This article first appeared in The Edge Malaysia Weekly on April 4, 2022 - April 10, 2022

IT is not a secret that the fiscal position of the federal government is not healthy. With the additional spending aimed at stimulating the economy and providing a buffer to weather the pandemic, things have worsened over the last two years.

The government’s fiscal deficit increased to 6.5% of GDP in 2021 from its target of 5.4% as outlined under Budget 2021. This is after it announced four additional assistance and stimulus packages worth RM25 billion during the year. At 6.5% of GDP, the deficit came to RM98.8 billion, according to the Ministry of Finance’s (MoF) Fiscal Outlook 2022.

As the country transitions towards the endemic phase of Covid-19, the topic of fiscal consolidation has come up again. For starters, there is a view that it is unsustainable for the government to invest in mega public transport infrastructure while continuing to subsidise fuel prices, especially when crude oil prices are above US$100 per barrel.

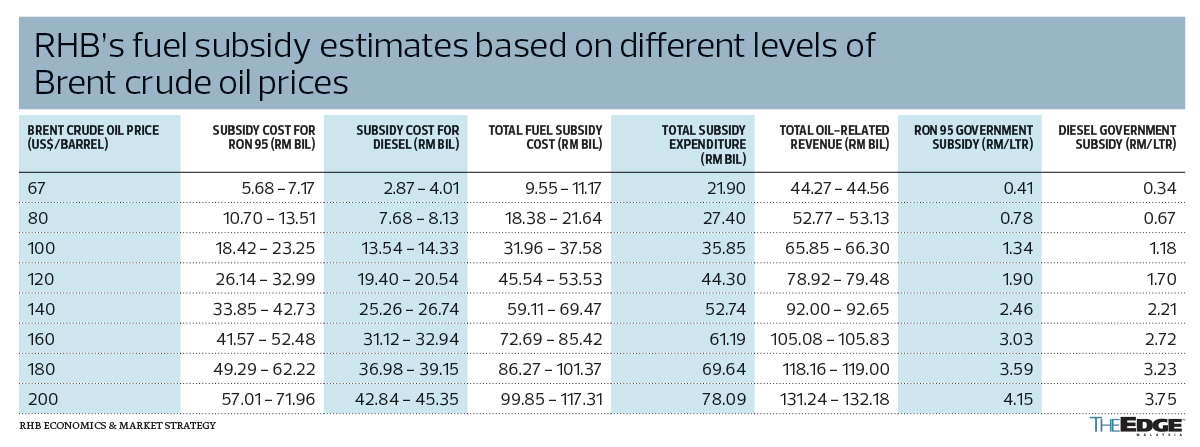

Finance Minister Tengku Datuk Seri Zafrul Aziz has said the government may be looking at a fuel subsidy bill of RM28 billion this year if crude oil prices remain at an average of US$100 per barrel.

However, an analysis by RHB Economics and Market Strategy, released in a report last Friday, pegs it even higher. It says the total fuel subsidy could range between RM31.96 billion and RM37.58 billion with Brent crude averaging at US$100 per barrel.

Mega infrastructure projects in Malaysia are usually funded by debt as the government’s fiscal situation is quite dire, with a primary balance shortfall of 3.9% of GDP in 2021 and a forecast shortfall of 3.3% of GDP this year.

It is worth noting that the 2022 primary balance shortfall forecast was done prior to the sharp gains in crude oil prices. The benchmark Brent crude rose from US$68.87 per barrel on Dec 1, 2021, to US$127.98 per barrel on March 8, fuelled by the Russia-Ukraine conflict. While crude oil prices have fallen off their peak, they are still hovering above US$100 per barrel.

With the government lacking fiscal space to undertake development programmes via revenue generated, it has opted to borrow to finance projects. Last year, the government raised RM98.8 billion from domestic borrowings to fund its operations and development plans.

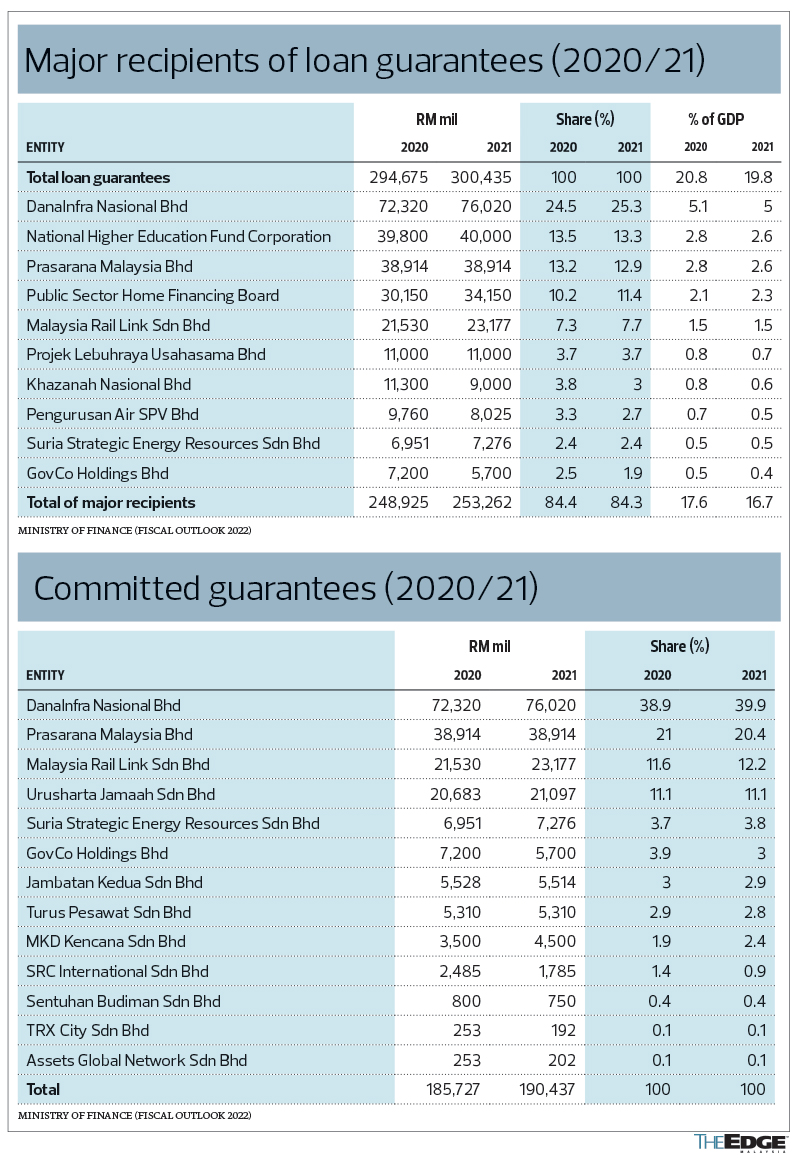

For rail infrastructure, the government utilises DanaInfra Nasional Bhd as a vehicle to raise debt to fund its projects. The debt is guaranteed by the government.

According to DanaInfra’s website, it has raised RM78.6 billion to fund the construction of the MRT Kajang Line, MRT Putrajaya Line and a portion of the Light Rail Transit Line 3.

The agency is the biggest issuer of government guarantees (GG). As at end-June 2021, the total outstanding GGs had increased slightly to RM300.4 billion, or 19.8% of GDP, from RM294.7 billion, or 20.8% of GDP, in 2020.

By segment, 54.2% of the GGs issued are for infrastructure-related financing, followed by services (26.6%), investment holding (8.3%), utilities (6.8%) and others (4.1%), according to the MoF.

On the surface, GGs are a facility given to government entities to undertake strategic projects that have longer gestation periods, and facilitates borrowings at a more competitive financing rate.

However, in its Fiscal Outlook 2022, the MoF said that in certain situations, entities with GG facilities may also require funding from the government to assist them in debt servicing, working capital assistance or cash flow support. This means some entities with GGs fall back on the government for debt servicing, thus increasing the government’s debt servicing payments. The GGs provided to such entities are called committed guarantees.

According to the MoF, there had been a slight increase in committed guarantees to RM190.4 billion, or 12.6% of GDP, as at end-June 2021 from RM185.7 billion, or 13.1% of GDP, in 2020. This was primarily due to issuances by DanaInfra and Malaysia Rail Link Sdn Bhd.

Including GGs, debts owed by 1Malaysia Development Bhd and other liabilities, the federal government’s debts and liabilities exposure stood at RM1.334 trillion, or 88.1% of GDP, in 2021, according to the MoF.

“From a public finance perspective, you cannot do both — keep subsidising pump and gas prices while also encouraging motorcar sales by foregoing duties and so on, and spend to build rail infrastructure, as well as all the toll highways,” says economist and former DanaInfra principal official Dr Nungsari Radhi.

“What do you get out of all the spending? It is all driven by projects instead of the result of a cohesive and comprehensive analysis of what public expenditure should be.”

Since the debt raised by DanaInfra to fund infrastructure projects are outside the ambit of the federal government’s budget, as it is not a profit-making entity, and neither MRT Corp Sdn Bhd nor Prasarana Malaysia Bhd are profitable, the onus falls on the government to service these borrowings.

This means that, at the end of the day, it is the taxpayers who will foot the bill.

Bank Islam Malaysia Bhd chief economist Dr Mohd Afzanizam Abdul Rashid says that while the fuel subsidy reform has to happen, he warns that the timing is extremely crucial. He points out that now may not be the right time to make changes to the fuel subsidy regime as it would create a negative shock to the economy.

“We have learnt that when the previous administration raised RON97 by 78 sen in June 2008, it resulted in the inflation rate shooting up to 7.7% and 8.5% in June and July 2008 [respectively] from 3.8% in May,” says Mohd Afzanizam.

“Certainly, we do not want that to happen again at a time when the economic recovery is still in its nascent stage. There must be a clear roadmap to gradually remove the fuel subsidy completely.”

Nevertheless, Dr Sailesh K Jha, group chief economist and head of market research at RHB Bank Bhd, opines that there is still enough cushion from oil-related revenues to offset potentially higher fuel and total subsidies.

“So far in 2022, Brent oil has averaged around US$98 per barrel. And if this is indeed the average for the whole of 2022, our estimate for the fuel subsidy would be around RM33.5 billion, around RM35 billion for the total subsidies, and the total oil-related revenues would be around RM64.8 billion,” Sailesh says in the RHB Economics and Market Strategy report.

“For various oil price assumptions, our analysis indicates that even if our total subsidies estimate is erroneous by 50%, there is still enough cover from robust oil-related revenues via petroleum tax revenues, Petronas dividends and petroleum royalties to offset higher than programmed budget fuel and total subsidies in 2022.”

He also pointed out that the bank expects the government’s development expenditure to be lower than what was planned for 2022 at RM73.4 billion, compared with the MoF’s estimate of RM75.6 billion.

In addition, the prosperity tax could yield at least RM15 billion in revenue and windfall taxes could be larger than what the government has anticipated, and offset the higher subsidies in 2022, says Sailesh.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.