This article first appeared in Personal Wealth, The Edge Malaysia Weekly on August 28, 2017 - September 3, 2017

Last October, the government launched the Net Energy Metering (NEM) scheme for those who wish to sell the excess electricity generated by their solar panels to the utility companies. This allows homeowners, as well as commercial and industrial users, to adopt renewable energy and potentially generate some cost savings.

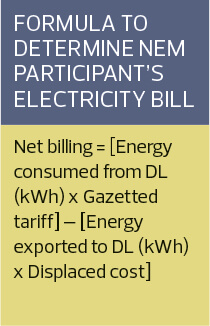

The excess electricity can be sold to the utility companies in Peninsular Malaysia or Sabah at a rate known as the displaced cost. For low voltage systems, which would be used by most homeowners, the displaced cost is 31 sen/kWh.

For commercial and industrial users with higher voltage systems, the displaced cost is lower. However, it rises when the tariffs are increased.

Participants of the scheme receive credits that can be used to offset future electricity bills. The credits expire after 24 months.

Under the NEM scheme, some 500mw of electricity can be sold to the utility companies from 2016 to 2020. Participants in Peninsular Malaysia can sell up to 90mw a year while those in Sabah can sell up to 10mw. The unused quota from each year can be carried forward to the following year.

The scheme, however, has not caught on with Malaysians. So far, none of the quota has been taken up in Sabah while only 3.0726mw has been taken up in Peninsular Malaysia. Also, the take-up rate is lower among homeowners than commercial and industrial users.

Sustainable Energy Development Authority Malaysia (Seda) chief operating officer Akmal Rahimi Abu Samah says the NEM scheme was introduced because the Feed-in Tariff (FiT) scheme was considered unsustainable as the utility companies would have to pay participants a premium rate for 21 years. “This is a natural progression because it is happening in other countries as well,” says Akmal Rahimi.

“They started with FiT to get the ball rolling. When people are more experienced and can see the benefits of such schemes — and there are enough market players — then we can move on to other less costly programmes that can enlarge our renewable energy mix.”

Users who consume a lot of electricity and want to invest in solar panels to take advantage of the government’s incentives for renewable energy generation may consider participating in the NEM scheme. Akmal Rahimi says homeowners should consider a few factors to determine whether the scheme is suitable for them.

“Number one is the tariff they are enjoying at the moment. When you do the analysis, you will find that the scheme is suitable for those in the medium and high-income groups because they tend to use more electricity and have to pay higher tariffs,” he says.

“If these groups can generate electricity on their own, they will be displacing their energy costs. So, that is where the savings come from.

“But if you use very little energy, your cost is quite low. Then, the NEM scheme may not be very attractive for you.”

Domestic electricity consumers are charged according to the tariff blocks set by the utility. For example, those who use less than 200kWh a month are charged 21.80 sen/kWh in Peninsular Malaysia. The most expensive tariff block is 57.10 sen/kWh.

“Under the NEM scheme, participants are not actually trying to sell energy to the utility companies. What they are trying to do is not buy electricity from the utility companies when their consumption is high,” says Akmal Rahimi.

“Those who have electricity bills of more than RM500 a month are good candidates for the NEM scheme because it is a form of energy cost saving. By generating the electricity themselves, they save money that they otherwise would pay to the utility company.”

Consumers who want to contribute to clean energy production because of their environmental concerns or those who are looking to be free from any increases in the tariffs set by the utility companies may also consider participating in the NEM scheme. Such schemes are particularly popular in countries with high tariffs, says Akmal Rahimi.

While the tariffs are relatively low in Malaysia, a rate hike may be imminent as production costs are rising and the tariffs are up for review next year. “When we promote the NEM scheme, we try to highlight that in some cases, it may not look attractive or viable at the moment. But once the tariffs go up, then you can see that the return on investment becomes higher and the payback period becomes shorter,” says Akmal Rahimi.

“The tariffs will keep increasing in the future. They will never go down. So, this is just a starting point for the NEM.”

William Lean — an independent solar power producer who was involved in creating a solar loan product with Alliance Bank for the FiT scheme — agrees that the NEM scheme may be a good way to partially protect against future tariff increases. He adds that the decline in the cost of solar panel equipment over the years has made the investment more viable.

“The NEM scheme is the latest evolution in incentives to bring individuals and corporates to the independent solar power production space,” says Lean. “The FiT scheme was much more attractive and helped create a vibrant solar industry in Malaysia. For example, the power purchase agreement in 2013 went as high as RM1.57 per kWh.

“However, the system cost was just as high. A 12kW solar system, which is good for a bungalow, cost as much as RM150,000 back then. Today, it is only about RM55,000.”

The downside of the NEM scheme is that participants will not be able to enjoy a payback period of five to seven years, which was possible under the FiT scheme. Instead, it will take 11 to 15 years, says Lean.

Installation can be costly

Akmal Rahimi estimates that the payback period may be around 10 years for a consumer who pays the highest tariff block and purchases a solar panel that costs RM6,000 to RM7,000 per kW. “You have to remember that the lifetime of a solar module is very long. Even the warranty from the manufacturer is 25 years, and a lot of systems can last 30 years,” he says.

“Some people may say 10 years is too long. But if your system can last 30 years or more, it means that after 10 years, your energy is totally free.”

A list of registered solar photovoltaic service providers is available on Seda’s website. Michael Leong, manager of Tera Va Sdn Bhd, which is one of the service providers, says it performs an analysis for customers based on their energy usage and patterns.

“When the customers come to us, we conduct an interview to find out things like how they consume the energy, the periods in which they consume it and the duration. Then, we come up with a suitable solution for them,” he adds.

“With the FiT scheme, you could go for the maximum capacity. But with the NEM, we have to come up with a system that is just good enough for the clients to optimise their returns.”

He says there has been interest from those who consume lower amounts of electricity as well, although the interest from homeowners is weak compared with that of commercial and industrial users, which can benefit from tax allowances.

The average cost of a solar panel is between RM4,500 and RM6,500 per kW and those used by homeowners can range from 1kW to 15kW, says Leong, who estimates a payback period of 8 to 10 years.

But the initial investment for installing a solar panel can be prohibitive. When the FiT scheme was introduced, some banks came up with loan products for solar panel installation. However, there are none available for the NEM scheme at the moment.

Akmal Rahimi says he recognises the lack of financial support for domestic users and is trying to do something about it. “Earlier this year, we talked with the Energy Commission about some kind of tax relief for those who purchase solar modules, but we don’t know the outcome yet.

“There was also a suggestion of a solar leasing programme so consumers do not have to come up with a large chunk of money up front. They can just go to these solar leasing companies and purchase on instalment.”

He has received feedback from commercial and industrial users and says they prefer the savings to come in the form of cash rather than credits and the net energy amount to be calculated with the prevailing tariff rate.

Lean hopes that the displaced cost for homeowners can be increased so that it is on a par with the rate given to commercial and industrial independent power producers (IPPs) through their power purchase agreements and Large Scale Solar (LSS) projects. “From the numbers, it would appear that the displaced cost for the homeowners is lower than the rate given to the large IPPs. A higher displaced cost would, of course, improve the returns from the NEM scheme and provide more homeowners the opportunity to generate more attractive returns from producing solar power,” he says.

“A suggestion for a level playing field between individuals and corporates is to raise the displaced cost for homeowners to at least the tariff rate of the LSS producers or IPPs. Let the small guy have a chance to have a solar panel on his rooftop at a decent rate as well.”

Those who are interested in buying a solar panel could apply for a low-interest-rate loan, Lean suggests. “There is some space to improve the return on equity (or cash) if there is a low-cost loan. For homeowners, potentially the cheapest way is to refinance their home, especially if it was purchased some time ago,” he says.

“The concern about this angle is that the global interest rate has just started an up cycle that may last several years. At this juncture, a fixed-rate loan would be more prudent to avoid interest rate risk. It would be useful for the authorities to engage consultants or organise financing packages with the local players.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.