAsia to post a core net loss of RM3.96 billion in FY20, and a RM455 million net loss in FY21. He anticipates the budget airline to return to the black with net profit of RM371 million in FY22.

Yap wrote in his research note that the core net loss for 2QFY20 is likely to be worse due to the full impact of the movement control order and border closures across Asean, resulting in an 85% year-on-year drop in available seat-kilometres capacity.

According to him, AirAsia has restructured 70% of its fuel hedges (originally 72% of 2Q-4Q20F and 20% of FY21F budgeted consumption at Brent price of US$60/bbl) by agreeing to settle some over six months and pushing some to FY21F in order to ease cash flow.

The effect of the restructuring will be to transfer some of the unrealised fuel hedging losses currently parked in balance sheet reserves into its profit and loss account in 2QFY20.

“From the peak of losses in 2Q20F, losses may sequentially narrow in 3Q20F as domestic capacity is restored across the various group airlines by late-Jul/Aug but there is no sign yet that international flights can resume meaningfully,” he said via a note.

Given that AirAsia is looking to raise capital, he commented investors should be cautious about investing in AirAsia shares until the size of shareholder dilution, if any, is made transparent.

Yap has maintained his “reduce” call and cut his target price to 58 sen, from 60 sen previously.

Affin Hwang Capital Research’s Isaac Chow said he is expecting AirAsia to report core loss of RM1.9 billion in FY20, from RM1.2 billion initially forecasted. Losses are expected to narrow to RM276 million in FY21, before returning to profitability in FY22.

Chow said new earnings forecasts were done up after incorporating weaker-than-expected 1QFY20 results, lower capacity in 2020 to 2022, higher average fares and more rational competition and lower operating costs in 2021 to 2022 after incorporating lower leasing expenses and other costs.

He maintained his “sell” call and cut his target price to 54 sen, from 78 sen previously.

“Overall, we expect AirAsia to continue running its business as a going concern, in anticipation of a liquidity boost from new loans and equity raising(s). Nonetheless, the business environment remains very challenging and we expect AirAsia to continue reporting losses in the coming quarters. This should, in turn, weigh down its share price,” he noted.

Hong Leong Investment Bank’s Daniel Wong is now forecasting a loss after tax and minority interest (LATMI) of RM1.7 billion for FY20, from a LATMI of RM1.5 billion.

While maintaining his “sell” call with a target price of 48 sen, Wong noted there is ongoing uncertainty resultant of Covid-19, which has also impacted consumer behaviour in air travel demand. As such the group would have to compete in a smaller market to maximise fleet utilisation, with a further risk of cash calls also on the cards.

AmInvestment Bank Research forecasts a net loss of RM1.69 billion in FY20, and a smaller net profit of RM211 million in FY21, from RM219 million previously.

The research house said the earnings downgrade is mainly to reflect a 50% contraction in passengers carried in 2020, from a 35% contraction previously estimated — reflecting the slower-than-expected capacity recovery against a backdrop of weaker demand for air travel amid the Covid-19 pandemic.

It has maintained its “sell” call on the airline while cutting its fair value to 41 sen, from 43 sen previously.

For Public Investment Bank Research’s Nur Farah Syifaa’ Mohamad Fu’ad, AirAsia is expected to post a core net loss of RM1.38 billion in FY20, before posting core net profit of RM24.7 million in FY21 and RM281.5 million in FY22.

“We remain cautious on its earnings outlook for the year as we expect weaker results in 2Q due to loss in revenue after hibernation of the fleet from late March 2020 as travel restrictions increased,” she said.

Nur Farah has retained her “neutral” call on AirAsia with an unchanged target price of 78 sen.

Kenanga Research’s Raymond Choo said he is now forecasting a net loss of RM1.11 billion for FY20 from a net loss of RM556 million. Choo also cut AirAsia’s load factor assumption to 72%, from 79% previously.

While Choo maintained his “underperform” call on the stock, he cut its target price to 52 sen, from 60 sen previously.

“However, this is a high beta stock which could bounce up strongly when Covid-19 is finally overcome,” he opined via a note to clients.