This article first appeared in The Edge Financial Daily on August 16, 2018

YTL Hospitality REIT

(Aug 15, RM1.21)

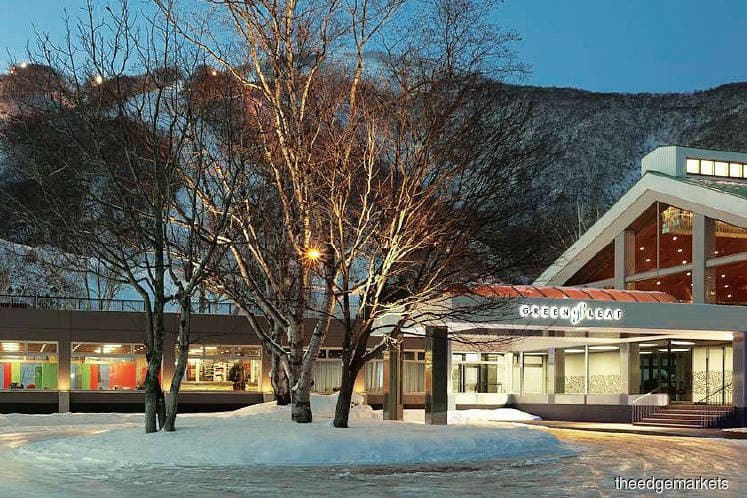

Maintain buy with an unchanged dividend discount model-derived target price (TP) of RM1.32. The report was issued after YTL REIT entered into a conditional sale and purchase agreement with Niseko Village K K, an indirect wholly-owned subsidiary of YTL Corp Bhd for the acquisition of the Green Leaf Niseko Village for a cash consideration of ¥6 billion (RM222.5 million). The property is located in Niseko-cho, Hokkaido, Japan. The 200-room, five-storey hotel was substantially renovated, refurbished and reopened in December 2010.

The acquisition is a related party transaction.

Upon completion of the proposed acquisition, YTL REIT will lease the hotel to the vendor under a 30-year lease agreement, with an option (granted to the vendor) to renew for a further term of 30 years. The initial annual rental payment is ¥315 million for the first five years, with a step-up provision of 5% every five years. The rental translates into an initial gross yield of 5.25%. YTL REIT intends to fund the acquisition via borrowings and internally-generated funds.

We are positive on the acquisition due to the long-term lease of 30 years with option for another 30 years to provide good earnings visibility. The gross yield is at 5.25% and the acquisition is expected to be earnings-accretive in view of the low borrowing cost of around 1% in Japan.

The yen-denominated borrowings will be viewed as a natural hedge for the rental income earned in yen. The acquisition should increase YTL REIT’s gross gearing to 40.3% from 37.4%, which is still viewed as manageable.

We maintain our earnings forecasts for now, pending completion of the proposed acquisition. At a 6.7% yield based on the forecast earnings for FY19, YTL REIT’s valuation looks attractive. The downside risks include a deterioration in the Australian hotel market, interest rate hikes and strengthening of the ringgit against the Australian dollar. — Affin Hwang Capital, Aug 15