(May 8): Malaysia’s 14th General Election is drawing near, with the Press calling it the “mother of all elections”, referring to the major changes to Malaysia’s political scene in recent years.

Chief among them include the resignation of former Prime Minister Tun Dr Mahathir Mohamad from the ruling party, UMNO, in protest of current caretaker Prime Minister Najib Razak’s handling of the 1MDB scandal.

His resignation was followed by resignations of other senior party leaders and the formation of Parti Pribumi Bersatu Malaysia (“Bersatu”) and the participation of Bersatu in Pakatan Harapan (“PH”) together with DAP and PKR in Peninsular Malaysia.

With Pakatan Harapan and the Barisan Nasional campaigns underway, several differences emerged between GE13 and GE14. The inclusion of Bersatu into Pakatan Harapan has allowed the PH to hold rallies and campaign speeches in rural Malay villages and FELDA settlements that were previously inaccessible to Opposition politicians.

However, settlers and rural Malay voters are still reluctant to be demonstrative about their support for PH — as evidenced by their reticence to stand in the light of the campaign tents, preferring to linger on their motorcycles and remain in the dark — as the issue of social isolation (“dipulaukan”) is deeply felt in these tightly-knit communities.

In mid-2017, an INVOKE Malaysia survey found limited increase in support for the Barisan Nasional. All that has changed in 2018, with Opposition politicians estimating 5%-15% declines in support for BN among rural Malaysia, especially in non-FELDA settlements.

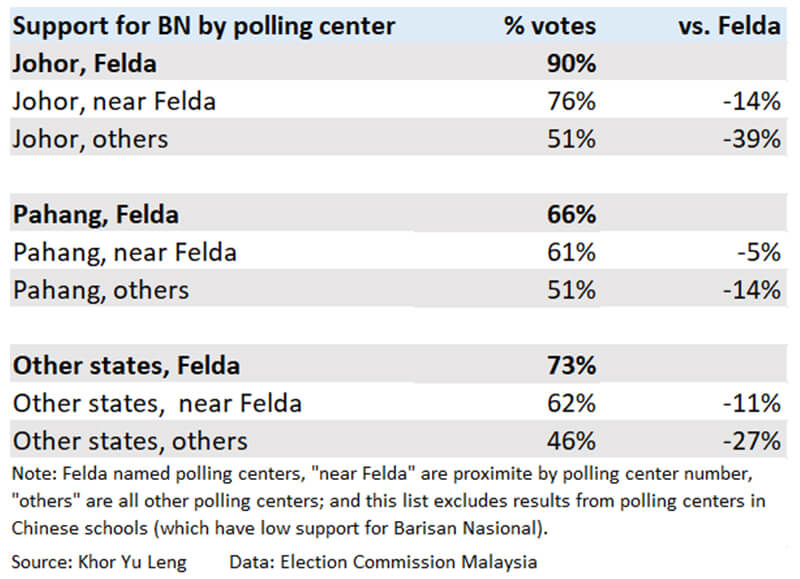

To explore these differentials between FELDA and non-FELDA settlements, we reviewed voting preference data from the Election Commission on GE13 Parliamentary election votes (Table 1). This data excludes voting outcomes from polling centers at Chinese schools (an obvious segment, but clearly it is impossible to differentiate ethnic preferences in regular schools), as the focus is on the Malay vote.

It shows that Pahang was more homogeneous in voting outcomes between Felda and kampung biasa (proxied by “near Felda” data) in GE13, and that Johor shows a wider differential of -14%-age support for BN in 'kampung biasa' versus Felda settlements. Thus, BN support within Felda was greater in Johor than in Pahang versus regular kampungs. Overall, support for BN was higher in Johor than Pahang, which is greatly influenced by PAS.

Click / Tap image to enlarge

Field Notes

We also recently took a trip through rural settlements Pahang and Johor to understand the challenges faced by smallholders, their sentiments towards the election, and what the potential impact might be on GE14. Based on our observations and previous research on FELDA, we compiled some field notes to share on the economic conditions faced by settlers.

The first thing one notices when driving into a FELDA settlement is the density of the trees. The roads are flanked by densely-packed palm oil plantations that stretch out across the horizon. Most settlements are in remote areas of Pahang and Johor, between 15 minutes to more than an hour’s drive from the nearest town. This lack of integration means smaller and more remote settlements only have access to basic products and services at their local D’mart (a small grocery chain run by FELDA) and nothing much else.

The isolation has an impact on bread and butter issues such as the rising cost of living which are affected by rising costs of consumer goods and lower palm oil prices (now down to RM2,300/MT from their peak of RM3,200/MT in late 2016). Products sold in settlements can be more expensive than the same product found in supermarket shelves in the towns and cities due to additional costs needed to transport the products from distribution centers in urban areas to the settlements. Settlers see this price differential in everyday products like vegetables and chicken (RM6 in the town and RM8 in settlement, according to a Johor settler). Settlers from Lok Heng Barat near Kota Tinggi, Johor, were frustrated as rising consumer goods prices increased their cost of living. From their perspective, wages have stagnated, as palm related incomes ranged between RM1,000-RM3,000 and is split between all members of the second generation, sometimes up to six families. It is this distribution of income and assets among the second generation that impacts smallholder incomes more than macroeconomic issues such as the EU’s RED II policy.

Additionally, many first generation settlers are approaching their 90s and depend on their children for support. As it becomes impossible to survive on palm incomes alone, many second and third generation settlers commute between settlements and the town centers in search of work as general contractors, shopkeepers, salespeople, and as manual labour. Some families get by with additional remittances from family members who migrated to the urban centers of Singapore, Johor Bahru, Kuala Lumpur, and Penang. However, with stagnant wages and the introduction of GST, their wallets are squeezed even further, and PH has leveraged on this frustration to harness the support of 110,000 FELDA settlers and their children against the Barisan Nasional incumbents.

From our conversations with settlers near Bentong, Kuantan, Kota Tinggi, and Simpang Renggam, issues around cultivation and production of palm oil also weigh heavily on the minds of second generation settlers (or anak peneroka “settlers’ children” as they are colloquially known). Many anak peneroka are no longer interested in working in the fields and have subsequently moved to urban centers for better economic opportunities, resulting in abandoned or under-maintained fields. This was evident as we drove through Pahang and Johor via the Kuantan-Segamat Expressway. Anecdotally, we estimate the trees along the expressway to be at least 15-20 meters high and approximately older than 20-25 years, well beyond the optimum height (<14m) and age (<20 years) for cultivation.

For 'anak peneroka' who still live in the settlement, most prefer to sub-contract the production and harvesting to FELDA or foreign labourers. Settlers in Pahang spoke about taking on loans from FELDA to pay off their subcontractors while others in Johor took on debt to finance their re-planting activities. Johor settlers disclosed their debt obligations to be between RM50,000-RM100,000 for production, maintenance, harvest, and re-planting activities; this is consistent with nationally reported figures and estimates.

The debt includes a cash advance to cover minimum living expenses during the first three years of replanting when yields are low. These debt obligations continue for as long as the settler wishes to continue with the production. As one settler puts it, “perhutangan kami akan terus sepanjang kehidupan” (our debt will follow us for the rest of our lives).

Although taking on debt is part and parcel of smallholder palm oil production, questions remain as to whether the debt-for-production model is sustainable as smallholders continue to migrate to urban areas and the third generation are even less likely to remain in settlements. Resolving the financial situation of FELDA’s smallholders will be critical for FGV and whoever takes the reins of the Malaysian Parliament on Thursday.

Felda-FGV pre-election takeover deal rumour debunked

With a few days to spare before polling day, Felda Global Ventures Holdings Berhad (FGV) has debunked re-emergent rumours of a major takeover deal. FGV is a government-linked corporation closely linked to the Federal Land Development Authority (Felda). FGV's official statement is that “There is no truth in this story. It is not only false, it is also mischievous.”

FGV has been focussing on corporate reform after facing headline crises in the middle of last year. Its Board of Directors has also seen some changes since then and it largely comprises independent directors. At the Felda level, a deal was concluded with Peter Sondakh for a stake in PT Eagle High Plantation in 2016.

A takeover deal has been a longstanding speculation by International Palm Oil Monitor (IPOM), a secretive website. On 30 April 2018, IPOM asked if FGV might proceed with a deal before May 9, 2018 (polling day), stating the following: “It has been two weeks since our source spotted representatives from Indonesian Chinese tycoon Peter Sondakh’s Rajawali Group, representatives of PT GAMA Plantation, owned by another Indonesian Chinese tycoon, Martua Sitorus and representatives from a local Malay owned conglomerate at a meeting in a leading five-star hotel in Kuala Lumpur.”

The Edge Malaysia reports that “In the past FGV denied having any talks with Syed Mokhtar (a Malaysia Bumiputera tycoon), and parent Federal Land Development Authority (Felda)’s executives had denied any plan for Sondakh and Sitorus to surface in FGV.” The investment community has been speculating about it as far back as March 2017, with some seeing limited synergy with Syed Mokhtar's plantation arm, but favouring instead (then rumoured) China National Cereals, Oils and Foodstuffs Corp (COFCO) as giving FGV a leg-up into the China downstream market. Indeed, it was reported that no less than three China companies were vying for a strategic stake in FGV.

The question is whether Felda settlers would be in favour of or be worried about a potential FGV takeover deal. So far, settlers seems to be more concerned about bread-and-butter issues, and have limited interest in big financial deals. Moreover, if a deal were to generate a cash bonus, any concern may be allayed (but cash is not the norm for an asset-for-shares deal). Would the settlers worry about the dilution of their stake and that of Felda in FGV? Would they favour a major stake taken by a Malaysia-based tycoon versus foreign tycoons? As there is no deal on the table, this is not a real issue yet.

Background from the Indonesia palm oil sector: Some in the plantation sector speculate that Multi Gambut, a Sumatra peat plantation (previously owned by Tabung Haji, the Malaysia Pilgrim’s Fund, which sold its stake to a Martua Sitorus-related company) is a potential for any asset-for-shares deal. Tabung Haji took some time to dispose of the large peat plantation. The market talk was of the cash-rich Indonesian group getting a good deal as buying interest was then relatively scarce for such a large estate significantly on deep peat. Moreover, peat concessions face rising regulatory pressure in Indonesia. Experts also point to the the need for replanting (as Multi Gambut’s development started in the 1990s and oil palm trees have a typical economic life of 20-25 years, after which capital expense for replanting is needed). Some also worry that ganoderma disease (a risk linked to oil palm on peat) could cause the second generation oil palms on peat to be replanted within 15 years (5-10 years short of the typical lifespan). However, recall that some plantations on peat are managed and perform very well. The standard bearer for many is United Plantations in Teluk Intan, Perak (Peninsular Malaysia), which was developed decades ago. Overall, peat is a marginal soil that is usually regarded as being more difficult and more costly to (re)develop and operate on; as it faces fire risk in the dry season, it is carefully watched for hot spots. Martua Sitorus was a founder of Wilmar International Ltd, and is mentioned in a recent Indonesia investigative report. In April 2018, FGV announced new policies for improved peat management systems and peat restoration.

Khor Yu Leng is an independent political economist, assisted by Jeamme Chia.