This article first appeared in The Edge Malaysia Weekly on November 25, 2019 - December 1, 2019

YOU have heard it. Oil giant Saudi Aramco has begun the book-building exercise for possibly the largest initial public offering ever, given its plans to raise up to US$25.6 billion from investors looking to participate in the most profitable company in the world.

The proposed listing, though smaller-than-expected now, involves a mere 1.5% stake, or 30 billion shares, in the Saudi oil giant. With an indicative value of 30 riyals (US$8 or RM33.37) to 32 riyals per share, this values the whole company at US$1.5 trillion to US$1.7 trillion.

Oil observers are keeping a close watch on the IPO because of its sheer size and Aramco’s role as de-facto chief of the Organization of the Petroleum Exporting Countries (Opec), as well as being the supplier of 10 million barrels per day (bpd), which meets a 10th of global oil demand at present.

Considering Aramco’s large presence in the global oil space, how will the outcome of its IPO affect oil and gas markets elsewhere?

A benchmark on valuation

A fund manager with a local investment firm tells The Edge the IPO “could serve as a benchmark for the valuation of existing listed companies of similar operations”, pointing to the listed subsidiaries of Petroliam Nasional Bhd (Petronas) as examples. “The listing model will also likely be studied by Petronas or even its shareholder, the Malaysian government itself. If Aramco’s valuation is good, then why not do the same thing?”

There has been talk of monetising the upstream operations of Petronas under Petronas Carigali Bhd to boost Putrajaya’s constrained wallet. Industry watchers estimate that the listing of a 10th of Petronas group, based on Aramco’s valuation, could raise about RM86 billion. That said, in the past the national oil firm has preferred to opt for a listing of its subsidiaries.

Aramco’s indicated dividend yield of 4.4% to 4.8% sits at the low end compared with the average of 5.7% offered by Western oil majors. In comparison, the returns of Petronas Chemicals Group Bhd are even lower, given its indicated yield of 4.07%.

At a valuation of US$1.6 trillion, Aramco’s annualised 1HFY2019 results would translate into 17 times price-earnings ratio, according to reports, on a par with that of Petronas and within the range of the five supermajors (Shell, ExxonMobil, Total, Chevron and BP).

Malaysia’s O&G rally local-centric

However, the impact on Malaysia’s oil and gas sector is likely to be minimal as it is highly local-centric, says a senior executive with a locally listed upstream O&G service provider. “For now, our operations are highly domestic. There is a huge dependency on Petronas’ upstream activities.”

Domestically, two names have emerged as potential beneficiaries under Aramco — Malaysia Marine and Heavy Engineering Holdings Bhd and Sapura Energy Bhd, both of which separately signed long-term agreements with Aramco last year for the provision of engineering, procurement, construction, installation and commissioning work for offshore facilities.

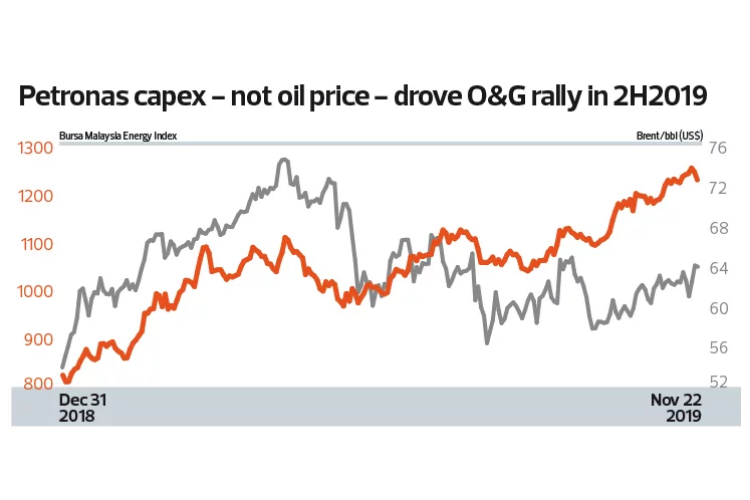

In any event, O&G counters on the local stock exchange have had a good year so far. Bursa Malaysia’s Energy Index chalked up an impressive gain of 50% year on year, largely led by Petronas’ ramped-up local upstream capital expenditure of RM15 billion, from RM8.5 billion last year.

With Petronas’ upstream capex concentrated in 2HFY2019, analysts believe there is still room for more upside, even if share prices have rallied substantially, as Malaysia’s O&G stocks are rising from a low base.

Moreover, many counters have experienced an upward rerating this year as prospects improve and companies are able to cope with the low oil price environment.

“The local energy counters are much more affected by the fundamentals of the sector rather than the Aramco IPO itself,” says Maybank Kim Eng analyst Liaw Thong Jung.

Among analysts, consensus top picks include storage tank operator Dialog Group Bhd, floating production vessel operator Yinson Holdings Bhd, engineering services group Serba Dinamik Holdings Bhd and rig operator Velesto Energy Bhd, owing to their job prospects plus the balance sheet to back them.

“It is also good to have a rotational play with laggards that are currently undervalued, such as vessel operators,” adds Liaw, who has a “buy” call on Alam Maritim Resources Bhd and Icon Offshore Bhd in the segment.

“A lot of companies have re-based their costs,” he says. “This coincided with contract revisions … (as) they have adapted to the new norms. The key is that there should be oil price stability.”

Eyes on the aftermath

In that sense, Aramco’s IPO outcome could still nudge the market. With oil prices averaging US$61 per barrel in the first 10 months of the year, the market is a long way from its heyday.

Pundits will be keeping a close eye on how Aramco behaves as a listed entity, given that its role in Opec could influence oil market movements.

More certainty can be expected when its shares are priced. While Reuters reports that the IPO’s institutional tranche is oversubscribed, keep in mind that the original plan was for an international listing with a group valuation of US$2 trillion.

It is speculated that Aramco’s scale-back to a lower group valuation and a local listing were the result of a lack of international interest and difficulties in securing cornerstone investors. Even Petronas has decided to give the IPO a miss, confirming last Friday that it would not be participating in the public share sale.

“Petronas would like to confirm that after due consideration, the company has decided not to participate in Saudi Aramco’s initial public offering exercise,” the national oil company told Reuters in an email statement.

Briefly, concerns over the mega IPO ranged from inadequate information in the prospectus to high valuations, geopolitical risks and the prospects for the oil market.

The IPO is currently limited to the Kingdom’s Tadawul stock exchange, which opened its doors to foreign investors only four years ago. Liquidity is another concern.

As a result, while Saudi Arabia has seen funds flowing out of other local stocks as investors prepare to buy into Aramco next month, the movement has not transpired elsewhere. For now the local IPO is a possible yardstick if Aramco pursues its international listings as planned by 2021.

If that happens, Aramco will eventually compete with other oil companies for the same investment pool, according to Wall Street research and brokerage firm AllianceBernstein in a recent market report.

Time will tell how much Aramco post-IPO will influence global O&G market sentiments.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.