This article first appeared in The Edge Malaysia Weekly on January 17, 2022 - January 23, 2022

MALAYSIA’s retail industry is looking forward to a recovery after numerous movement restrictions in the past two years because of the Covid-19 pandemic, with Retail Group Malaysia projecting a 6% growth in sales this year from an estimated 0.5% growth in 2021.

However, a tepid recovery is forecast for retail real estate investment trusts (REITs), whose portfolio of assets comprises primarily shopping malls. These REITs have experienced a sharp erosion in distributable income over the past two years and may take a while to bounce back and to recoup rental income lost.

“We have chosen to err on the side of caution, especially as we think that REITs will not completely do away with rental assistance this year. Additionally, we don’t think FY2022 will see prime retail REITs registering pre-pandemic reversion rates of 5% as tenants are still in a relatively tough operating environment, [and] still prioritising survival over growth at this point in time,” RHB Research analysts Raja Nur Aqilah Raja Ali and Loong Kok Wen tell The Edge.

Over the past two years, many shopping malls had to resort to providing rental rebates and discounts to their tenants, who were impacted by the lower level of footfall in malls due to the pandemic.

Area Management Sdn Bhd executive chairman and honorary secretary of the Malaysian REIT Managers Association, Datuk George Stewart Labrooy, says landlords had offered rental relief of up to a maximum of three months in the form of discounts or deferred rent.

“Needless to say, some tenants who could not sustain their operations or cash flow closed down, and mall and office REITs suffered lower occupancy and rental returns from March 2019 till mid-2021 and this negatively impacted their dividend distributions for 2019 to 2021. This was reflected by a drop in their share price during the period.

“The relief provided was for a few months only at the onset of the pandemic when malls were shuttered but I understand that there is no further rental support offered now as the market is starting to recover and footfall is increasing. Kudos to the government of the day as it also offered salary relief to businesses affected by the lockdowns,” Labrooy tells The Edge.

On whether the “new normal” between mall tenants and landlords could mean shorter leases given the uncertainties in the current operating environment — the economic impact of the Omicron variant, for instance — Labrooy explains that malls typically do not offer long-term leases, with the exception of anchor tenants such as supermarkets and designer labels that are capable of drawing in the crowds.

“The norm is for two-year renewable leases only. It gives mall managers the flexibility of changing the tenant mix to suit the trends of the day. What had saved the day for retailers was their ability to pivot quickly to an e-commerce hybrid model for their retail distribution. They soon realised that e-commerce gave them a 24/7 retail model with no rent and staff to pay.

“The new normal for retail is still evolving. Some mall managers — for example, Sunway Pyramid and 1 Utama — have set up e-commerce trading platforms for their tenants and there is a move towards more experiential malls in the future. Many new retailers are also entering the fray, providing Malaysian consumers with a much wider choice,” he adds.

How attractive an investment are retail REITs?

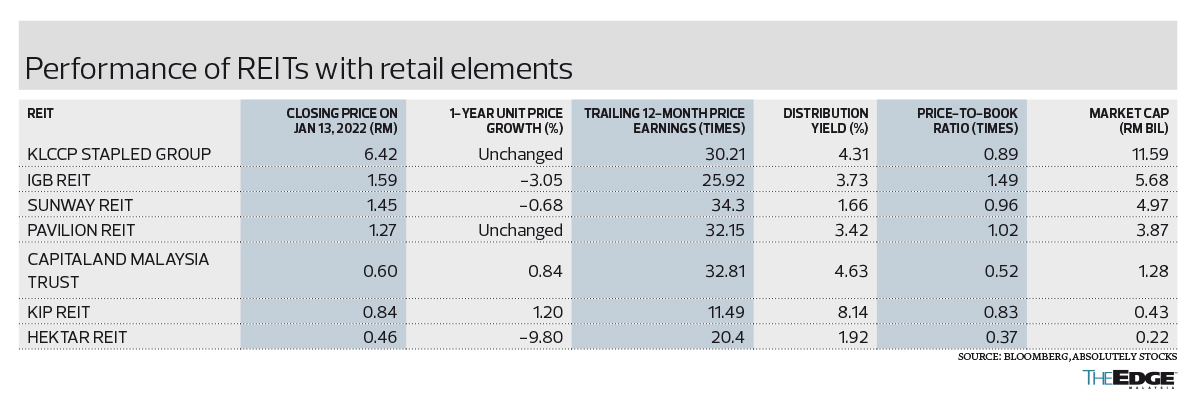

A quick check on the unit price performance of retail REITs over the past year shows a muted growth of between 0.84% and 1.2% for a couple of them, while others saw a decline of almost 10% during the period. Trailing 12-month (TTM) distribution yields ranged from 1.67% to 8.14%, with KIP REIT — whose investment portfolio comprises KIPMalls in Bangi (Selangor), Johor, Melaka and Negeri Sembilan as well as AEON Mall in Kinta City, Ipoh — charting the highest TTM yield.

Private investor and former investment banker Ian Yoong Kah Yin, who is overall neutral on retail REITs, believes it is an asset class worth considering at this juncture given that it is coming from a low base.

“In my view, 2021 was the nadir for retail REITs [as] we have seen the worst that Covid-19 can bring. [While] the government has assured us that there will not be any lockdowns going forward, the anticipated increase or series of increases in global interest rates this year is more daunting.

“The US Federal Reserve Board has indicated that it will increase interest rates in 2022, in addition to the dreaded taper. It is highly likely that domestic interest rates will follow suit. The yield for the 10-year Malaysian Government Securities (MGS10YR) will most likely increase from the current 3.67% to 4% by 4Q2022.

“The yield spread between retail REITs and MGS10YR is 40bps with MGS10YR at 3.6% and average retail REITs at 4%. The yield spread has to widen significantly for retail REITs — for this sub-sector — to be attractive,” Yoong tells The Edge.

Datametrics Research and Information Centre Sdn Bhd (DARE) managing director Pankaj C Kumar projects a recovery this year as he expects consumer spending to return to pre-pandemic levels.

“With the economy back on its feet, I foresee demand for space increasing, although it may take a while before we see an upward revision in rental rates. Landlords too will be in a better position as they would not need to provide any more rental rebates, hence enhancing the REITs’ bottom line as well as dividends to unitholders.

“The way I see it, our listed retail REITs are in a class of their own and most of them run premium malls and not mediocre ones where the asset manager may find it tough to attract not only the right tenant mix but also footfall. Hence, except for a few malls owned by one or two of the listed retail REITs, most of them will not be impacted by the current glut experienced in the sub-sector and to the contrary, will continue to attract top-tier brand names,” he opines.

Even a potential hike in the overnight policy rate (OPR) by Bank Negara Malaysia this year, which could make the investment proposition for retail REITs less attractive, is not expected to have a major impact, according to Pankaj.

“The OPR is set to rise by between 25bps and 50bps this year but even if Bank Negara were to move by 0.5%, the potential move to as high as 2.25% is still well below the 3.00% mark before the emergence of Covid-19 in early 2020. Hence, even a 50bps hike will not result in the retail REIT sector being impacted greatly but the listed REITs would carry relatively higher borrowing costs as most of them have borrowings that are based on floating rates. This may eat into their profitability but I do not foresee that to be a significant factor that will undermine earnings and dividends visibility in a big way,” he explains.

A rising interest rate environment would also see property prices and rents rise, which would improve the performance of REITs, says Labrooy. “It will also create an environment where acquisitions may be more accessible, and with growth comes better share valuations and better total returns.”

For Yoong, the distribution yield for IGB REIT, which manages Mid Valley Megamall and The Gardens Mall, is attractive. “Yield is 3.69%, which we expect to improve to 4% for FY2022. The location and branding of Mid Valley Megamall and The Gardens Mall is a formidable moat.

“According to the latest annual report, the occupancy rate of Mid Valley Megamall stands at 99% while that of The Gardens Mall is 92%. These are impressive occupancy rates in a pandemic,” he points out.

IGB REIT is also the choice of RHB’s Nur Aqilah and Loong, as they say the key is to prioritise asset quality with the recovery theme in mind.

“We would focus on REITs that have demonstrated robust occupancy levels despite the pandemic, a domestic shopper profile so as to not be impacted by our still-closed international borders, as well as a strategic rental structure to fully capitalise on improving tenant sales. For these reasons, our preferred pick within the retail space is IGB REIT.

“We like IGB REIT as a proxy for the recovery theme due to the undeniable quality of both Mid Valley Megamall and The Gardens Mall. Their strategic location with a wide catchment area will allow it to fully reap the benefits of revenge spending, further complemented by its strategic rental structure where its turnover rent portion is the biggest among the retail REITs in our universe. Its minimal dependence on international shoppers is also a plus point while the reopening of international borders remains a moving target at this point in time.”

RHB has a “buy” call on IGB REIT, with a target price of RM1.92, or an upside of 21% over its closing price of RM1.59 last Thursday.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.