This article first appeared in Personal Wealth, The Edge Malaysia Weekly on November 13, 2017 - November 19, 2017

Emerging-market bonds are expected to continue seeing investment inflows amid the start of the US Federal

Reserve’s rate hike cycle. This will give bond prices a leg-up going forward, says Sergei Strigo, head of emerging markets debt and currency at Amundi Asset Management in London.

“We see further room for yield compression and prices going up within the emerging-market bond space,” he says.

According to Strigo, the inflows are due to an improving global economy, which has seen growth recovering and unemployment rates remaining low. Commodity prices have also experienced a boost. All these are seen to benefit emerging markets.

The yield-chasing phenomenon is expected to continue. That is because interest rates and bond yields globally are still low despite the rate hike cycle kicking off.

“Emerging-market bonds offer yields of 7% to 10%, which is very attractive to investors looking for higher income,” says Strigo.

However, bond prices are not expected to rally significantly this year compared with last year. “Emerging-market bond yields in general are expected to compress another 30 to 40 basis points, depending on the interest rate movements,” he says.

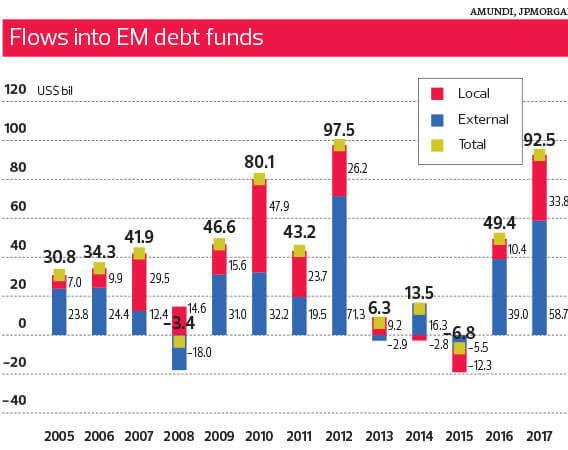

Referring to a JPMorgan chart, Strigo says investment inflows into emerging-market bonds from January to October hit US$92.5 billion — the second highest since 2005. The biggest investment inflow, totalling US$97.5 billion, occurred in 2012.

Meanwhile, the two largest outflows took place in 2008 and 2015, totalling US$3.4 billion and US$6.8 billion respectively. The first instance was when the global financial crisis erupted while the second was when China devalued its currency amid an economic slowdown.

Brazil and Russian government bonds attractive

Strigo and his team prefer hard currency bonds at this stage as the strength of the US dollar is unclear in the short term due to the uncertainties surrounding key events. The uncertainties are mainly due to the expected retirement of Fed chair Janet Yellen early next year and who her replacement will be. A candidate with a hawkish stance would strengthen the greenback.

Another factor is the tax reform in the US that seeks to lower the corporate tax rate. The US dollar is expected to strengthen against emerging-market currencies if Congress passes the bill.

“Bonds denominated in hard currency (referring to currencies that are widely accepted globally such as the US dollar, euro and yen) will eliminate or reduce currency risk,” says Strigo, adding that this is important as most bond fund managers do not hedge currency risks due to the high cost involved.

Within the soft currency space, which encompasses currencies that fluctuate in value due to economic or political uncertainties, Strigo favours Russia and Brazil government bonds. Russia is benefiting from an improved economy, which came out of a recession two years ago, and the recovery in oil prices.

On Nov 1, Brent crude oil hit US$60 a barrel — the first time in more than two years — mainly due to the Organization of the Petroleum Exporting Countries (Opec) cutting production. Prices are expected to remain relatively stable in the range of US$40 to US$60 a barrel moving forward, which will benefit Russia, says Strigo.

Also, the inflation rate remains low in Russia and below the central bank’s target while interest rates stand at 8.5%. This gives the central bank room to cut rates further, which is positive to the government and its bondholders.

“Yes, cutting rates could cause its currency to weaken. But this is offset by more investors buying into Russian bonds, which will help its currency to remain relatively steady,” says Strigo.

Meanwhile, the Brazilian government has instituted reforms to stabilise its fiscal position despite facing political challenges. According to news reports, at the end of last year, the government passed a spending cap — known as PEC 55 — for the next 20 years. In July, it passed a labour reform bill, which is aimed at cutting business costs by allowing companies to negotiate contracts freely with employees. A pension reform bill is expected to be tabled soon to overhaul the country’s costly pension system.

These efforts by the Brazilian government, however, have sparked protests in the country, especially among union workers. The United Nations has also said that the PEC 55 austerity package will “hit the poorest and most vulnerable Brazilians the hardest and increase inequality levels in an already very unequal society”.

The country’s situation was made even more complicated when President Michel Tremer was charged with bribery. Congress, however, blocked the charge against Tremer, saving him from a potential Supreme Court trial and impeachment. With a general election scheduled for October next year, it is uncertain whether he will remain in office.

From an investment perspective, Strigo sees these reforms as a positive sign. He is keeping a close watch on news related to the upcoming general election.

“I am comfortable investing in Russian and Brazilian local currency government bonds as their currencies are pretty stable. The yields range from 7.5% to 10%, which is very attractive,” says Strigo.

Keeping an eye on NAFTA renegotiation

Volatility during a rate hike cycle could be an investor concern. But Strigo does not foresee high volatility nor a strong reversal to occur in the emerging-market bond space this year.

This is mainly due to a gradual rate hike taking place and an improved communication between central banks and the markets. “The markets have priced in the rate hikes,” he says.

China’s economy is a key risk to emerging-market bonds, but Strigo is not worried at this point in time. “The country has been stable so far. Its government has managed the economic slowdown to a certain level without having major volatility. The continuation of this — which we believe will be the case — will be very positive for the market.”

One event that he is keeping an eye on is the renegotiation of the North American Free Trade Agreement (Nafta). “The outcome will certainly affect emerging markets and especially Mexico,” he says.

According a news report, the fourth round of negotiations ended on Oct 17 and the fifth round has been pushed back until mid-November to give the negotiators more time to work on the more controversial issues. Representatives of Canada, Mexico and the US issued a joint statement on their previous meeting to highlight their progress and intention to reach a deal, reported by CNBC.

The report says the individual remarks given by the representatives after the joint statement painted a more pessimistic picture on finding common ground. US Trade Representative Robert Ligthizer reportedly said, “Frankly, I am surprised and disappointed by the resistance to change by our negotiating partners on both fronts.”

Meanwhile, Mexico’s Economy Minister Ildefonso Guajardo reportedly said, “All parties must understand that we all have limits [in order to reach a fruitful agreement].”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.