This article first appeared in The Edge Financial Daily, on April 25, 2016.

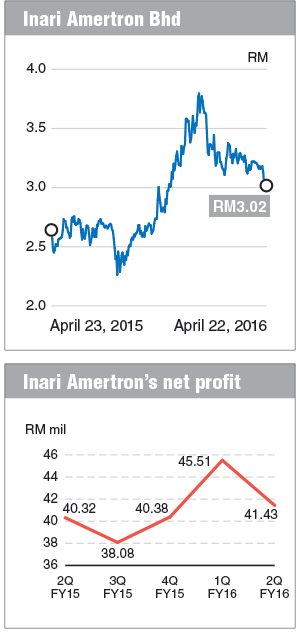

KUALA LUMPUR: Inari Amertron Bhd, the biggest semiconductor player in Malaysia and one of wireless chipmaker Broadcom Ltd’s (formerly Avago Technologies) top electronic manufacturing services providers in the wireless division, saw its share price fall 17.58% to RM3.02 year-to-date (YTD).

KUALA LUMPUR: Inari Amertron Bhd, the biggest semiconductor player in Malaysia and one of wireless chipmaker Broadcom Ltd’s (formerly Avago Technologies) top electronic manufacturing services providers in the wireless division, saw its share price fall 17.58% to RM3.02 year-to-date (YTD).

The stock was a hot favourite last year, which saw its share price climb from as low as RM1.87 on Jan 2 to peak at its all-time high of RM3.8 on Dec 30.

Its recent slump, however, may not come as a surprise to many, given the recent rebound in the ringgit, and the slower sales volume guidance for the first half of 2016 from Broadcom, which makes semiconductors for cellular, automotive and defence industries, and is Inari’s biggest customer.

Interestingly, while Inari’s share price has been falling, Malaysia’s largest fund, the Employees Provident Fund (EPF), has been buying into its shares.

Bourse filings showed that the EPF, which used to hold 5.91% in the company and ceased to be a substantial shareholder of Inari on Nov 24, 2015, re-emerged as a substantial shareholder with a 5.01% interest on Jan 11 this year. As at last Friday, the EPF’s stake had risen to 7.36%.

Besides Inari, its peers like Globetronics Technology Bhd and Unisem (M) Bhd have also seen their share prices trend down of late. Globetronics shares have declined 16.61% YTD, while Unisem shares have dropped 3.78%.

“I think the recent volatility in share price can be tied to the strengthening ringgit and news surrounding cuts in iPhone production [due to weak sales and high inventory levels]. Nevertheless, we do foresee a rebound in the second half of 2016, driven by the launch of new smartphone models,” TA Securities technology analyst Paul Yap told The Edge Financial Daily.

As such, TA Securities is positive on the earnings outlook for Inari, with an expected compound annual growth rate of 23.6% in earnings in the next three years, mainly driven by a ramp-up of production in its P13 plant.

Another fund manager opined that Inari’s strength in the last couple of years had more to do with the group’s business model and not so much the ringgit’s weakness. He also expects the company to continue to do well.

A market observer, however, felt that Inari might have gone into a bit of an overexpansion last year with its new factory in Bayan Lepas, which will be developed as P21, and another land acquisition.

Still, he noted that overcapacity had yet to be seen, but warned that it is a downside risk if there is a drastic fall in global Tier-1 smartphone shipments.

Yap, however, disagreed. “Their expansion plans are supported by growth within the smartphone industry. Although smartphone unit sales have been slowing down, content within smartphones continues to increase. A global LTE (Long-Term Evolution) device has an estimated 4.8 times more radio frequency content value than a typical 3G (third-generation) device.

“Growth can also come from market-share gains, as there is still potential to grow its presence within the Chinese smartphone market,” Yap argued.

Inari recently entered into a memorandum of understanding with Taipei-listed semiconductor firm PCL Technologies Group to form a joint venture (JV) in China, and has bought a 9.7% equity interest in PCL for NT$355 million (RM42.8 million).

The JV is to provide front-end outsourced semiconductor assembly and test services in China and both parties aspire to list the JV within five years. The JV will be split 50:50 between Inari and PCL, but could potentially be diluted by the entrance of other shareholders. Initial capitalisation of the JV is US$20 million (RM77.6 million).

Besides current key customers like Avago, PCL has also indirectly penetrated Huawei’s supply chain in the Chinese market through Huawei’s upstream subsidiary, HiSilicon, and has become an exclusive provider of 10Gb optical transceiver modules.

Alliance DBS Research’s Toh Woo Kim said in his report dated March 31: “We believe the proposed JV between Inari and PCL intends to utilise Amertron’s facility in Kunshan to serve Huawei in the future.” The research house is positive on this venture, given the growth potential of the telecom infrastructure market in China, and customer diversification.

At its current share price level, Inari is trading at a trailing prie-earnings ratio of 16.39 times, way below its historical high of 20 times.

Inari has a strong balance sheet. As at Dec 31, 2015, its cash and short-term deposits with licensed banks stood at RM325.6 million, up 9% from its filing in June 2015, while its borrowings totalled only RM65.99 million, comprising RM39.74 million short-term borrowings and RM26.25 million long-term ones.

“We remain confident in the group’s long-term prospects, supported by its healthy pipeline of expansion plans. However, there may be near-term earnings risk, due to [the] strengthening ringgit and weaker-than-expected demand,” Yap added.