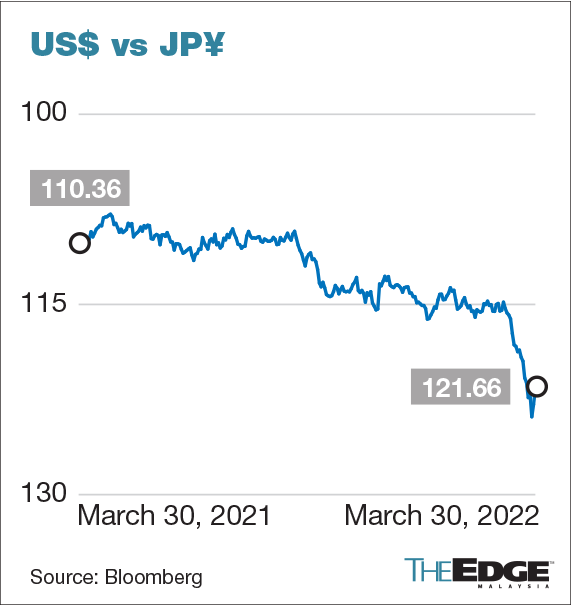

KUALA LUMPUR (March 30): The depreciation of the Japanese yen — which has tumbled to its lowest in seven years against the greenback amid the Bank of Japan’s (BOJ) ongoing purchase of its bonds in a bid to stifle yields and interest rates — appears to be good news for local listed automotive companies who import marques from the Land of the Rising Sun.

However, not all firms are set to benefit, as analysts point out that some of these players import their cars and parts in US dollars instead of yen.

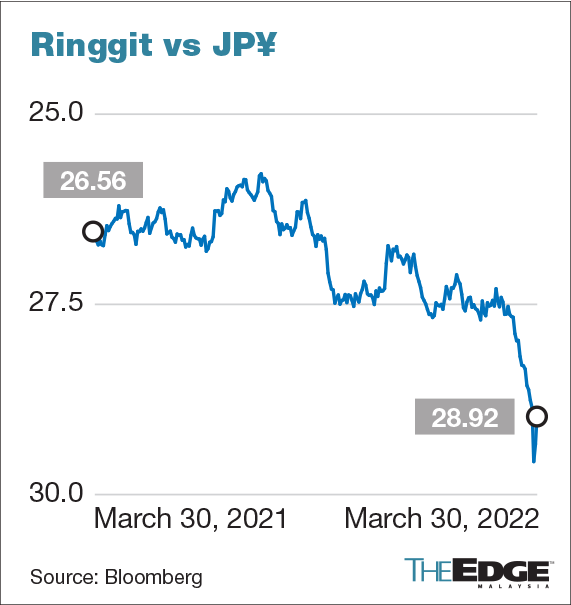

At the time of writing, the exchange rate was one US dollar against 121.86 yen, while the ringgit was trading at 28.47 yen.

Areca Capital chief investment officer Edward Iskandar Toh said the yen weakness is mainly due to Bank of Japan (BOJ)'s preference for a weak yen.

“They announced recently their intention to buy up Japanese Government Bonds (JGBs), effectively keeping their long bond yields ultra low. This is a divergence from other developed nation's monetary policy moving forward,” he said.

Toh noted, however, that the ringgit had also been weakening against many currencies lately, due to rising interest rates in the US and other developed or developing nations.

“So in relative terms, with the yen weakening faster, the ringgit appears to be strengthening against it but not because of any direct move with the yen. Effectively, imports from Japan may now look cheaper,” he said.

Toh noted that the ringgit has weakened against the US dollar by about 2% since the start of the year while yen has weakened about 7% in the same time frame.

“There should not be much of a direct impact right on this weakened yen. Maybe Japanese players are more competitive now in terms of export. However our imports from Japan if quoted in US dollars would have minimal impact,” he said.

Analysts name the top beneficiaries

RHB Investment Bank head of equity research Alexander Chia said auto players whose principal currency is in yen are expected to benefit should the currency remain weak.

“We foresee that it will take up to two quarters for auto players to be impacted depending on the extent and duration of their internal foreign exchange (FX) hedging policies.

“Some auto players import based on the US dollar and as such, not all Japanese marque importers stand to benefit if the currency stays depressed,” he said.

Meanwhile, JF Apex Securities Bhd analyst Jayden Tan opined that in the short term, the divergence in monetary policy between Japan and the US, combined with the trade deficit and worsening of the current account balance of Japan’s government may weaken the yen, but the currency’s performance will normalise in the long term.

Tan added that the weakening of the JPY will definitely benefit local auto import companies such as DRB-Hicom Bhd, UMW Holdings Bhd and Tan Chong Motor Holdings Bhd as they are able to import the vehicles at lower costs.

“However, I do not expect this to bring a huge effect to those companies mentioned as I believe it will be normalized in the long term,” said Tan who has a 'buy' call and target price (TP) of RM3.77 for UMW.

On the other hand, there are views that UMW ('buy' call, TP of RM4) and MBM Resources Bhd ('buy' call, TP of RM4.55) are the key beneficiaries from the strengthening of the ringgit, through their equity stakes in Perusahaan Otomobil Kedua Sdn Bhd (Perodua) as the automaker would enjoy lower landed costs in ringgit terms.

“Bermaz Auto Bhd ('buy' call, TP of RM1.97) also stands to benefit through its associate, Mazda Malaysia Sdn Bhd, which has yen-denominated input cost,” said AmInvestment Bank Bhd analyst Muhammad Afif Zulkaply.

However, Muhammad Afif noted that UMW Toyota — the distributor of Toyota and a subsidiary of UMW — and Tan Chong Motor — the distributor of Nissan — mainly trade in US dollars, so the weakening of the yen has a minimal impact on their earnings.

For MIDF Amanah Investment Bank Bhd analyst Hafriz Hezry, Bermaz Auto ('buy' call, TP of RM1.98) is the biggest beneficiary of the weaker yen among the auto stocks under the firm’s coverage.

Their exposure, he said, is mainly in the form of completely-built-up (CBU) imports denominated in yen for the Mazda brand — CBUs make up around 26% of domestic Mazda sales volume (9MFY22).

“Complete knocked down (CKD) exposure to yen is limited via 30%-owned Mazda Malaysia, which holds the rights to import and assemble Mazda CKDs here.

“Perodua, part-owned by UMW (38%) and MBM Resources (22.6%) has some imported content exposure to the yen, but its models are highly localised in general.

“For UMW Toyota and Tan Chong Motor, imports are mainly denominated in US dollars, so they're unlikely to be big beneficiaries of the weaker yen,” he said.