This article first appeared in The Edge Malaysia Weekly on November 23, 2020 - November 29, 2020

THE slew of news reports pointing to encouraging progress in the development of Covid-19 vaccines is weighing on glove stocks as investors shift from a pandemic play to a recovery theme.

With several vaccine candidates reportedly highly effective at preventing Covid-19, what is the chance of a rebound for glove stocks, which have enjoyed massive gains since early this year?

An analyst believes the glove sector, which comes under his coverage, has not disappeared from investors’ radar screens yet, although the stocks are expected to remain weak in the short term owing to market sentiment and the current news flow.

“We still have an ‘overweight’ call on the sector. The supply-demand dynamic for the next two years, at least, will not be back to pre-Covid-19 levels. Also, infections have not come down yet and vaccines are not 100% effective. I believe the glove theme will come back. It is just a matter of time,” he tells The Edge.

Moreover, he thinks the average selling prices (ASPs) of gloves can be sustained at current levels for at least another year. “The ASPs have been locked in for 1Q2021 and are unlikely to drop in 2Q2021 and 3Q2021. So, the super earnings for 2021 are guaranteed. You can’t ignore these super earnings,” he says.

Optimism about a break in the pandemic cycle is in the air after Pfizer and Moderna boasted that their vaccines have high rates of effectiveness. Pfizer claimed that its vaccine, co-developed with BioNTech, was more than 90% effective in early analysis while Moderna’s experimental vaccine was 94.5% effective.

In China, Sinovac Biotech’s CoronaVac vaccine reportedly led to a quick immune response during clinical trials.

ASP growth remains strong for big players, except Supermax

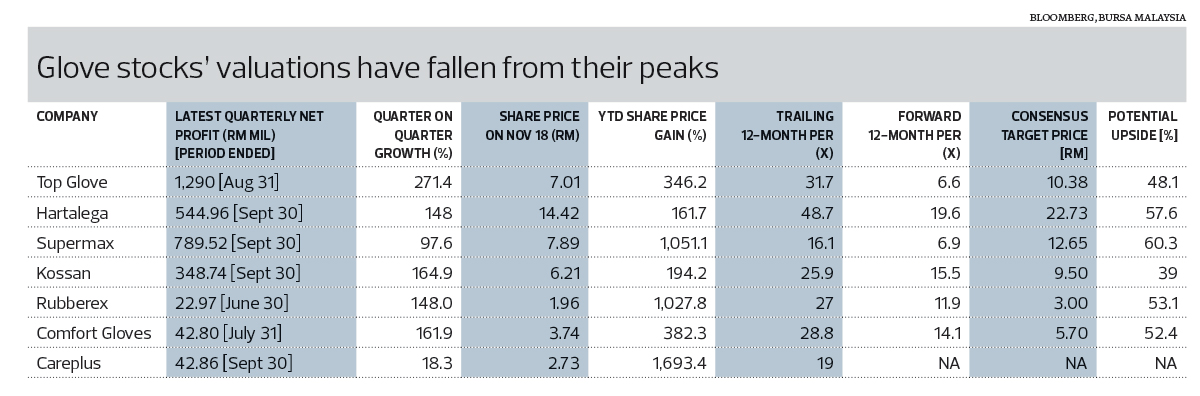

The analyst says stocks such as Hartalega Holdings Bhd and Kossan Rubber Industries Bhd are still playing catch-up in terms of ASPs, especially for 1Q2021. “On a quarterly basis, it will be at least 40% higher for Hartalega and Kossan for 1Q2021 versus 4Q2020. There is no guidance yet for Top Glove, but it is still on an uptrend.”

However, Supermax’s ASP growth is projected to be flattish at 5%, as it was the most aggressive player previously, owing to its own brand manufacturing model.

The analyst believes Kossan and Hartalega are safer bets as their downside risks are more limited than those of Supermax, the stock price of which has gained more than 1,000% year to date (YTD). Supermax’s quarter-on-quarter earnings growth has also slowed compared with its peers. “When ASPs start coming down, the first mover — which is Supermax — will be hit first,” he adds.

In his view, Kossan remains attractive. The glove maker’s annual production capacity is expected to rise to more than 40 billion pieces from 32 billion pieces this year.

“The YTD share price gain for Kossan is close to 200%, but it is making close to 20 years of profits in just these two years,” the analyst observes.

Although profits remain commendable for smaller players such as Rubberex Corp (M) Bhd, Comfort Gloves Bhd and Careplus Group Bhd, the analyst opines that their valuations are more expensive. “Take Careplus, although the company has been expanding, its production capacity is not that big, so the profit is capped compared with the big players.”

Inter-Pacific Securities analyst David Lai also believes that selling prices will not taper off until the second half of next year due to a lack of supply from the new players. “Earnings growth will remain intact next year. Nobody knows by how much the ASPs will soften going into 2022. Looking at the share prices, it is a bargain, but sentiment is not with them.”

Forward PER falls to single digit for Top Glove, Supermax

However, another analyst is doubtful that investor enthusiasm for glove counters can hold up, given the strong vaccine news flow. “The fall in the share prices of glove stocks are in line with my expectations. Investors already knew what would happen in 2022 and 2023. With earnings set to fall drastically after 2021, would you still buy into the stocks? That is my concern.

“If you look at the forward price-earnings ratio (PER) for Top Glove, it is just around six to seven times, which does not make sense. This is because the market is already looking forward to earnings after the peak. This is how the market behaves in reality.”

Given the low valuations, is the time right to bet on glove stocks?

“I wouldn’t say the glove story is gone. Demand will still be there post-pandemic. Trading opportunities are always there. But bear in mind that the downside risk is significantly higher than the upside risk. I highly doubt Top Glove’s share price will climb back to the [previous] high levels,” he opines.

Top Glove’s share price hit a high of RM9.72 after its bonus issue went ex in early September. Currently, the consensus target price for the country’s biggest glove maker is RM10.38, according to Bloomberg data. This implies an upside potential of more than 48% against its close of RM6.94 last Thursday.

Supermax’s forward PER has declined to 6.9 times while Hartalega is the most expensive at 19.6 times.

Bloomberg data shows an upside potential of 39% to 60.3% for glove stocks, with Supermax having the most upside based on analysts’ consensus target price.

Interestingly, the recent fall in share prices has prompted a handful of players to embark on share buybacks. Top Glove, for instance, spent RM209.78 million last week buying back its shares, raising its cumulative net outstanding treasury shares to 115.42 million, or a 1.41% stake. The company has splurged some RM489.23 million this month on share buybacks, adding to the RM355 million spent last month.

The Employees Provident Fund (EPF) has been accumulating Top Glove shares and now owns 6.4% of the company, from 5.67% at end-October. In addition, the pension fund has increased its shareholding in Kossan to 8.82% from 8.35% last month.

Kossan founder Tan Sri Lim Kuang Sia has also been buying. Through his private vehicle, Kossan Holdings (M) Sdn Bhd, he bought 0.02% shareholding, raising his direct and indirect equity interest in Kossan to 0.196% and 47.05% respectively.

Careplus CEO Lim Kwee Shyan has been actively acquiring the company’s shares, with his direct stake inching up to 18.89% from 18.86% earlier this month. His indirect equity interest remains unchanged at 5.32%.

However, Rubberex’s major shareholder Datuk Ong Choo Meng has been selling. He pared down his indirect stake in the company to 51.06% from 52.22% last month, but still holds a direct equity interest of 3.73%. Ong ceased to be a major shareholder of Comfort Gloves in September as his shareholding was reduced to 4.99%.

Interestingly, Top Glove executive director Lim Cheong Guan had also been paring down his stake. He sold a total of 610,000 shares in September and October, trimming his equity interest to 0.011% from 0.012% in July.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.