This article first appeared in Personal Wealth, The Edge Malaysia Weekly on March 5, 2018 - March 11, 2018

The exponential rise in the use of smartphones, mobile wallets and e-payment systems has given birth to a new technology that uses big data to determine credit scores. The technology has been lauded for helping the underbanked gain access to credit, representing the first step towards financial inclusion.

The use of non-traditional data to churn out credit scores is now expanding beyond the underbanked and unbanked to reach even well-banked individuals who already have a credit score. This pool of data, which is used to discover patterns of users’ repayment behaviour based on their mobile phone and social media usage, is playing an increasingly important role in Asia alongside traditional credit scores.

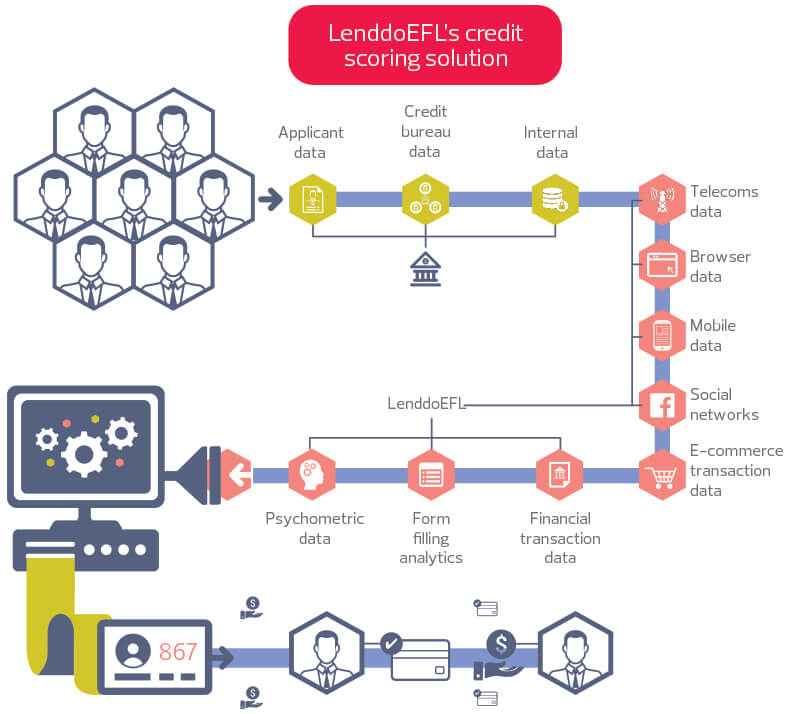

Based on studies that have drawn a correlation between mobile phone usage and repayment rates, algorithms have been created to predict an individual’s potential for defaults. LenddoEFL is one of the pioneers in this field. It started its operations in the Philippines in 2011 before expanding to other countries with large underbanked populations such as Mexico and Colombia.

The company has also established a presence in arguably well-banked countries such as South Korea and Australia. Last February, it established a partnership with credit reporting company Experian in Indonesia and Japan to provide their technology. It also partnered US-based credit score firm FICO in India in 2016.

Mark Mackenzie, managing director for Asia-Pacific at LenddoEFL, says the company will be announcing a partnership in Malaysia in mid-2018, although he is reluctant to disclose more details. “Today, the technology is being adopted by all the banks in Southeast Asia, which are at some level of evaluating how to use non-traditional data, be it smartphone, email or telecoms data. There is a significant amount of traction in non-bank financial institutions, financial companies and online peer-to-peer lending platforms to adopt this technology,” he adds.

The trend may continue to accelerate as the digital information generated by mobile phones on a daily basis increases. As pointed out by impact investment firm Omidyar Network in its 2016 Big data, small credit report, it is estimated that individual consumer data production will reach 35 billion terabytes by 2020 — some 44 times the data produced in 2009. It also highlighted a few reports that had observed more than 30 companies globally that are already creating credit scorecards using non-traditional data.

The benefits for regular customers who have a credit score history are that the additional source of information may improve their chances of getting a loan, particularly for those with mid-range scores. “It is not limited to the (underbanked) because we are able to increase significantly the predictive power for that segment, even for those who have previous banking experience,” says Peter Barcak, co-founder and CEO of CredoLab.

“The benefit for clients is the higher chance of getting a loan or card by using our service because lenders typically reject 70% to 90% of their customers. The second benefit is that good customers may get better pricing than bad customers because lenders can apply risk-based pricing.”

CredoLab is another company using non-traditional data for credit reporting. Headquartered in Singapore, the business-to-business company has clients in Indonesia, Thailand, Vietnam, Myanmar, the Philippines, China, Georgia and North Africa. Barcak says the company has a few prospects in Malaysia and is working on signing an agreement soon.

For lenders, the use of non-traditional data for credit scoring enables them to expand their pool of borrowers while keeping the risks in check. “Lenders can expand market share because they will know to whom they can lend using our tool. Their cost of risk will be much lower as we will add 10 to 30 Gini coefficient points to their current models, and every 10 Gini coefficient points will decrease delinquency by 20%,” says Barcak. The Gini coefficient is used to evaluate the predictive power of credit scoring tools.

Most lenders are not solely using this technology to assess potential borrowers. For those with existing credit scores, the data from both traditional and big data sources will be combined.

“Any chief risk officer would use as much data out there to help them make better decisions. We are not replacing what the banks are using today. We are very much augmenting what they have — those tried, tested and proven models that they have been using for the past 60 years. They are combining those tools with non-traditional data,” says Mackenzie.

Another benefit for lenders and borrowers is the quick turnaround time in using the technology. “I would say that the discussions that we are having in markets such as Australia, South Korea and Malaysia are often not just on credit scoring thin-file consumers but also giving all consumers a better customer experience,” he says.

“In the pursuit of building our technology to credit customers using non-traditional data, we have also built a stack able to deliver information on the consumer within seconds. As the big banks move towards digital banking and branchless banking, one of the first challenges they will come up against is the customer expectation that they will get faster decisions.”

Credit bureaus typically collect information from credit providers such as banks, credit card companies and non-bank financial institutions. Publicly available information such as court judgments, bankruptcy notices, telephone directory information and collateral registries could also be assessed. Other sources may include billing data from public utilities and other services, according to the Credit Reporting Knowledge Guide by the International Finance Corp. Malaysians can get credit reports from CTOS Data Systems Sdn Bhd, Credit Bureau Malaysia Sdn Bhd, Bank Negara Malaysia and RAM Credit Information Sdn Bhd.

Of course, thin-file consumers — those with little credit history — and micro, small and medium enterprises (MSMEs), which tend to use cash, are the ones most likely to benefit from this technology. Access to financial services allows individuals and families to plan for the long term as well as any unexpected emergencies. According to the World Bank, up to two billion adults globally do not have a basic account while more than 200 million formal and informal MSMEs in emerging economies do not have adequate financing due to a lack of collateral and credit history.

“There is a significant number of MSMEs or mom-and-pop stores in Asia-Pacific, like the sari-sari stalls in the Philippines. Huge amounts of money in the economy go through these small businesses, but traditionally they have had very limited access to even small amounts of trade credit. So, there is a significant amount of stress in building a credit risk scorecard,” says Mackenzie.

Other players offering similar technology are Tala in East Africa and Southeast Asia, Branch in Kenya and Tanzania and Trusting Social in Vietnam, Singapore and the US. US-based credit scoring giant Equifax partnered Cignifi to offer similar services in Latin America in 2016. Famous mobile-based financial company M-Pesa in Kenya and Tanzania also has its own version of the technology through M-Shwari.

How does the technology work?

Credit scores are traditionally obtained by analysing one’s loan payment history. But for consumers who have not taken out a loan or owned a credit card, a credit score can, ironically, be hard to come by. It then turns into a vicious cycle as the lack of a credit score affects their ability to apply for a loan in the future.

Companies such as LenddoEFL and

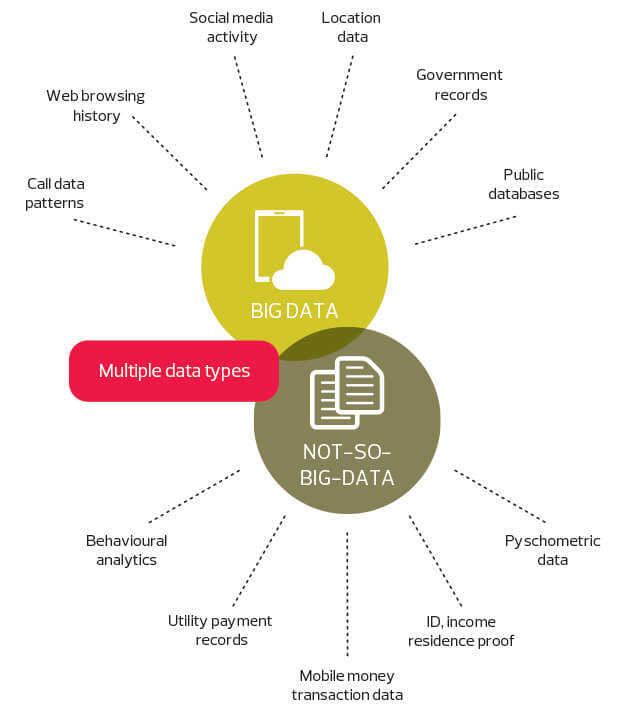

CredoLab can use the data provided by telcos or by asking potential borrowers to go through a process, such as downloading an app, to allow them access to their mobile phones. The type of data points collected varies. Some believe that the data collected on phone usage patterns — such as duration of calls, number of contacts, types of apps downloaded — provide better indicators while others collect data from social media usage.

Both LenddoEFL and CredoLab’s clients are lenders. This means that when potential borrowers approach the lenders, they may be asked by the lenders to go through a process to authorise access to their mobile phones. In CredoLab’s case, potential borrowers have to download the CredoApp. After the company crunches the data, a credit score is provided to the lender, usually within minutes.

“We are interested in behavioural variables or data points that give us an insight into the character of the consumer. So, if I gave you my mobile phone for half an hour, you could probably tell something about my character from how well organised it is. Does my behaviour look consistent? Do I talk to the same people every week or month?” says Mackenzie.

“For a long time, companies such as FICO have identified certain behavioural traits that are consistent with good repayment behaviour. We like the same type of things, but we get the evidence of that from a different data set.

“Some examples are looking at the number of contacts you have, how many people we would expect you to contact regularly and the times of the day that you are active. We could also look at your charging behaviour. Are you a person who lets your phone run out of battery? These are simple examples of ways that we could use the data to get an understanding of your character.”

The way they correlate mobile phone usage with repayment behaviour is by creating a model. LenddoEFL creates a different model for each client, depending on the target market, demographics or type of loan and credit. The model could be built using the studies it has conducted in the past, depending on the client’s demands.

Mackenzie says it has 12,000 variables of tracked mobile phone usage behaviours that it can tap to create features, which are behavioural characteristics relevant to the potential of repayment. “Over the last seven years, we have collected millions of social profiles. We have built features that are put together by multiple variables, which we know are very predictive. We rarely use one single variable such as the number of calls made at night (to predict behaviour). The models that we have built use different types of variables to build a feature.”

An example of a feature the company focuses on is consistency of behaviour. “That is one of the best types of data we look for. Evidence of erratic behaviour clearly does not correlate with the propensity for being a good payer,” he says.

LenddoEFL collects information from mobile phones and email. It also requires potential borrowers to undergo psychometric tests in the form of short quizzes as part of its analysis. It also works with data sources such as banking transaction data if the client asks for it. Instead of only tracking mobile phone usage, any platform that is transactional in nature, such as consumer loyalty cards or mobile wallets, can generate relevant data.

“Mobile wallet penetration is increasing exponentially. A lot of mobile wallet companies are interested in being a track for the extension of credit,” says Mackenzie.

“They have high volumes of transaction data and it can be used in the same way banks would use CASA (current account, savings account) for transaction data. Any transaction data has significant discrimination for building not just a credit-risk model but the capacity-to-pay models. I think we will see huge investments from financial technology (fintech) behemoths in the mobile wallet landscape across Asia.”

For instance, China-based fintech giant Ant Financial, which operates popular payment solution Alipay, has a credit-scoring service called Sesame Credit for Alipay users. Its competitor, Tencent, flirted with a trial of Tencent Credit earlier this year.

CredoLab also creates a distinctive scorecard model for each lender. When it strikes up a partnership, it embarks on a data collection phase for at least three months where they collect data from borrowers as well as their repayment behaviour. During this period, the lender disburses loans as usual without input from CredoLab. The borrowers are asked to download the CredoApp to enable access to data.

“After two or three months, we will have a sufficient number of records. Then, by correlating the digital footprint from mobile devices and performance data from that particular lender, we are able to develop a scorecard,” says Barcak.

“From the moment we put that scorecard into production, if there is a new banking customer, the process will be the same, but we can send a score to the lender to make the credit decision. The score is a probability of default — it is between zero and one. Then, it is up to the lender to make the decision.”

A higher score means the individual is less likely to default.

For most people, mobile phone data can be extremely private. Guarding the data privacy rights of individuals then becomes paramount for companies in this field.

“We are only collecting anonymous data and that is very important because our customers, who are the lenders, care a lot about data privacy and clients’ rights. It means that CredoLab does not know the client’s name, address, email address or phone number,” says Barcak.

“What we are collecting is raw data available on the client’s mobile device. The data is related to calls, SMS, applications installed, calendar events or mail. It is about the client’s behaviour on that phone. It is not about who that person called, but rather the duration of the calls, such as are you making your calls during business hours mostly or during the night, or what does your inbox look like in the morning?”

A 2013 report by the Center for Financial Inclusion in the US suggests that customers must be allowed to give consent or deny the use of their data under such settings. Governments may also need to amend the rules that govern who owns and who can use such data.

CredoLab has built more than 50,000 features for the basis of scoring. This differs from previous approaches where only 40 to 60 of the most relevant features are used to create a scorecard.

“We use models and statistics to indicate which particular behaviour pattern is good or bad. We are able to do so after correlating the digital footprint with the performance from the lender,” says Barcak. The variables and features the company has are proprietary so he is not able to share the details. But he says an example could be that the more contacts you have on your phone, the better your score.

“We also look at the different applications and calls made or received. Some apps are of higher significance. For calls, we look at patterns of behaviour, such as how many

outgoing night calls are made, the total duration of the calls, how you react to missed calls, how often you return those calls … all these things matter,” says Barcak.

Both companies are unable to disclose the clients they are currently working with. Their clients range from major banks to smaller non-bank financial institutions.

Last October, Lenddo merged with Entrepreneurial Finance Lab (EFL), which also works on digital credit scoring technology, to become LenddoEFL. The merger has expanded their coverage to 30 countries.

“We are expecting another year of robust growth globally. The non-traditional data space will reach some kind of inflection point, where the credibility of non-traditional data for credit risk is accepted in the risk community. And we are starting to see evidence of that,” says Mackenzie.

The beginnings of LenddoEFL and CredoLab

LenddoEFL was founded in 2011 by Richard Eldridge and Jeff Stewart. They had been running another business in the Philippines and were puzzled when they observed their well-educated permanent employees requesting salary advances from them. This led them to realise that many of their employees, who were part of the emerging middle class, did not have sufficient credit history.

Mark Mackenzie, LenddoEFL’s managing director for Asia-Pacific, has known the founders for more than two decades and has a background in management consulting. Together, they decided to tackle the problem faced by thin-file consumers who are eager for credit in developing countries. They had a hypothesis that they could use non-traditional data from mobile phone usage to predict loan payment potential.

“We did some research to look at the emerging middle class who were thin-file. The thing they had in common was that they had a very rich digital footprint. I guess the natural extension of our inquisitiveness was, if all these consumers had a rich digital footprint, it could conceivably tell us something about their behaviour,” says Mackenzie.

“Could it tell us something about their loan payment behaviour, their character? That was the hypothesis we wanted to test — if looking at one type of behaviour would enable us to build a model that could predict another type of behaviour.”

So, they decided to start their own lending business in the Philippines. “We actually did the first completely paperless lending company in the Philippines, then we went to Colombia and Mexico — all very different markets. We did that for three years just to get the payment outcomes to help us build the algorithms and prove our hypothesis that this data can be discriminatory and that it can work. After three years, we proved that the data can be used to build models to predict good and bad borrowers,” says Mackenzie. At that point, they pivoted to become a business-to-business player.

They have a team of data scientists with experience in machine learning based in New York. Mackenzie says all this knowledge and experience has helped them take this risk and build a credit-risk model based on non-traditional data — a feat that had not been done before.

Meanwhile, CredoLab had its beginnings on the other side of the world: Ukraine. Co-founder and CEO Peter Barcak is experienced in the field of risk management. He was in retail risk management with BNP, Citibank, Intesa Sanpaolo Group and Platinum Bank.

“I was at Platinum Bank in Ukraine as chief risk officer. Five years ago, we did a pilot project where we took data from a telco and correlated it with the performance data of customers who indicated that they had a number with that telco. We combined the data and realised that we were able to increase the Gini coefficient — which is the indication of the quality of the scorecard — by 20%, which is huge. That pilot project was very successful as it had a remarkable impact on our ability to accurately and consistently rate retail customers,” says Barcak.

After a stint at business school, Barcak and his former colleagues from Platinum Bank decided to bring their expertise to Asia, where they could improve credit access for those left out of the traditional banking infrastructure.

“We started talking to telcos in this region, but soon realised that they were not ready to share data for various reasons. First, from an IT perspective, they were not ready for this as they needed to integrate 25 different databases into one. And some of them were thinking that maybe they would do the lending themselves, so it did not make sense for them to share data with the others,” says Barcak.

So, they pivoted from this idea and created an Android-based application called CredoApp. It enables the company to take a digital footprint from a mobile phone. The data can then be used to predict the customer’s potential credit risk.

“CredoApp is distributed to our consumer-lender clients on a subscription basis. We currently have more than 20 paying customers. It is a B2B business so our customers are lenders — they could be big, mid-sized or small banks, consumer finance companies or app-based lenders,” says Barcak.

LenddoEFL’s investors include financial technology (fintech) venture capital (VC) firm Life.SREDA, impact investing firm Omidyar Network, technology VC firm Blumberg Capital and iNovia Capital. CredoLab’s investors include regional fintech VC firm Fintonia Group, Forum Capital Advisors and Indonesia-based institutional investor Reliance Modal Ventura.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.