This article first appeared in Personal Wealth, The Edge Malaysia Weekly on June 25, 2018 - July 1, 2018

Many millennials who are just cutting their teeth on wealth management have found that they are making costly financial mistakes that could reduce their net worth. By arming them with the right knowledge and support, they can avoid making these mistakes, says Whitman Independent Advisors Sdn Bhd founder and managing director Yap Ming Hui.

Yap, whose company has been providing advisory services for 18 years, observes that most of its middle-income clients had lost between RM1.5 million and RM3 million in their 20 to 30 years of working life due to “unnecessary financial mistakes”.

Having conducted numerous talks and seminars for the public and private sectors, he says many of the participants, who were in their fifties or sixties, often shared their frustration of not having financial foresight when they were younger. “They said they had made so many financial mistakes and lost quite a bit of money, and that they only had a few more active income-earning years left to achieve financial freedom, if that is even possible,” he adds.

As their wealth managers, Whitman financial advisers often find themselves doing some housekeeping before they can help their clients create a road map that will help them achieve financial freedom. “We would need to do something about some of their poorly performing investments — [financial products] which they shouldn’t have purchased — or life insurance with very high premiums,” says Yap.

He adds that based on his experience, young people generally do not realise that buying such products involves decisions that will either move them closer to or further away from financial freedom. “Considering that they have limited resources, millennials cannot afford to make many mistakes. They need to ensure that every ringgit they earn is allocated properly to optimally support them in achieving their financial goals,” says Yap.

“If they are not careful, they may end up buying products that may deplete their hard-earned money. Unfortunately, some irresponsible financial service providers, who choose to sell financial products to unknowing consumers without first referring to their financial freedom road map, could compound the situation.”

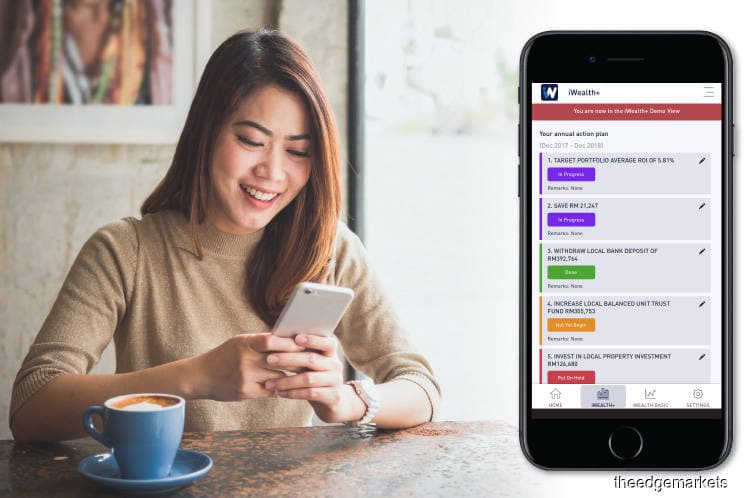

Whitman recently launched its wealth management mobile application, iWealth, to address these issues. Yap says it is the country’s first adviser-driven wealth management mobile app that “seamlessly integrates bespoke advisory services with financial technology (fintech) innovation to deliver personalised wealth management solutions”.

Whitman, he says, prides itself on being a holistic wealth management (HWM) company that specialises in delivering complex wealth management solutions to high-net-worth individuals, who are usually not so young. The HWM service measures performance not by the return on investment or assets under management, but the client’s growth in total net worth.

“The service covers eight areas — investment planning and management, risk management and insurance, tertiary education planning for children, retirement planning, asset protection, estate planning, debt and loan management and tax planning. But the most important element is a personalised road map to financial freedom, which is developed to ensure that the solutions prescribed are given based on the client’s unique situation and are in his best interests,” says Yap.

He adds that millennials are an underserved market when it comes to wealth management. The typical services offered by private banking entities usually require clients to have at least RM1 million to RM2 million in their bank accounts, he points out.

“Where can millennials go to find such services then? Banks have been providing these services [to wealthier clients] for decades, so why would they bother serving a smaller segment of clientele with less money?” says Yap.

“I am not sure how profitable this app will be, but I feel that it is the right thing to do and we want to enter this market [mobile wealth management platforms] and start offering our services.”

iWealth offers Whitman’s HWM service, which was previously only offered as a premium offline service [worth RM1,800 per year] to high-net-worth and upper-middle-class

clients. “The low entry cost makes it more affordable and appealing to millennials as it supports them in building their personalised road map to financial freedom. In the past, they may not have had the opportunity to do so due to the high advisory fee and higher minimum asset requirement,” says Yap.

For an annual fee of RM480, users can avail themselves of the iWealth+ package, which offers access to personalised financial documents such as income and expense statement and balance sheet, a financial health check, a tailor-made road map to financial freedom, a custom-made action plan with strategies to achieve their desired financial freedom, online consultation sessions with a dedicated human wealth manager and an annual report card. The annual report card helps users measure their wealth management progress against the recommendations provided by a Whitman-licensed wealth manager.

The app then highlights gaps and opportunities to improve the user’s financial position, including personalised strategies to achieve financial freedom. “It even helps users understand the impact of life events on personal finances, such as making a home purchase, starting a family and investments, by providing tangible step-by-step solutions to navigate these important decisions,” says Yap.

Human-driven fintech

Making financial decisions can be difficult when one’s goal is to achieve financial freedom. And without a road map, the task becomes even more challenging, says Yap.

iWealth’s compelling value proposition is going back to the basics and offering the user a holistic and tangible roadmap, he said during the launch of the app. It integrates offline HWM disciplines with the online user experience by aggregating, analysing and organising financial information such as assets, liabilities, income and expenses.

The HWM process begins with collecting the user’s financial information. Describing the initial step as “thorough and elaborate”, Yap highlights the role of human advisers in collecting the data.

“Malaysians are quite sensitive and secretive about their financial information, but our wealth managers are able to get them to open up [about their financial standing]. Once this is done, the information is passed on to our para-planner team. Then, our proprietary software helps them to identify gaps and recommend actions,” he says.

“They need to test many scenarios and recommend actions such as increase investments, reduce living expenses and switch unit trust funds. So, there are quite a number of actions and scenarios to weigh in coming up with a comprehensive financial plan.

“Only after this process will the advisers be able to get back to their clients and present a report. The implementation of the plan also requires a thorough process as Whitman does not allow advisers to simply pick any product. We only deal with shortlisted products on which due diligence has been carried out.”

Yap acknowledges that the wealth managers cannot cover all aspects of financial planning, hence the need for specialists to assist them. “There are various aspects to planning such as choosing the right insurance products and estate planning. So, while the main contact is the designated wealth manager, he or she is assisted by other specialists,” he says.

The difference between the offline HWM service and the one available via the app is that clients can communicate with their wealth managers remotely via video calls. The offline service requires clients to have at least RM2 million in asset, while the app has a lower requirement.

“That is because if your asset value is more than RM2 million, the wealth managers would have to meet with you in person as your situation is more complex,” says Yap. Those who plan to use the app should have monthly disposable income of at least RM1,000 or earn RM5,000 a month, he suggests.

Yap says while the company will not discount the advantages of artificial intelligence (AI) and robo-advisory services, wealth managers will continue to be an essential part of financial planning, even in the next 20 years. “Financial decision-making is so human. We have seen so many cases where clients need human inference, human encouragement and human assurance and we do these things at Whitman,” he points out.

“Some of our clients had to be assured several times before they could decide whether or not they were ready to retire. So, how would you get AI or a chatbot to assure them in such cases?

“However, the AI element could come into play by helping us accumulate our best practices and best pieces of advice. We just need to figure out how to ensure it complements our human advisory process so that the interface and flow [of communication] is natural.

“While robo-advisors apply AI to create better investment decisions, we will apply AI to empower our human advisers as they would need to read and remember a lot of things, which is not humanly possible. So, the ideal model is to use AI technology to compile all this knowledge and help the wealth managers provide advice.”

Yap says Whitman will be tapping the latest technologies to improve the app’s processes. “Some technologies are useful to us now while others, such as robo-advisory, have not matured yet. We can pick and choose the technology and continue to improve the user experience.

“Three years down the road, I would say that iWealth users will have a totally different experience when they subscribe to the service compared to now because by then, 70% of the app’s content will come from technology while the remaining 30% will come from humans. Currently, it is the other way round. So, it will be like an evolution.”

He says the company is waiting for the regulator [the Securities Commission Malaysia] to get banks to allow web providers and fintech companies to gain access their clients’ data. “By then, we would get 50% of the job done as the clients won’t have to find the statements for us. However, that does not mean we should not enter the market even though we are not a tech company. It is now or never.”

Yap acknowledges that the app is far from perfect and there is a lot of room for improvement. “One thing I have learnt about technology is that you do not have to come out with the perfect product. You can have a minimally viable product so that you can continue to improve with the feedback provided by users,” he says.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.