KUALA LUMPUR (Oct 6): Moody’s Investors Service has revised the outlook for the global shipping industry to negative from stable.

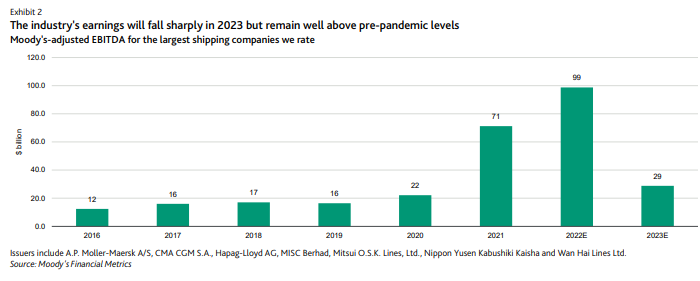

In a report titled “Shipping — Global: Outlook turns negative as earnings peak, macroeconomic environment worsen” released on Thursday (Oct 6), the firm said the industry's aggregate earnings before interest, tax, depreciation and amortisation (Ebitda) have likely peaked, and will decline sharply in 2023, because of tough comparisons to current data and rising economic risks.

“Our outlook is primarily driven by container shipping and its stellar performance in 2022, as well strong earnings for dry bulk carriers, which will be difficult to match next year.

“Rapidly slowing growth in Europe's largest economies amid general high inflation and soaring electricity prices, and a bleaker outlook for global economic growth pose risks to the industry as a whole.

Moody’ global shipping outlook had been stable since December 2021.

The firm said carriers are on course for another year of record high profitability.

However, it said signs pointing to a more benign market environment in 2023-24 abound — an order book implying supply greatly outstripping demand, decreasing utilisation rates and falling spot rates.

“That being said, carriers have very strong balance sheets, and are already trying to address softening demand by cancelling sailings as well as through more transformational actions, such as diversifying into terminals, airfreight and third-party logistics,” it said.

Moody’s said the redirection of oil trade flows following Russia's invasion of Ukraine (Caa3 negative) has led to higher tonne-mile demand for tankers, especially for Aframax and Suezmax vessels, as many European companies source crude and oil products from more distant markets.

It said charter rates have already risen this year, and it expects rates to remain at least stable over the next 12 months, given the ongoing geopolitical tensions and limited supply of new vessels scheduled for 2023.

However, it added that weakening global growth poses risks to global oil demand.

“We would consider changing the outlook back to stable if we expect the difference between shipping supply and demand growth to be within a range of -2% to +2%, and if we expect the industry's year-on-year aggregate Ebitda growth to be between -5% and +10%,” it concluded.